1.3 EU Structural Funds grants

The Commission makes EU Structural Funds available to support the cohesion policies of the Union and individual Member States. The respective Managing Authority of the Member State processes these grants. In most cases, the public entity is interested in combining such grants with PPPs because it wishes to source the necessary co-financing from private funds and/or it sees value in an off-balance sheet treatment of the underlying asset. When assessing the mechanics of combining the grants with PPPs the respective Managing Authority would normally work in cooperation with the public sector entities involved in the procurement of PPPs.

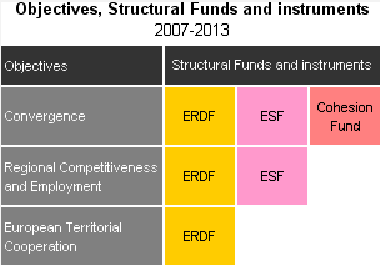

Structural Funds and Cohesion Fund The Structural Funds and the Cohesion Fund are funds allocated by the European Union as part of its regional policy. They aim to reduce regional disparities in terms of income, wealth and opportunities. Europe's poorer regions receive most of the support, but all European regions are eligible for funding under the policy's various funds and programmes. The Structural Funds are made up of the European Regional Development Fund (ERDF) and the European Social Fund (ESF). New objectives have been defined for the current programmes, which run from 1 January 2007 to 31 December 2013. The overall budget for this period is EUR 347bn: EUR 201bn for the European Regional Development Fund, EUR 76bn for the European Social Fund, and EUR 70bn for the Cohesion Fund.

|

The Structural Funds grants offer the largest amount of funding that is potentially available to PPPs, both as a whole and on a project basis. They can come either as a defined percentage of construction costs of non-revenue generating projects (e.g. un-tolled roads) or a variable grant to bridge the funding gap in revenue-generating projects (e.g. waste incinerator, toll road). Where an economically worthwhile project which generates some revenue is, nevertheless, unable to meet the whole of its costs from user charges, it can apply for EU grants. The maximum grant is the amount that is sufficient to make the project financially viable. This is known as the 'funding gap'. The beneficiary of the grant has to be a public sector entity but the funding can subsequently be made available to private partners in a PPP provided certain key principles are observed (i.e. mainly procurement and state aid rules)5. This instrument does not necessarily reduce the credit risk of the underlying project, but without such a grant, the project would not be feasible as PPP. A good example would be the Greek Rion Antirion Bridge.

Structural Funds grants are also made available as non-repayable contributions, but the rules that allow applying them in PPPs are very different from TEN-T funds and they are managed by different counterparts on both sides of the application process.

_________________________________________________________________________________

5 This is at least established practice, although the rules do not seem to prohibit explicitly grant applications directly by the private sector.