ANNEX A IFRIC 12 - a brief overview

This annex provides a brief overview of Interpretation 12 Service Concession Arrangements (IFRIC 12), which was issued by the International Financial Reporting Interpretations Committee in November 2006. It gives guidance on the accounting by operators (the private sector) for public-to-private service concession arrangements. IFRIC 12 does not cover accounting by the grantor (the public sector).

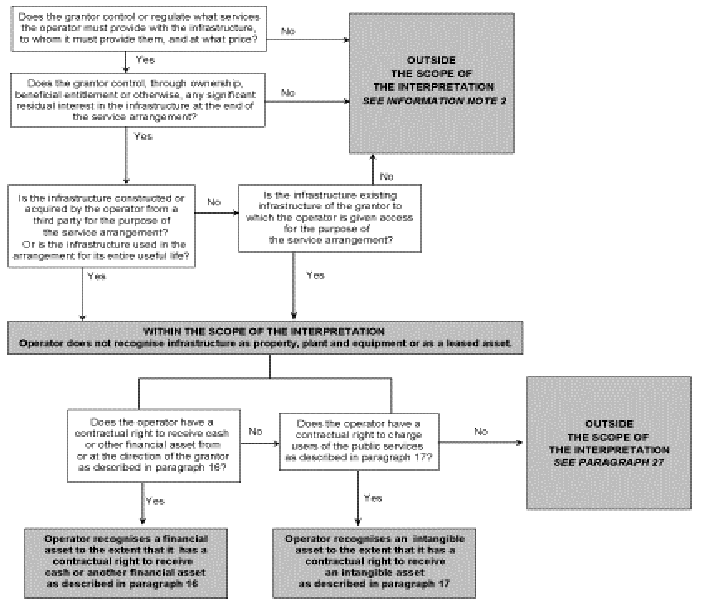

IFRIC 12 states that it is control that determines the accounting treatment by the operator. If the grantor retains control, then the infrastructure asset is not an asset of the operator. This suggests that the infrastructure asset becomes or remains (depending on how the infrastructure asset is provided) an asset of the grantor. The flowchart below, taken from IFRIC 12 (paragraph references in the table are to paragraphs in IFRIC 12), shows how the operator can determine whether or not the concession arrangement is within the scope of IFRIC 12.

IFRIC 12 applies to service concession arrangements if (paragraph 5 of IFRIC 12):

(a) the grantor controls or regulates what services the operator must provide with the infrastructure, to whom it must provide them, and at what price; and

(b) the grantor controls - through ownership, beneficial entitlement or otherwise - any significant residual interest in the infrastructure at the end of the term of the arrangement.

Paragraph 6 of IFRIC 12 notes that infrastructure used in a public-to-private service concession arrangement for its entire useful life is within the scope of IFRIC 12 where the condition in IFRIC 12.5(a) is met. That is, even if the grantor does not have any significant residual interest in the infrastructure at the end of the arrangement, but controls the services, to whom they are supplied and the price during the arrangement, then the infrastructure does not belong to the operator. The inference is that it will belong to, and be accounted for, by the grantor.

The Application Guidance to IFRIC 12 provides further guidance on what type of arrangement might fall into the scope of IFRIC 12.