NPD Surpluses

Under a NPD structure, surpluses are distributed for the benefit of the public sector or wider community. Where surpluses are available for distribution within the shadow bid model, this cash flow should be taken into account in carrying out the Value for Money assessment. The cash flow from surpluses should be risk-adjusted to reflect the likelihood that it will occur and discounted back using the discount rate specified within the Treasury's Green Book, consistent with the Unitary Charge cash flow. Further information on the NPD structure is available online at: http://www.scotland.gov.uk/Topics/Government/Finance/18232/NPDExpNote

Where the Value for Money margin of an NPD procurement relies on the receipt of the surpluses defined in the shadow bid model, the Procuring Authority should ensure that the Project will also deliver Value for Money on qualitative grounds in accordance with the VfM guidance.

The preference of the Procuring Authority for receiving a defined level of surpluses should be considered alongside the efficiency of generating the level of surpluses required. If the level of surplus required from the NPD model is artificially high, the Unitary Charge will increase to reflect this and the model is likely to become inefficient.

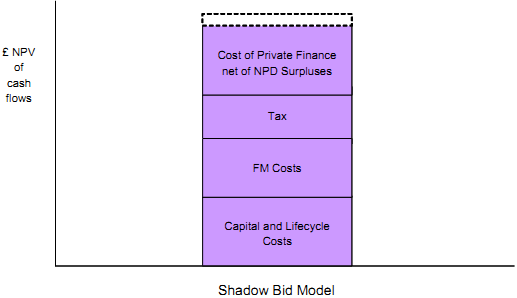

Figure 4: Shadow bid model step 1: quantify project costs