EXECUTIVE SUMMARY

1 The National Physical Laboratory (NPL) is one of the world's leading laboratories working on the measurement of physical properties such as time, length and mass. It sits at the pinnacle of the UK's National Measurement System for which the Department of Trade and Industry (the Department) is responsible.

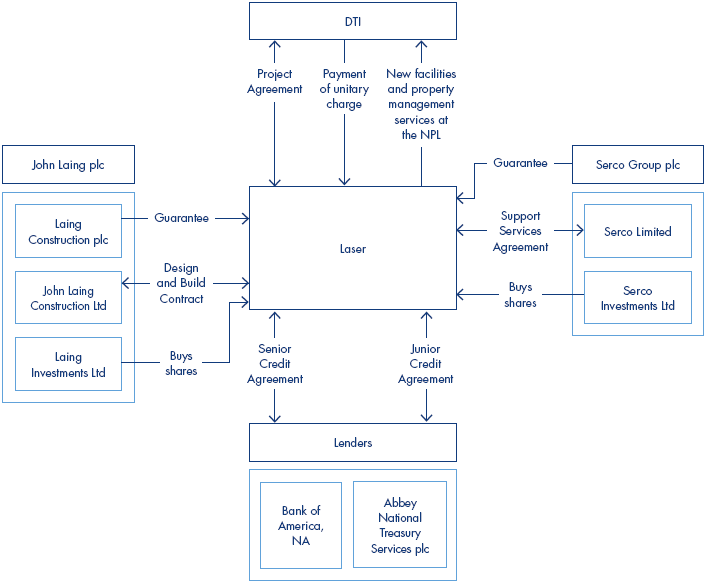

2 On 31 July 1998, the Department and Laser, a special purpose company jointly owned by Serco Group plc and John Laing plc, signed a 25-year long, Private Finance Initiative (PFI) contract. Under the contract Laser would build and manage new facilities for the NPL, comprising 16 linked modules, containing over 400 laboratories, and replacing many existing buildings. The planned cost of the new buildings was approximately £96 million,1,2 financed mainly by loans from Bank of America, NA; and Abbey National Treasury Services plc (the Lenders) (Figure 1 overleaf). The Department would pay Laser a unitary charge, of £11.5 million (1998 prices) a year once the new buildings were ready. The charge would be increased annually by a factor based on the increase in retail prices. At the end of the contract, the charge would cease and ownership of the buildings would pass to the Department.

3 The project suffered considerable construction delays and difficulties in achieving the specification for some parts of the buildings. These difficulties delayed the realisation of benefits associated with the new buildings, although mitigating action protected the quality of the scientific research conducted in the existing facilities. In December 2004, the Department and Laser agreed to terminate the PFI contract. The Department paid Laser £75 million for its interest in the new buildings, took over responsibility for completing some outstanding building works, and its liability to pay the unitary charge ceased. Laser passed the payment in full to the Lenders and is currently being wound up.

4 This was the first termination of a major PFI contract involving serious non-performance. We examined the Department's handling of the project and the lessons that might apply to other PFI projects. This report examines the problems that led to the termination, why these problems arose, how the Department managed them and the value for money consequences of the termination. Appendix 1 sets out our methodology.

1 | Principal relationships between the parties |

| |

Source: National Audit Office and the Department | |

__________________________________________________________________________________________

1 All figures quoted in this report are cash except where otherwise stated.

2 The figure includes the fixed price for the design and construction of the new facilities, fees for construction advisers, capital expenditure in preparation for the provision of facilities management services and debt interest payments during the construction period.