Expert panel consultation

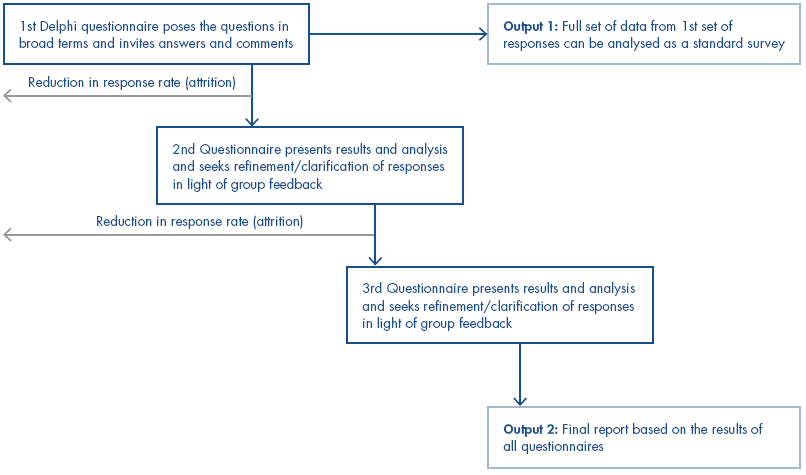

We convened an expert panel. The consultation was undertaken via an email survey following a simplified Delphi process. Three rounds of questionnaires were used in total. The first posed questions in broad terms; the second questionnaire presented our analysis of the issues arising and asked for further feedback. The third round comprised a discussion paper, circulated mainly for high level comment. Delphi consultations are typically used to identify or predict future developments. This was used to provide additional insight into how the Department's approach to PFI may affect a programme of long term projects. This was the first time this method had been used by the NAO.

25 | Delphi Panel | |||

|

|

|

| |

Public Sector | Other stakeholders | |||

■ Audit Commission ■ South East Centre for Excellence Waste Contractors | ■ Environmental Services Association ■ Friends of the Earth Europe ■ unison | |||

■ Biffa ■ Viridor | ■ Chartered Institute of Wastes Management | |||

■ SITA |

| |||

advisers and funders |

| |||

■ Mott MacDonald |

| |||

■ Bevan Brittan |

| |||

■ Trowers Hamlins |

| |||

■ Walker Morris |

| |||

■ HBOS |

| |||

■ Bank of Ireland |

| |||

■ Scott Wilson |

| |||

■ SLR Consulting |

| |||

■ Barclays PFI unit |

| |||

■ Deloitte & Touche |

| |||

■ Ernst & young |

| |||

Source: National Audit Office | ||||

The findings of the panel were used to develop a theoretical model of how PFI could be used under ideal circumstances, based on elements of consensus from a diverse panel of experts. They were also used to populate our Issue Analysis throughout the audit, to identify key areas of risk in obtaining value for money from the use of PFI in Waste Management and to triangulate our findings later in the study.

The panel was a purposive sample derived from desktop research into organisations active in the waste PFI market in the broadest sense. The purpose of the sample was to provide a deliberately varied and diverse range of viewpoints, in order to identify where consensus could be derived, if at all. Where possible, existing contacts were used.

26 | Overview of the expert panel consultation process |

|

Source: National Audit Office | ||