4.4.5 Fixed, variable and semi-variable costs

When forecasting future operating costs, it is useful to distinguish between fixed, variable and semi-variable costs. Figure 4-3 illustrates the relationship between total cost and unit service cost.

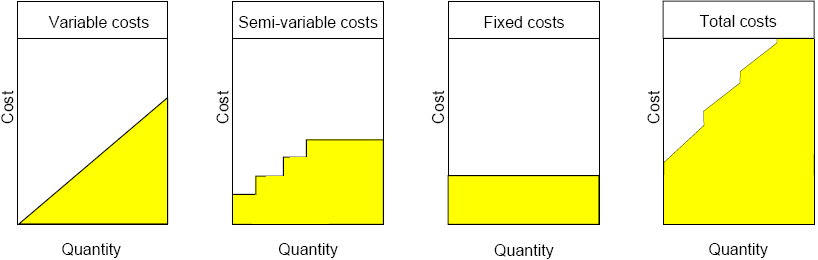

Figure 4-3 Operating cost components

Fixed costs are, in the short term, independent of the volume of services delivered. For example, in the provision of water treatment services, this may typically include lease charges on the required land.

The volume of services delivered drives variable costs. In the previous example this may include the cost of chemicals and agents in the water treatment process.

Semi-variable costs only increase after a threshold increase in the level of services has been reached and, as seen in Figure 4-3, will usually then taper off. In the provision of water treatment services example, this may include treatment filters, since higher water volume throughput may lead to greater filter usage.

The proportion of variable to total costs will influence also the sensitivity of the PSC to changes in operating assumptions. Section 6.6 discusses sensitivity analysis.

Forecasts of the expected direct operating costs in the Raw PSC should also reflect reasonably foreseeable improvements in service delivery or efficiency savings. This may be influenced by:

• increased efficiency, or familiarity with new service, or production techniques;

• economies of scale - if services are increased over the life of the Reference Project, or synergy is likely through integration with other infrastructure (ability to spread fixed costs over multiple product/project offering); and

• declining market cost of inputs (e.g. IT equipment).

For example, the types of direct costs that might be included in a typical accommodation services project are:

• direct capital costs:

buildings;

buildings;

refurbishment;

furniture; and

• direct operating costs:

council rates; and

building services.