FINANCIAL REPORTING OF PFI CONTRACTS

2.21 The Government only uses PFI where it offers value for money, considered over the long term. Its approach to the use of PFI is detailed in Chapter 3. The financial reporting and balance sheet treatment of projects are subsequent and irrelevant to the decision whether to use PFI, but the monitoring and reporting of financial commitments made under PFI is an important part of managing the public finances.

2.22 The Government publishes its estimates of the unitary charge payments - single annual payments made by the procuring authority to the private sector which cover all the costs, both capital and service, of PFI projects - to be made under all signed PFI contracts in the Financial Statement and Budget Report. These payments represent the full price of the specified facility being made available and cover all costs over the life of the contract. These Departmental commitments of future revenue are monitored by Government, included in consideration of future budgets, and therefore taken into account by Departments in deciding how much PFI investment to undertake.

2.23 PFI unitary charges include payments to cover the cost of capital expenditure (money to repay the debt and interest charges, including hedging costs, incurred in building a large capital asset), the services needed to run and repair that asset, like maintenance work and supporting soft services like catering, cleaning and hospital portering. In a typical PFI hospital, payments for services make up 40-50 per cent of the unitary charge. For a typical PFI schools project, around 30 per cent of the unitary charge goes toward caretaking, maintenance and other services. If a project is built using conventional procurement, these future costs for services are not automatically covered, monitored or disclosed. Reporting estimated payments under PFI contracts therefore provides a fuller picture of future commitments than would be possible under conventional procurement, and provides better information for the management of future budgets.

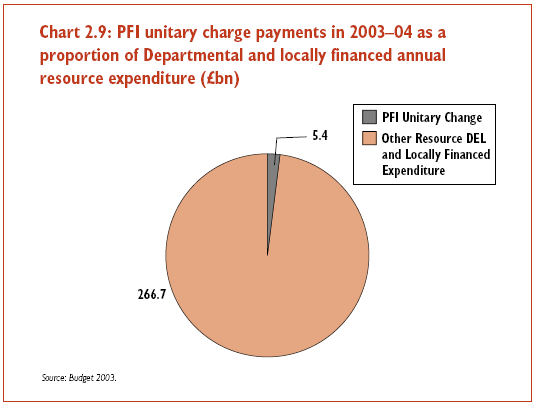

2.24 These annual payments under PFI unitary charges make up a very small proportion - just over 2 per cent - of total annual resource budgets, as illustrated in Chart 2.9. Consequently, they represent very little threat to the flexibility of the Government's budgets, and a small commitment of future revenue.

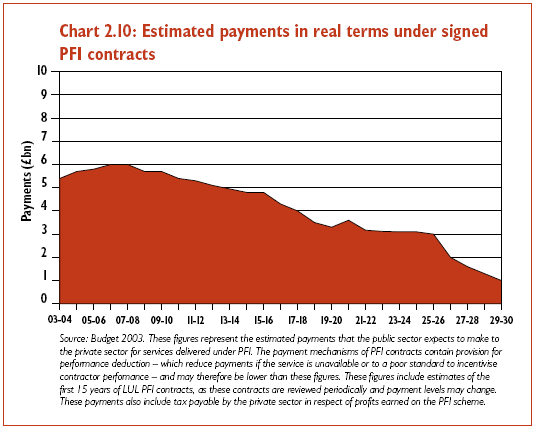

2.25 This conclusion, that PFI presents little threat to overall budgetary flexibility, remains true into the future. Because the cost of PFI unitary charges in the future is clear, and transparently reported, the Government is able to take it fully into account in future budgeting. In fact, as illustrated in Chart 2.10, the estimated payments under signed PFI contracts begin to fall after 2007-08. These figures obviously do not take into account unitary charge payments under future PFI contracts, however, if PFI investment remains the limited proportion of total investment it currently is, there is no reason to believe that these payments represent a long-term threat to overall budgetary flexibility.