The Public Sector Comparator (PSC)

The PSC was one of a range of assessment criteria utilised during a Partnerships Victoria procurement process. The PSC estimates the hypothetical risk-adjusted cost if a project were to be financed, owned and implemented by government. The PSC is also based on the most efficient form and means of government delivery.

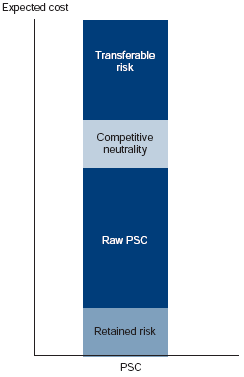

Figure 4B sets out the four components that make up the PSC cost.

Figure 4B Components of the PSC

Source: Partnerships Victoria PSC Technical Note June 2001, page 6, section 2.4.

Figure 4C defines each element of the PSC.

Figure 4C Definition of PSC Components

Retained risk Retained risk is any risk not to be transferred to a bidder. The cost of retained risk is included to provide a comprehensive measure of the full cost to government in a PSC. Examples of retained risk are planning permission or cultural artefacts. Raw PSC The raw PSC provides a base costing under the public procurement method. This includes all capital and operating costs, both direct and indirect, associated with building, owning, maintaining and delivering the service (or underlying asset) over the same period as the term under the Partnerships Victoria proposal and to a defined performance standard as required under the output specification. Competitive neutrality Competitive neutrality adjustments remove any net competitive advantages that accrue to a government business by virtue of its public ownership. This allows a fair and equitable assessment between a PSC and bidders. Transferable risk Transferable risk is any risk transferable to a bidder. Examples of transferable risk are construction costs, construction delays and materials cost escalation. |

Source: Partnerships Victoria PSC Technical Note June 2001, page 7