But few authorities have rights to share in refinancing benefits

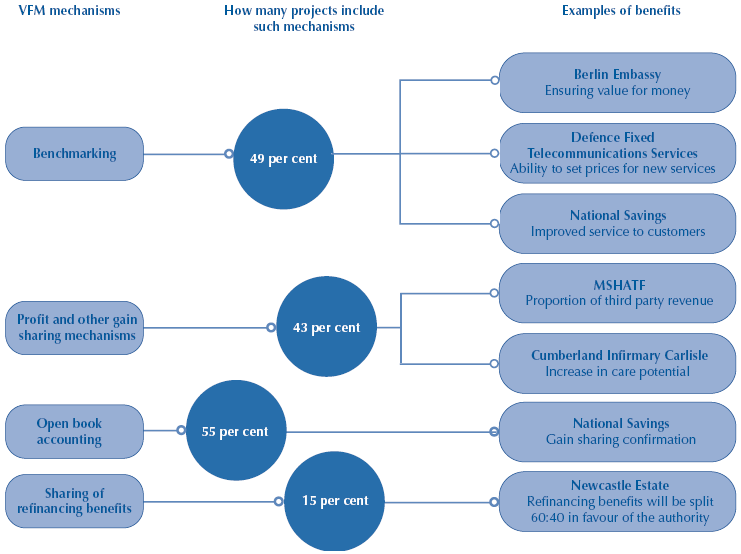

1.30 As was highlighted in our report on the refinancing of the Fazakerley PFI prison contract4, and the subsequent report by the Committee of Public Accounts5, the perceived value for money of a project can be affected if a contractor receives significant windfall gains as a result of refinancing a PFI project. Only 15 per cent of authorities, however, told us that they had the right to share in refinancing benefits. Other authorities may, nevertheless, have other contractual rights which could enable them to negotiate over sharing refinancing gains. This was the case in the refinancing of the Fazakerley prison project where the

8 |

| Examples of the benefits derived from VFM mechanisms |

|

|

|

|

| Source: National Audit Office survey of authorities |

Prison Service had the right to approve the increase in its termination liabilities arising from the proposed refinancing. This gave it an opportunity to negotiate a share of the contractor's refinancing gains.

1.31 Guidance on refinancing in the Treasury's Standardisation of PFI contracts published in 1999 said authorities should seek a share of refinancing gains only in limited circumstances. Following the recommendations of the Committee of Public Accounts the Office of Government Commerce is preparing revised guidance, which is likely to recommend that refinancings should always be subject to authority consent and that contracts should give authorities approval rights over refinancings and contain provisions on sharing gains.

1.32 55 per cent of the contracts we surveyed had provisions for open book accounting. As well as helping authorities to understand the contractor's financial position and determining the outcome of any profit sharing arrangements, open book accounting can also enable an authority to work in a collaborative manner with its contractor. For example, National Savings takes care, when planning a marketing campaign, to time it to run when there is a trough in Siemens' workload so as to even out Siemens' costs.

1.33 Open book accounting could also help a contractor to draw to the attention of an authority any problems to which the contractor believes the authority has contributed. For example, one contractor told us that it had incurred additional costs because the authority had ordered a new service but did not deliver sufficient users of the service to generate the expected additional revenues for the contractor to offset the costs of developing the service. Another contractor said the authority sometimes asked for a new service to be developed but then changed its mind.

____________________________________________________________________________

4 The National Audit Office's report on the refinancing of the Fazakerley prison PFI contract HC584 (1999-2000)

5 Committee of Public Accounts: 13th Report, 2000-01, HC 372, The Refinancing of the Fazakerley PFI prison contract