Competitive bidding

2.6 London Underground's decision to create three Infracos aligned with the preference aired during consultations across various market sectors in the summer of 1998. For all three Infraco concessions there was competitive bidding through to the appointment of preferred bidders - although this was not initially the case for the Infraco SSL contract.

2.7 At an early stage, both the Department and London Underground viewed Railtrack, then owner of the national railway infrastructure, as a dominant bidder likely to affect competition adversely. London Underground dealt with this by engaging Railtrack in exclusive negotiations for Infraco SSL, after Railtrack had made a strategic case for integrating the sub-surface lines into the national railway. In exchange, Railtrack agreed not to bid for Infraco BCV and Infraco JNP whose deep tube concessions included extensive tunnels.

2.8 London Underground, in July 1999, sought expressions of interest in the two deep tube concessions by advertising in the Official Journal of the European Communities. In response, six consortia, comprising 26 companies, were formed. But by late 1999, however, the negotiations between London Underground and Railtrack for Infraco SSL broke down. Subsequently in December 1999, London Underground announced that it was running a competition for Infraco SSL and received expressions of interest from five consortia.

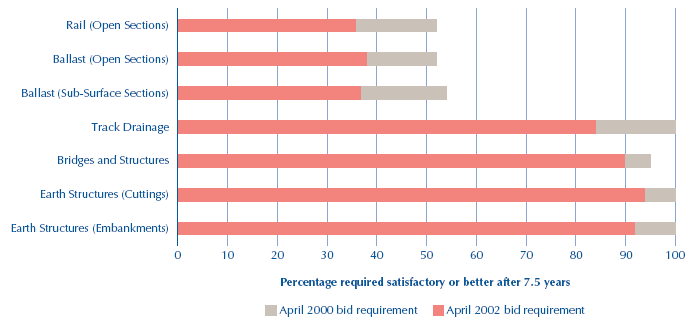

2.9 London Underground knew that despite investigations by its own advisers, Ove Arup, and investigative work by bidders, the condition of less accessible fixed assets (tunnels, some embankments, bridges etc.) would not be known before award of the contracts, and in some cases not before the end of the first 7½ year period (Figure 7). The uncertainty meant that bidders sought protection from the consequences of adverse conditions exceeding prudent levels of contingency. They were particularly concerned because London Underground envisaged the Infracos taking full 30 year responsibility for the design, procurement strategy and decision-making in support of infrastructure renewal and upgrade activities.

|

7 |

|

Required condition by asset class |

|

|

|

|

|

|

|

NOTE LU classify asset conditions on a scale of A-E, where A, B and C are satisfactory or better; D means heavy maintenance or replacement/ overhaul is needed; and E requires frequent inspection or removal from service until fixed. This figure shows, for different asset types, the PPP bid requirement for the proportion to be made satisfactory (condition A-C) within 7.5 years in April 2000 and April 2002. The variations depend on the underlying baseline: for example, 85-90% of drainage assets were classed as A, B or C in shadow running years. Grey assets (see glossary) are provisionally classed as satisfactory unless engineering judgement indicated otherwise. Source: London Underground |