A good price for financing was obtained

2.20 In redeveloping the 2 Marsham Street site, the financing for the office development has been kept separate from the financing for the residential/commercial development. The latter development has been financed by a £45 million corporate loan from HSBC to AGPRD. This section examines the financing associated with the office development for the Home Office.

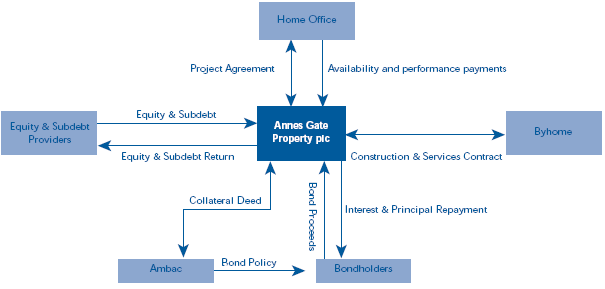

2.21 Figure 10 overleaf shows the structure of the deal. Anne's Gate Property plc consortium consists of HSBC Infrastructure Limited and Byhome Limited (Byhome is majority owned by Bouygues UK and minority owned by Ecovert FM during the construction phase and this will reverse during the operational period. Both are wholly owned by Bouygues Construction S.A.). Byhome's performance is also underwritten by Bouygues Construction SA. It is responsible for the construction of the office development and then the subsequent provision of building management and other support services directly to AGP, and indirectly to the Home Office within the building.

2.22 The bulk of the financing for the construction of the project comes from a bond issue in March 2002. Equity investment predominantly comes from secured loan stock (subordinated debt) provided by HSBC with a small amount of pure equity from both HSBC and Byhome. The amount of each funding source for the project is shown in Figure 11 overleaf.

10 |

| The Structure of the PFI deal |

|

|

|

|

| Source: National Audit Office |

11 |

| AGP Funding Sources | ||

|

| Funding Source | Amount (£ms) | percentage |

|

| 3.237 per cent Index-Linked Guaranteed Secured Bonds due 2030 | 144.22 | 48.5 |

|

| 5.661 per cent Guaranteed Secured Bonds due 2031 | 100.00 | 33.6 |

|

| Equity: Subordinated debt (Secured Loan Stock) | 28.5 | 9.6 |

|

| Pure equity | 0.64 | 0.2 |

|

| Property disposal proceeds (Sales of surplus land to AGPRD) | 11.00 | 3.7 |

|

| Revenue during construction | 2.86 | 1.0 |

|

| Interest income (Predominantly through reinvestment of bond proceeds in a Guaranteed Investment Contract) | 10.23 | 3.4 |

|

| TOTAL | 297.44 |

|

|

| Source: National Audit Office |

|

|