Increased termination liabilities

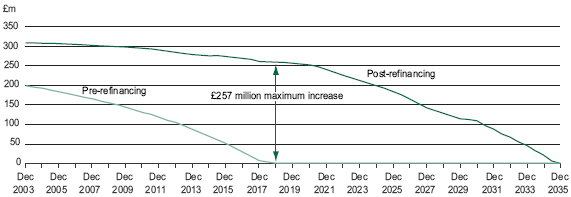

The amount the Trust would have to pay to end the contract early could increase by up to £257 million. If Octagon defaults on its contractual obligations, and the contract is ended by the Trust, the Trust will continue to pay monthly payments. These monthly payments will be related to the Trust's previous contractual payments for using the hospital and the costs of repaying Octagon's debt but reduced by any increased costs the Trust may incur in re-procuring the required services. The Trust's liabilities, following contract termination in these circumstances, are likely to cover most, but not necessarily all, of Octagon's outstanding debt. In other circumstances, if the Trust defaults, or chooses to end the contract, its liabilities will be the full amount of Octagon's outstanding debt, payable as a lump sum. The purpose of these contractual arrangements was to ensure that the Trust pays a fair amount for its use of the hospital if it wants to end the contract early. As the Trust's termination liabilities under these arrangements were linked to Octagon's debt, the liabilities rose in line with the increase in Octagon's borrowings on refinancing. The Trust did not, however, challenge this outcome in a situation where the increased borrowings were not being used to expand the hospital buildings which it was using. The £257 million maximum increase in these liabilities would arise if the Trust terminates the contract, without Octagon default, in 2018, fifteen years after the refinancing (Figure 4).

The Department considered these additional termination risks were justified on the grounds that it had not experienced any terminations on 46 large PFI projects which were operational. The Trust judged that, taking this experience into account, on the balance of probabilities, it would be value for money to obtain a 30% share of the refinancing gains on the terms Octagon had proposed. There is a risk, however, that changing circumstances over the next fifteen years could increase the likelihood of the Trust needing to end this contract early.10

Figure 4: Change in Octagon's outstanding debt and the Trust's maximum termination liabilities

Note: The Trust's termination liabilities would be payable as a lump sum equal to Octagon's outstanding debt if the Trust defaults on its contractual obligations or chooses to end the contract early (for reasons other than Octagon defaulting on its contractual obligations).

____________________________________________________________________________________________

10 C&AG's Report, Figure 12, p12; Qq 4-8, 14-17, 34-48