A stronger role for corporate governance

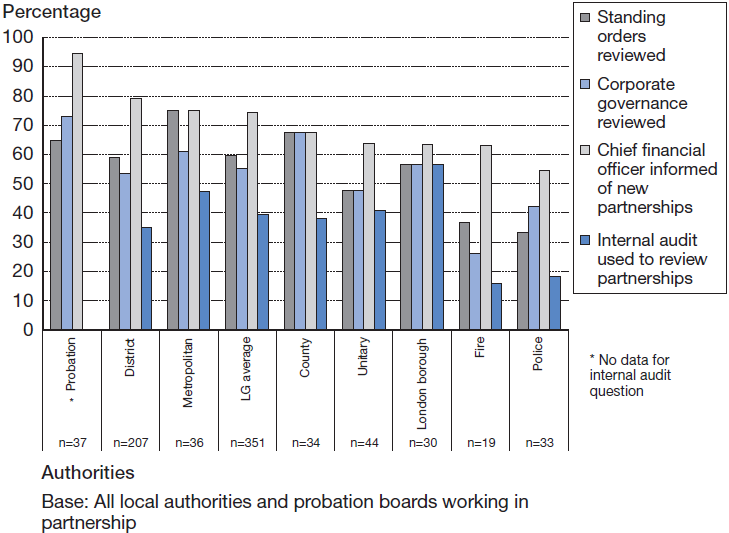

140 Where partnerships are not corporate entities, their separate governance arrangements cannot mirror the detail found in corporate bodies. In the absence of formal governance arrangements, responsibility for supporting the governance of partnerships falls to partners' own corporate governance mechanisms. Most public bodies have clear structures and systems to support better corporate governance. However, the links between these and the governance processes involved in partnerships are often missing or unclear (Figure 13).

141 Public bodies need a scheme of delegation that makes clear who can take decisions on their behalf, the extent of their authority and how decisions will be reported back. Public bodies must scrutinise the decisions that partnerships take. There should be formal links between an organisation's scrutiny and internal audit functions and its key partnership activities. For example, in local authorities, the health scrutiny function and the overview scrutiny function provide good opportunities to investigate issues connected with their power to promote well-being. Councils can use this wide power to create specific partnership scrutiny panels. The Audit Commission's view is: (Ref. 19)

'If local authority scrutiny of health works well, it will provide a valuable forum for review and debate, engage local people and generate realistic suggestions to improve services. Done badly, it could duplicate effort, damage partnerships and result in little more than political point scoring.'

142 Internal audit processes, and documents such as the Statement on Internal Control, should cover the activities of important partnerships. Internal audit should consider the risks attached to partnerships and report on the links between corporate and partnership activities. The Statement on Internal Control does not require explicit reference to partnerships or joint working. It does require the chief executive (and leader for local authorities) to state that there is a system of internal control in place that is designed to ensure that key risks are managed. This should always include risks in relation to partnerships.

Figure 13 Many local public bodies should review organisational processes to support working in partnerships. |

|

Source: Audit Commission, 2004 |

143 In order to manage risks effectively, an organisation's corporate governance systems and processes should address partnerships. This is particularly important in terms of risk management, performance management and financial management. The patchy quality of corporate governance across the public sector presents a potentially serious obstacle to sound risk management (Ref. 20). Poor corporate governance in one key partner will jeopardise the governance of the partnership overall. Organisations that are considering working in partnerships should take a view about the quality of their own and their partners' corporate governance arrangements. If possible, this should be a joint exercise, so that all partners address any weaknesses. This task may be difficult and sensitive, but it is vital.