9.5.3. Scope of activities and the Intelligent Customer

In order to specify the scope of activities that the Go-Co would be expected to undertake, the customer interface between MoD and the Go-Co would need careful review and possible reformulation.

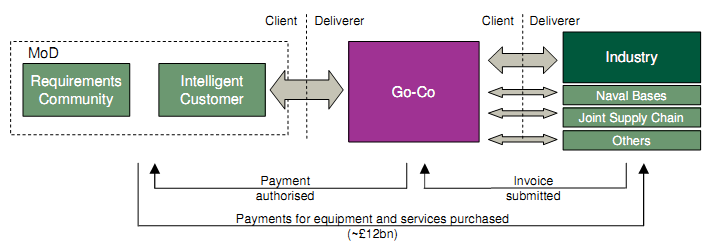

The Go-Co's primary interface for equipment procurement with the MoD would be with the Intelligent Customer ("IC") organisation, which would be charged with capability planning, project and programme investment decisions, formulation of business cases and monitoring of Go-Co performance. It would be the TLB for equipment procurement expenditure It is likely that the IC would be built from the Capability Sponsor organisation, which would need to be enhanced if it is properly interrogate and control the Go-Co. Concretely, this means that the MoD would need to develop both technical expertise and financial skills outside of the Go-Co, including an improved cost estimation function, if it is to fulfil its role adequately.

The Go-Co would be principally concerned with the effective management of procurement and support projects which had been specified and approved by the IC. This means Go-Co is the "deliverer", not the "decider" and is not part of a "unified customer" construct as DE&S is now.

In addition it would be expected to provide support to the IC in providing pre-approval inputs or services, including independent cost estimates, industry inputs on options, technical feasibility, etc. which may be required to supplement the IC's own enhanced internal knowledge base or resources.

The IC would be expected to be able to carry out performance, cost and time tradeoff assessments independent of the Go-Co in framing its requirements and making recommendations to the IAB for approval.

This arrangement is illustrated schematically in Figure 9-2.

Figure 9-2: Potential operation of DE&S as a Go-Co

The Go-Co acts as a professional project manager, in a manner somewhat akin to the role that a Quantity Surveyor would play on a construction project: It would manage the contracting process and scrutinise the work that is being carried out. It would not, however, pay for the work once it is complete. Rather, it would approve invoices that contractors submit for scrutiny and which the MoD customer pays.

The Go-Co does not, therefore, control the full £12bn that the MoD spends on the EP. Rather, it controls only the <£1bn that constitute the running costs of the areas of DE&S that fall under COO's control. It is on this sum that the Go-Co would earn its management fee. Of course, the contract could be structured in such a way that the Go-Co is additionally rewarded for delivering savings on the EP.

The role of Go-Co in TLCM and Programme management would also need reconsideration. As recommended earlier, the Review team believes the Department should focus primarily on securing efficiencies on a whole-life costing basis (i.e., initial procurement plus support costs for equipment) rather than attempting to overcome complexity associated with optimisation across all eight DLoDs. To this end, the Go-Co would be expected to continue to develop the Department's strategy in support transformation and support cost savings more generally, but under direction from the IC. This would imply the IC would need to upweight its focus on support costs compared to now. The broader programme management and DLoD tradeoff and optimisations associated with TLCM would be retained within the Capability Sponsor organisation, with the Go-Co providing inputs (e.g., option development or costings) on equipment or support issues as requested.