The Performance Management System

3.22 The Performance Management System is the main lever for monitoring performance (Figure 3 on page 17). These systems are a vital and helpful tool for contract managers that provide incentives for contractors to perform to the specification required and acts as a lever to drive performance. We found:

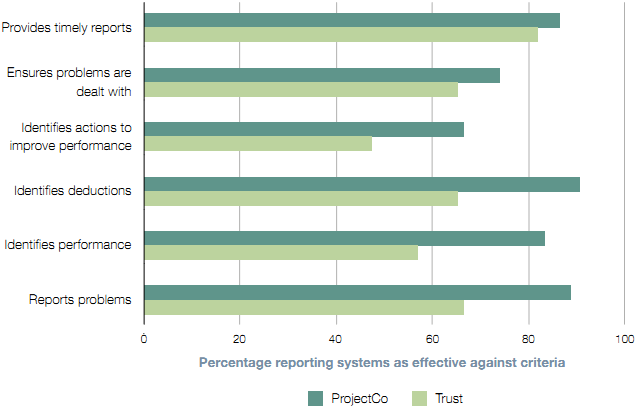

a Trusts are moderately enthusiastic about the effectiveness of the systems. Forty-seven per cent agreed the systems complied with five of the six key aspects we identified as objectives of a good Performance Management System, although only 28 per cent thought their systems complied with all six (Figure 14 on Page 33).

Figure 13 In general Trusts and Contractors have positive relationships

|

We asked Trusts to rate their relationships against seven key aspects of a good relationship. These were: Understanding of key business drivers: We have a mutual understanding of all relevant issues about the contract and services being delivered and each other's business needs and goals. Conduct and behaviour: We talk to each other openly and honestly, at all times, on all issues; we have implicit faith in each other's professionalism and integrity. Responsibilities and commitments: We trust each other to meet our respective responsibilities and deliver what has been agreed. People: There is mutual trust, confidence and respect at all levels; we are confident in the people we work with; and we are consulted about staff performance. Continuous improvement: All parties view the relationship as one team, although we recognise our different responsibilities within the team. We continuously seek to improve our team performance and relationship. Flexibility and responsiveness: All parties always respond quickly and supportively. Staff replacements: We are consulted about staff replacements, and staff turnover has little impact on our relationship. NOTE 1 -2 equals the relationship falls well short of the best practice statement and 2 equals relationship fully matches up to the best practice statement. Source: National Audit Office Survey of Trusts |

Figure 14 Trusts are moderately enthusiastic about the effectiveness of their Performance Management Systems Criteria

Source: National Audit Office Survey |

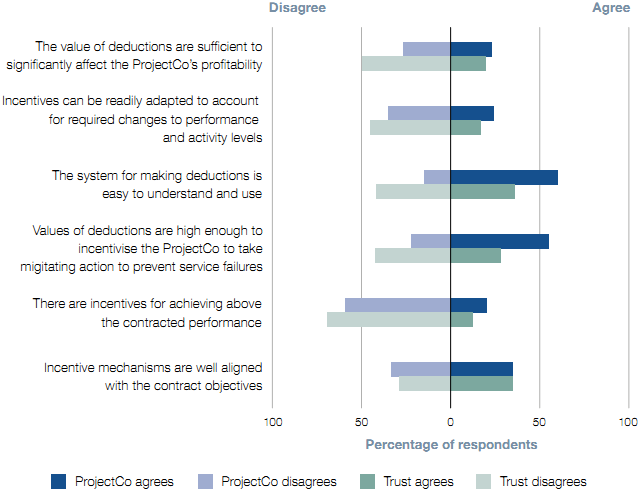

b Individual performance indicators could be improved, but together provide each Trust with an overview of performance. Most Trusts are positive about most targets, although 45 per cent stated that their systems contained performance indicators that did not meet all of our good practice criteria (Figure 15 overleaf). Seventy-seven per cent of Trusts say their Performance Management System is effective at reporting performance (Figure 14). c Most Trusts verify the accuracy of performance reports. Contracts are designed to be 'self-reporting': the contractors provide the performance information in the Performance Management Systems. But Trusts have a responsibility to verify the information, by sample checking the data, to ensure they are getting the level of service required. Two of our eight case studies, however, carry out no auditing of the data. We also believe some Trusts do not have enough contract management staff to monitor performance (paragraph 3.6). d The Performance Management Systems do not always provide sufficient incentives to improve performance. Deductions are not intended to reimburse Trusts for the full effects of poor performance. But deductions are sometimes too small to drive performance. For example: • East Lancashire Hospitals levied a deduction of 47 pence for a failure to fix a tap within the set timeframe. • At Hereford County Hospital, the contractors told us they decided it was cheaper to receive a deduction than provide an alternative cooling system to keep an operating theatre open whilst they repaired the main system. • Some systems only penalise initial failures. Oxford Radcliffe's contract allows only one deduction for specific portering failures in an eight-hour period. Thus there is no incentive to meet targets following an initial failure. Many Trusts and ProjectCos are sceptical that their systems and deductions provide sufficient incentives to contractors (Figure 16). |

Figure 15 Most Trusts are positive about most targets

|

We asked Trusts to assess their contractual targets for maintenance, cleaning, catering, portering and laundry against the following criteria: Objective and measured - i.e. based on a quantifiable standard of performance that does not require judgement; Focused - i.e. a set of only a few indicators which set clear incentives and priorities and not a long list of unconnected indicators; Detailed - i.e. set out in sufficient detail to capture the required service level; Auditable - i.e. you have a way of checking that the data provided by the contractors against the indicator is accurate; and Provide the right incentives - i.e. incentives capture all the required tasks and subcontractors cannot meet targets by doing things you do not want. Source: National Audit Office survey |

e a few trusts do not charge the deductions they should. Our survey identified six Trusts (8 per cent of those who responded) who stated that they had not charged deductions to which they were entitled, because they thought it would affect their relationship with their contractor or not improve performance. Two of our case study Trusts had suspended the use of their Performance Management System to give their contractors a chance to concentrate on specific aspects of performance. For example, we estimate Oxford Radcliffe Trust did not charge around £7,000 of deductions over the six weeks that their Performance Management System was suspended. The Committee of Public Accounts has said that public bodies should always apply financial penalties when contracts entitle them to do so, unless there are very exceptional circumstances why they should not.10 In the Trust's opinion, the benefit of improved performance delivered through the contractor focusing on overall performance rather than specific targets would be greater than the cost in terms of deductions not levied. |

Figure 16

Source: National Audit Office Survey |

___________________________________________________________________________________________

10 Public Accounts Committee 2008–09 Central government’s management of service contracts.