The impact of cutting equipment numbers

2.5 As discussed, the Department undertook a strategy to reduce the number of units being purchased, compared with the numbers the Department said it required when the main investment decision was taken. The Department can reduce equipment numbers in response to changes in military requirements, such as reducing numbers to enhance performance in the remaining feet, but most often it is done to avoid cost increases.

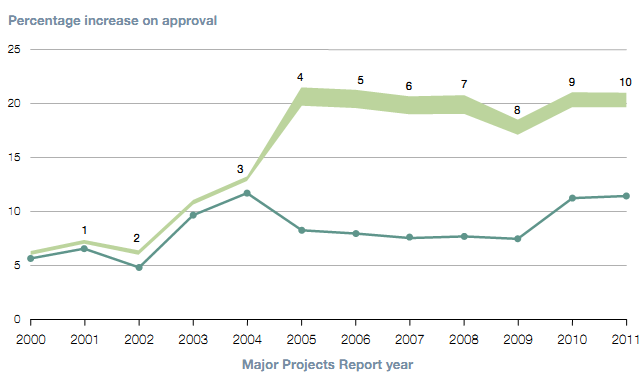

2.6 Figure 9 on page 21 shows the potential effect on total forecast cost since 2000, had numbers being purchased not been reduced. If the Department had purchased the numbers it originally intended at the time of the main investment decision, an extra £7.6-£8.8 billion would have been spent. This would have been in addition to the £10.6 billion noted in paragraph 2.2, theoretically increasing the total overspend to between £18.2-£19.4 billion - depending upon assumptions of the unit production cost of some equipment. This would have increased the total cost growth on projects from 11.4 per cent (Figure 7) to 19.6-20.9 per cent, above the level at which they were approved.

Figure 8 |

|

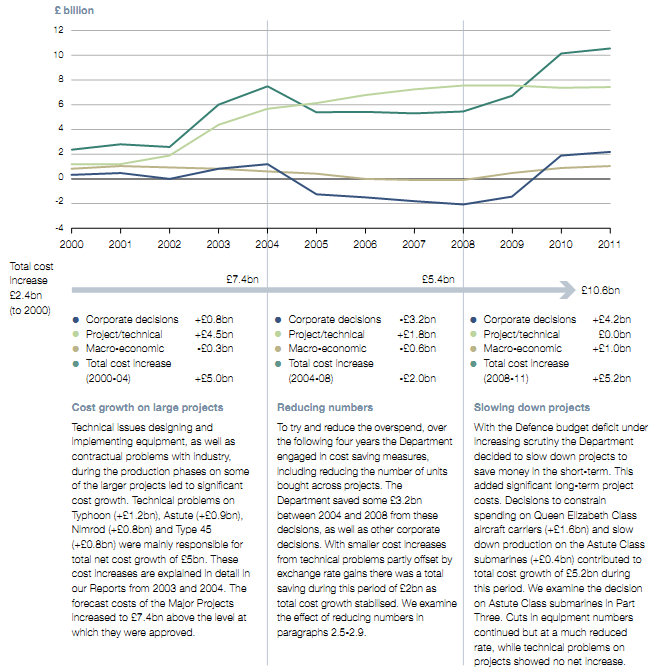

NOTES 1 The decision to slow down production on the Queen Elizabeth Class aircraft carriers was examined in Major Projects Report 2010. 2 Costs have been calculated by grouping the variation causal factors as reported in project summary sheets. A summary of these and details as to how they have been classified can be found in Appendix Four. 3 All projects that have passed their main investment decision are included in the analysis. The only exceptions being for Multi-Role Armoured Vehicles and Extended-Range Ordnance/Modular Charge System which have been excluded in the year in which they were cancelled. 4 The cost increase of £2.4billion relates to cost increases before 2000 and is part of the total cost increase of £10.6 billion. Source: National Audit Office analysis of Departmental data |

Figure 9 | ||||||||||||

| ||||||||||||

| 6.3 | 7.3 | 6.4 | 11.0 | 13.2 | 21.4 | 21.1 | 20.6 | 20.7 | 18.4 | 21.0 | 20.9 |

| 5.6 | 6.5 | 4.8 | 9.5 | 11.7 | 8.3 | 8.0 | 7.5 | 7.7 | 7.4 | 11.2 | 11.4 |

Key Equipment Cuts 1 Tornado Mid-Life Update 2 Nimrod, Sting Ray Lightweight Torpedo 3 Bowman 4 Typhoon, Support Vehicles, Nimrod, Sting Ray Lightweight Torpedo, Guided Missile Long Range System, Beyond Visual Range Air-to-Air Missile 5 Bowman, Panther, Guided Missile Long Range System 6 Guided Missile Long Range System 7 Beyond Visual Range Air-to-Air Missile 8 Nimrod, Lynx Wildcat 9 A400M, Typhoon 10 Puma Life Extension Programme | ||||||||||||

NOTES 1 The cost of projects, had the original numbers of units been bought, has been estimated using the 'unit production cost' from the project summary sheets. The lower estimate is based on the unit production cost when the equipment numbers were cut. The higher value is based on the unit production cost in the year the project was last covered by the Report. Where this is not available the unit production cost has been taken from the latest asset delivery schedule from when the project was last covered by the Report. 2 The effect of decisions is shown when it was reported in the Major Projects Report. This may not necessarily be the year in which the decision was made. For example, Major Projects Report 2009 reported that numbers were reduced on the Nimrod maritime patrol aircraft (12 to nine) but the decision was taken in the spring of 2008. 3 The projects shown are where significant numbers were cut. There are further projects where numbers were cut, which are not shown. 4 The decision to reduce the United Kingdom's buy by 88 aircraft and remove funding (£978 million) from the Typhoon aircraft project was reported in 2005. However, in 2010, the Department decided to purchase 16 of the 88 aircraft as part of an additional £2.65 billion commitment to the Typhoon programme. Both these decisions are reflected in the above chart. Source: National Audit Office analysis of Departmental data | ||||||||||||

Range of cost variation

Range of cost variation  Total cost variation

Total cost variation2.7 As noted by the Public Accounts Committee in 2005, cutting equipment numbers is an inevitable consequence of poor performance in controlling costs.14 The Department has also made decisions to cut equipment numbers as the military requirement or capability priorities have changed. Although Figure 9 illustrates how the Department has avoided further cost growth through these decisions, this can be at the expense of value for money, demonstrated through our unit cost analysis.

2.8 Defence projects tend to include significant development costs and the effect of reducing numbers is to share these non-recurring costs across a smaller number of production units. Therefore, reductions in numbers after the main investment decision has been made tend to be economically inefficient as this may include significant development costs. A unit production cost, which excludes these development costs, is an alternative measure preferred by the Department which generally remain stable following reductions in numbers.

2.9 Figure 10 shows the impact on unit cost of reducing numbers across projects where numbers have been cut. For example, numbers reduced by 57 per cent on the Nimrod maritime patrol aircraft while unit cost increased by 199 per cent. Had the project not been cancelled in 2010 each Nimrod would therefore have cost, on average, £266 million more than originally intended at the main investment decision.15

______________________________________________________________________________________________________________________

14 House of Commons Committee of Public Accounts, Ministry of Defence Major Projects Report 2005, Fiftieth Report of Session 2005-06, HC 889, Part One.

15 The Department was not able to provide a comparison for the change in unit production cost of the Nimrod aircraft, although it is likely it would not have changed substantially.