4.1 Using the accounting treatment of PPPs for Eurostat's purposes

National statistical offices do not generally have sufficient resources to analyse and classify each PPP transaction entered into in their jurisdictions. For this reason, they are often constrained to rely on adjusted figures derived from the accounting treatment of PPPs.

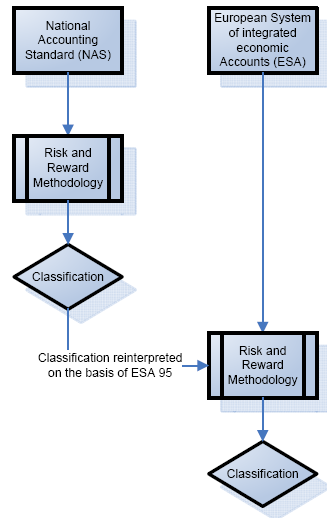

The statistical offices normally rely on the work of national accountants for the asset classification carried. Asset classification for the purposes of the accounting treatment of PPPs has historically been based, in the majority of EU countries, on a "risk and reward" criterion. In principle, this is not dissimilar to the requirements set out in ESA 95. However, whilst the rules of ESA 95 are often similar to that of accounting, they are not necessarily identical: each country has a methodology to determine when "sufficient" or "most risk" is transferred to the non-government partner. This potentially undermines the principle of comparability between countries which ESA 95 is seeking to achieve. For this reasons, the data derived from the accounting treatment of PPPs has to be adjusted to reflect such differences. This adjustment is carried out by national statistical offices.

Practical application of ESA 95

using data provided by the accounting treatment of PPPs

at the national level