G.6. Run-on project costs

When a project suffers from a slippage of forecast ISD DE&S are required to maintain the IPT and corresponding central functions (e.g., Chief Corporate Services) longer than otherwise planned. However, DE&S is unable to track directly the costs associated with new equipment delivery (as distinct from costs associated with delivery of support to in-service equipment).

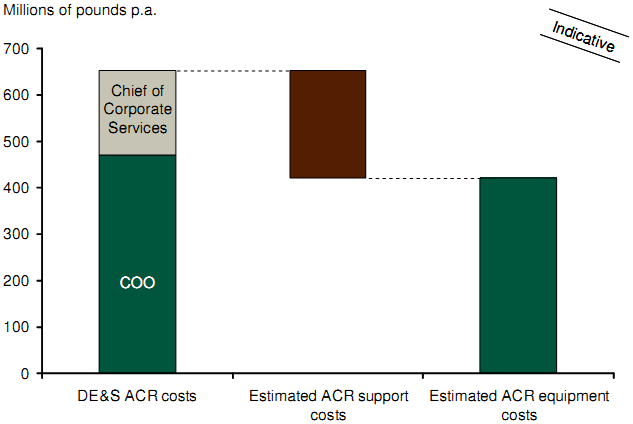

What is known is that the Administrative Cost Regime ("ACR") - ACR is primarily comprised of manpower costs. The control total for DE&S in 2008-09 was c.£1.3bn, of which c.£471m and c.£182m are the Chief Operating Officer and Chief Corporate Services budgets respectively.

To estimate of the proportion of ACR attributable to equipment procurement (as distinct from equipment support / sustainment), the annual ACR total of each IPT has been apportioned across procurement and sustainment depending on the amount of spend in 2008/09 managed by the IPT in the Equipment Procurement Plan (procurement) or Equipment Support Plan (sustainment), as shown in Figure G-5. This results in an estimated c.£420m p.a. of ACR costs associated with delivery of new equipment.

Impact of Equipment Plan delay on DE&S overhead

Note: * Has been calculated by understanding the proportion of in-year spend held in the ESP vs. the EPP at IPT / BLB level

Figure G-5: Impact of Equipment Plan delay on DE&S overhead

A range results from the consideration of how DE&S acts to size its project teams. As an upper bound, the Review team has considered the cost implications of assuming the sizes of the IPTs engaged in new equipment delivery are determined only at Initial Gate (i.e., no flexing of resources). If projects subsequently are delayed by c.80% vs. Initial Gate estimate, then the team could have achieved a similar total input of man-hours with c.45% fewer people (i.e., 1-{1/1+80%}).

Re-profiling of the size of the IPT during the lifetime of the project might be expected to mitigate c.50% of this cost, meaning a lower bound of c.23% fewer people. This corresponds to potential over-sizing of IPTs by £90m -£190m per year.

As noted in Chapter 6, an estimated c.1,000 man-years of effort are required each year for the annual planning round process within DE&S alone. Given the impact of delay, an estimated additional £15m-30m of MoD internal costs have been included. These would be associated with extensive re-profiling and other aspects of the planning round process, such as option development which are ultimately attributable to delay.