Budget performance

2.7 Project budgets against which cost performance is measured are subject to variations arising from price indexation (inflationary) effects, exchange rate variations, Government approval of changes in scope, transfers to Defence Groups and DMO cost performance.

2.8 Table 2.4 provides analysis of the budget variances between 2009-10 and 2010-11, measured against original project approval, for the 28 projects in this report by budget variation attribution. In 2010-11 the most significant impact to project budgets was from the application of price adjustments to move budgets to an out-turned value reflecting future price funding available to the global Defence budget. This accounted for an increase of $1.5b in 2010-11 for total project approvals of the unspent element of project budgets. The comparative strength of the Australian dollar against other currencies resulted in a net reduction against the project approval value of $1.2b. There were a total of three scope changes affecting this years report. This entailed the removal of the Moving Target requirement against Stand Off Weapon, additional Bushmaster vehicles; and, the reduction in the number of centre barrel replacement for the F/A 18 Hornet refurbishment programme (Para 2.13 provides further detail).

Table 2.4 - Major Variations to Budget Components

| Variance Attribute | Total budget variation (by attribute) to 30 June 2010 | Net budget variation within 2010-11 | Total budget variation (by attribute) to 30 June 2011 |

| $m | $m | $m | |

| Price Indexation | 6,286.2 | 1,470.7 | 7,756.9 |

| Foreign Exchange | -1,979.9 | -1,150.4 | -3,130.3 |

| Scope Changes | 4,820.0 | -50.0 | 4,770.0 |

| Transfers | -60.7 | 0.0 | -60.7 |

| Budgetary Adjustments | -342.9 | 0.0 | -342.9 |

| Budget Cost Saving | 0.0 | -107.2 | -107.2 |

2.9 These attributions are defined as follows:

• Price Indexation

The Price adjustment applied to project budgets reflects those indices agreed in the 2009-10 Defence budget update agreed by government. This provides a funding stream for projects to financially manage inflation. It is applied to the unspent component of the project budget. Price adjustments are in line with the deflator used by Defence to adjust the capital budget (for 2010-11 the deflator was the Specialist Military Equipment Weighted Average). Actual labour and materiel indices within each contract may differ to this deflator.

There was no change in the Specialist Military Equipment Weighted Average deflator during 2010-11.

2.10 Table 2.5 contains the breakdown by project of the price indexation as applied to 2009-10 (pre out-turned component) and the price indexation 2010-11 (post out-turned component) and the associated variance.

Table 2.5 - Price Indexation Breakdown by Project

| Project | Total Price Indexation as at June 2009-10 | Price Indexation (out-turn adjustment) June 2010-11 | Total Price Indexation as at June 2010-11 |

| $m | $m193 | $m | |

| AWD Ships | 854.8 | 318.4 | 1,173.2 |

| Wedgetail | 1,068.4 | 42.7 | 1,111.1 |

| MRH90 Helicopters | 556.2 | 123.6 | 679.8 |

| Super Hornet | 372.0 | 19.2 | 391.2 |

| LHD Ships | 350.0 | 78.4 | 428.4 |

| Overlander Vehicles | 313.3 | 433.6 | 746.8 |

| Joint Strike Fighter | 70.3 | 280.7 | 351.0 |

| ARH Tiger Helicopter | 414.9 | 3.3 | 418.2 |

| Hornet Upgrade | 314.3 | 9.2 | 323.5 |

| C-17 Heavy Airlift | 103.3 | 20.7 | 124.0 |

| Air to Air Refuel | 473.9 | 10.2 | 484.1 |

| FFG Upgrade | 228.1 | 2.2 | 230.3 |

| Hornet Refurb | 145.0 | 13.8 | 158.8 |

| Bushmaster Vehicles | 118.9 | 5.7 | 124.6 |

| Next Gen Satellite | 107.3 | 25.1 | 132.4 |

| HF Modernisation | 139.6 | 8.5 | 148.1 |

| SM-2 Missile | 118.7 | 9.2 | 127.9 |

| Additional Chinook | 16.3 | 30.6 | 46.9 |

| Armidales | 72.9 | 1.6 | 74.5 |

| ANZAC ASMD 2B | 71.0 | 5.1 | 76.1 |

| Collins RCS | 55.5 | 1.0 | 56.5 |

| Hw Torpedo | 91.5 | 7.9 | 99.4 |

| Collins R&S | 66.7 | 7.7 | 74.4 |

| UHF SATCOM | 16.5 | -19.5194 | -3.0 |

| ANZAC ASMD 2A | 88.7 | 12.6 | 101.3 |

| Stand Off Weapon | 59.2 | 3.3 | 62.5 |

| 155mm Howitzer | 8.7 | 8.5 | 17.2 |

| Battle Comm. Sys. | 8.3 | 7.3 | 15.6 |

• Foreign Exchange

Foreign exchange adjustment relates to increases and decreases to the total project budget to account for the movement in official exchange rates as advised by Central Agencies. This is consistent with Government policy as applied on a 'no win no loss' basis.

• Scope Changes

Scope changes generally take the form of changes in quantities of equipment, changes in requirements that result in specification changes, or changes to services to be provided which are accompanied by a corresponding budget adjustment. These total budget adjustments are made in response to Government approved scope changes.

• Transfers

Transfers occur when a portion of the project scope and budget is transferred to another project or sustainment product or to a Defence Group to deliver an element of project scope.

• Budgetary Adjustments

Budgetary adjustments describe all other variations to the total project budget. These include administrative decisions that result in variations such as efficiency dividends to be harvested from project budgets or other DMO and defence industry initiatives, as well as other adjustments not factored into the original budget plan.

• Budget Cost Savings

Cost savings attributed to any negotiated Foreign Military Sales or commercial contracts. These funds have been handed back to the Defence Portfolio.

2.11 Price indexation and exchange variations are environmental factors over which the DMO has no control. In particular, foreign exchange is driven by the relative strength of the Australian economy against overseas economies.

2.12 For example, in 2010-11 the US dollar averaged 1.005 against the Australian dollar compared to 0.8805 in 2009-10. The Australian dollar also strengthened against the Euro moving from an average of 0.6450 Euro in 2009-10 to 0.7253 Euro in 2010-11. These variations account for most of the exchange rate variations in table 2.4.

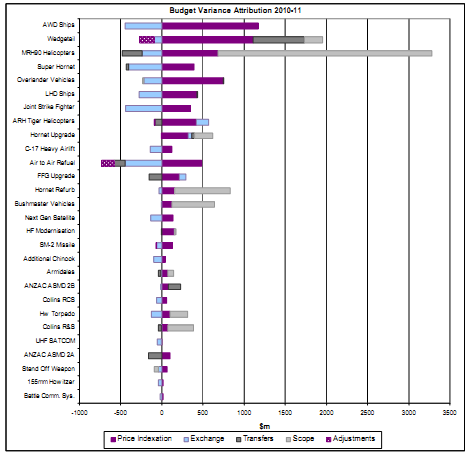

Figure 2.1 - Budget Components Above Original Second Pass Approval Value by Project as at 30 June 2011 (in $m)

2.13 Figure 2.1 presents a summary of the project budget variations from date of Government approval and subsequent transfer to DMO variance attribute (i.e. price indexation; foreign exchange; and real variations). Significant real variations fall within three main groupings:

• Scope changes: Projects with the largest budget 'real variation' from Government approved scope changes are:

- Wedgetail (June 2004) - Increased from four to six aircraft;

- MRH90 Helicopters (June 2006) - The significant budget increase is predominantly related to the scope increase from 12 to 46 helicopters for troop lift and maritime support capability to replace both the Black Hawk (Army) and Sea King (Navy) platforms. Additional facilities were also required in support of the MRH90 platform;

- Hornet Upgrade (June 2001 - May 2007) - scope increased to include an upgrade to the aircrafts' electronic warfare self protection suite; (December 2004) scope decrease to remove Radio Frequency Jammer, (October 2003) scope increase to include Hornet Air Crew Training System, (June 2001) White Paper considerations;

- Hornet Refurbishment (October 2010) - In December 2010, Government approved the reduction in the number of centre barrel replacements. Government approval also included direction to close the major capital projects AIR 5376 Phases 3.1 and 3.2;

- Bushmaster Vehicles (May 2011) - vehicle numbers have increased from an initial 370 to 807 vehicles and trailers to equip the Enhanced Land Force, and acquire vehicles for the Overlander project. The vehicles have also been modified based on operational experience to provide additional protection to personnel;

- Armidale Class (June 2005) - Patrol Boat numbers increased from 12 to 14;

- Heavyweight Torpedo (March 2003) increased in scope to allow for acquisition of torpedoes from the US through an Armament Co-operative Project;

- Collins R&S (July 2001) - scope increased to reflect the full scope associated with the implementation of a reliable and sustainable platform; and

- Stand Off Weapon (May 2011) - Removal of the moving target capability from project scope.

• Transfers: This year no transfers were made, unlike prior years where significant transfers of the DMO budget were made from the MRH90 Helicopters and Air to Air Refuel projects to the Defence Support Group to fund the acquisition of facilities. This reflects the practice of Defence Groups being allocated funds for the provision of services (for example facilities) at project approval, rather than those funds being allocated initially to the DMO, as well as payment by invoice rather than internal transfers. Previously there had also been a transfer from ANZAC ASMD Ph2A to ANZAC ASMD Ph2B to replace the initial Very Short Range Air Defence (VSRAD) with a phased array radar system.

• Adjustments: No Budgetary adjustments occurred against projects in this year's report. However previous years saw Air to Air Refuelling and Wedgetail budget adjustment reductions of over $150m each primarily due to changes in the currency mix and indexation parameters to those applied at original budget approval.

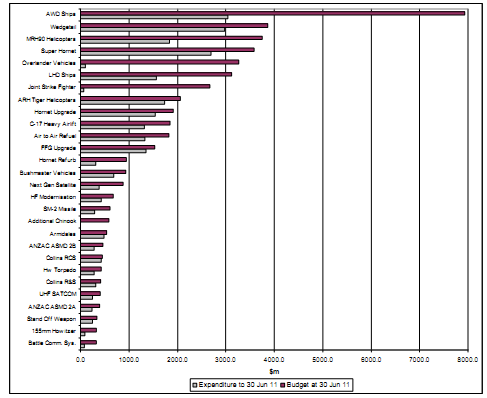

2.14 Figure 2.2 provides a comparison of expenditure as at 30 June 2011 compared to the total approved budget at that date. No project has exceeded its total approved budget. While this provides an indicator of project progress, the percentage of budget spent is dependent on the nature of the project and the level of early investment that may be required for project start-up and non- recurring engineering effort.

2.15 The relationship between project expenditure and project progress is not necessarily linear as this can be heavily influenced by the type of project, for example a developmental project would normally expend larger amounts of budget during the earlier phases whereas expenditure for a MOTS project is more likely to be linear in nature.

Figure 2.2 Comparison of Project Budget and Expenditure to Date (in $m)

2.16 The profile of expenditure against total approved budget is determined by several factors including the level of development and the type of acquisition. For example, a MOTS project acquired on a Foreign Military Sales (FMS) basis will generally have a linear expenditure pattern as FMS cases usually involve up-front quarterly payments. In comparison, a developmental project usually requires a degree of initial 'seed capital' on commencement with expenditure declining during the development phase and increasing as the project shifts into the build/integration phase.

2.17 Another key factor is the evolution of the project and its performance to date. Some projects may, for example, be well advanced but show a low level of expenditure against their total budget. This may result from poor contractual performance culminating in withholding of payments against specific milestones. This is, in effect, a deferral of payments that will be re- instated upon contractor achievement of milestones. Alternatively, unanticipated changes in project circumstances may also affect the level of project expenditure (e.g. Hornet Refurbishment had originally planned to replace 49 centre barrels but subsequent engineering and scientific work analysing airframe fatigue found that only 10 centre barrels required replacement. This will realise a significant reduction in expenditure against the project's approved budget).

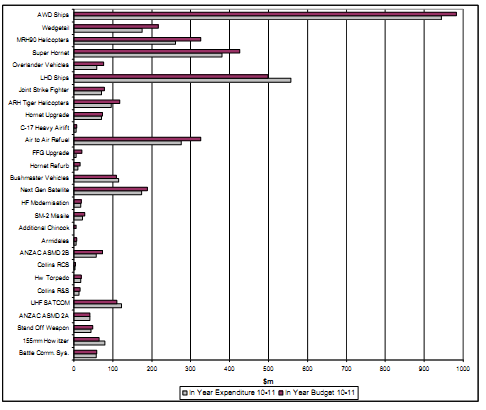

Figure 2.3 - Comparison of In-Year Budget Plan and Expenditure Actuals 2010-11 (in $m)

2.18 Figure 2.3 identifies actual expenditure achievement exceeding the1 budget year plan in 2010-11 for the following:

• LHD ships actual expenditure exceeded plan by $59.7m mainly resulting from the early completion and payment of milestones Build Sequence 1 and 2 for LHD 2.

• Bushmaster Vehicles year to date variance of $6.6m was mainly due to early delivery of composite armour design, early completion of the Tamworth facility and early delivery of vehicles.

• 155mm Howitzer $14.9m variance was primarily due to accelerated Foreign Military Sales payments for the Lightweight Towed Howitzers, early delivery of radios, rescheduling of vehicle integration activities to 2011-12 and foreign exchange adjustments.

____________________________________________________________________

193 Large variances of over $100m are attributable to the amount of project funding remaining at the time of out-turning against a large remaining budget.

194 The negative adjustment is a correction against the out-turned component of the budget.