PART ONE

The terms of the original bank finance appear in line with other early PFI deals but subsequent improvements in PFI financing terms mean that, although the Trust has received a share of the refinancing gains, it continues to pay a premium on the financing costs compared to current deals

1.1 The terms of the bank finance in the original deal appear competitive for a bank financed PFI deal at that time (Figure 4).

4 | Comparison of debt financing terms of the Trust's PFI deal with other early PFI deals | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Project | Norfolk & Norwich hospital | Dartford & Gravesham hospital (Darent Valley) | South Bucks hospital | Calderdale hospital | North Durham hospital | ||||||||||||||||||||

Sector | Health | Health | Health | Health | Health | ||||||||||||||||||||

Closing date | Jan 1998 | Aug 1997 | Dec 1997 | Aug 1998 | April 1998 | ||||||||||||||||||||

Facility | £197 million | £108 million | £54 million | £95 million | £82 million | ||||||||||||||||||||

Lead arrangers | ABN Amro, Bank of Scotland, Barclays, HSBC & Societe Generale | Deutsche, Rabobank & United Bank of Kuwait | Dresdner | Halifax & Bank of Scotland | ABN Amro, Deutsche, Rabobank & Royal Bank of Scotland | ||||||||||||||||||||

Period of loan | 20 years | 20 years | 23 years | 27 years | 20 years | ||||||||||||||||||||

Margin1: |

|

|

|

|

| ||||||||||||||||||||

■ Construction | 135 bp | 150 bp | 150 bp | 140 bp | 130 bp | ||||||||||||||||||||

■ Operations | 125 bp | 125 - 135 bp | 140 - 150 bp | 125 bp | 115 bp | ||||||||||||||||||||

Project | Bromley hospital | South Manchester hospital | Fazakerley prison | A19 |

| ||||||||||||||||||||

Sector | Health | Health | Prison | Roads |

| ||||||||||||||||||||

Closing date | Nov 1998 | Aug 1998 | Dec 1995 | Oct 1996 |

| ||||||||||||||||||||

Facility | £157 million | £86 million | £63 million | £63 million |

| ||||||||||||||||||||

Lead arrangers | ABN Amro, BNP Paribas & Dresdner | Bank of Scotland & Royal Bank of Scotland | ABN Amro & Bank of America | Industrial Bank of Japan & CIBC |

| ||||||||||||||||||||

Period of loan | 21 years | 25 years | 18 years | 18 years |

| ||||||||||||||||||||

Margin1: |

|

|

|

|

| ||||||||||||||||||||

■ Construction | 140 bp | 135 bp | 100 bp | 150 bp |

| ||||||||||||||||||||

■ Operations | 125 bp | 115 bp | 150 bp | 140 - 170 bp |

| ||||||||||||||||||||

Source: Project Finance International | |||||||||||||||||||||||||

NOTE 1 The margin represents that part of the interest cost which reflects the risks of the project. 135 bp is 135 basis points. This means the interest cost is | |||||||||||||||||||||||||

1.2 The successful delivery of the new hospital and the maturing PFI market have enabled better financing terms to be obtained on the funding in place prior to the refinancing producing a £34 million gain (Figure 5).

5 | Improvement in financing terms arising from the maturing PFI market and the successful delivery of the new hospital | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Financing term | Original bank financing | Bond financing following the refinancing | Resulting refinancing gain (net present value) | How the refinancing gain arises | ||||||||||||||||||||

Period of borrowing1 | 20 years | 32 years | 29 | Once the hospital was successfully delivered Octagon was able to increase the period of borrowing as funders are prepared to offer longer borrowing periods now the PFI market is more mature. The effect is that the repayment of borrowings is extended into later years so that the borrowings have a lower net present cost taking account of the time value of money. | ||||||||||||||||||||

Interest Margin2 | LIBOR + 135 bp (construction) LIBOR + 125bp (operations) | Gilt +81bp (including a monoline fee of 29bp) – equivalent to LIBOR + 51bp at the time of the refinancing, a reduction of over half of the interest margin compared with the original borrowing | 5 | Most of this improvement in the interest margin reflects the lower risks which funders attribute to PFI projects now the market is more mature. Although the original financing terms allowed for a reduction in the interest margin once the new hospital had been constructed, the successful completion of the construction allowed a further small improvement to the interest margin for the operational period. The lower interest margin reduces the borrowing costs throughout the period of the borrowing. | ||||||||||||||||||||

Total refinancing benefit relating to the funding in place prior to the refinancing |

|

| 34 |

| ||||||||||||||||||||

Source: Royal Bank of Canada |

|

|

| |||||||||||||||||||||

NOTES |

|

|

|

| ||||||||||||||||||||

1 To optimise the refinancing gain (in which the Trust would share) arising from longer borrowing periods available on refinancing the Trust agreed to extend the primary contract period from 30 to 35 years following the delivery of the new hospital. The minimum contract period now extends to 2037. | ||||||||||||||||||||||||

2 The interest margin is the additional interest cost, over and above the base rate for commercial borrowing, as represented by LIBOR (the London Interbank Offered Rate), to reflect the specific risks of the project. | ||||||||||||||||||||||||

3 The improved terms obtained by Octagon on refinancing are consistent with the financing terms in other PFI deals at the time of the refinancing in 2003. | ||||||||||||||||||||||||

1.3 Octagon has been able to generate further refinancing gains of £81 million from the improved market for financing PFI hospitals and lower general interest rates, mainly by increasing its borrowings and accelerating its shareholder distributions.

1 Octagon has taken on additional borrowings (Figure 6).

6 | Increase in Octagon borrowing | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Source of funding | Pre-refinancing | Post-refinancing | Increase on refinancing | NOTES 1 The opportunity for Octagon to increase its borrowings at the time of the refinancing arose from a number of factors connected with: the better financing terms available as a result of the maturing PFI market; the successful delivery of this hospital and the demonstration that the operational phase of the project is going to plan; and the reduction in general interest rates. A key part of the improved financing terms available to Octagon on refinancing related to the cover ratio (the extent to which expected net income must cover the level of debt repayment). When the original deal had been financed in 1998 the funders had been conservative in the level of annual debt repayments they would allow Octagon to take on in relation to Octagon's expected net income. By 2003, when the refinancing took place, funders were content to accept a higher ratio of debt repayment to income (equivalent to a lower cover ratio). This was because, compared to 1998, the funders now perceived a lower risk that unexpected movements in Octagon's income or non-financing costs might adversely affect Octagon's capacity to meet its debt repayment obligations. In addition, because longer period of borrowings were now available on PFI deals (Figure 5) this gave Octagon the opportunity to spread the repayment of its borrowings over a longer period (Figures 7a and 7b). This meant that the annual repayments due on the original level of borrowings would be lower and a higher level of borrowings could be taken on. The combination of lower cover ratios, increased borrowing periods and other factors such as the reduction in commercial borrowing rates and the interest margins specific to PFI deals all enabled Octagon to increase its borrowings at the time of the 2003 refinancing in a manner acceptable to the funders. | |||||||||||||

Senior debt | 200 | 306 | 53 | ||||||||||||||

32 | 32 | - | |||||||||||||||

Equity | 1 | 1 | - | ||||||||||||||

Total | 233 | 339 | 45 | ||||||||||||||

Source: Royal Bank of Canada (from Octagon records) | |||||||||||||||||

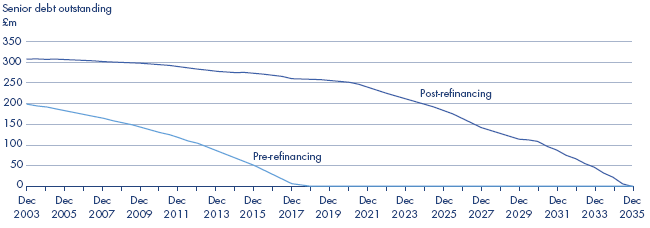

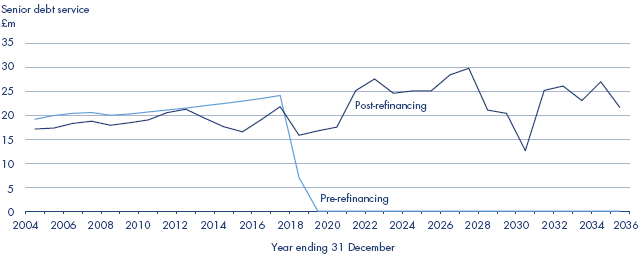

2 The increased senior borrowings will now be repaid over a longer period (Figures 7a and 7b).

7a | Change in Octagon's debt repayment |

Source: Royal Bank of Canada (from Octagon records) | |

NOTE Increasing the borrowings on the improved terms available in 2003, to allow shareholders to realise early benefits, produced a refinancing gain of £76 million. A further £5 million gain arose from extending the minimum contract period during which the borrowings would be repaid. | |

7b | Change in Octagon's debt repayment |

| |

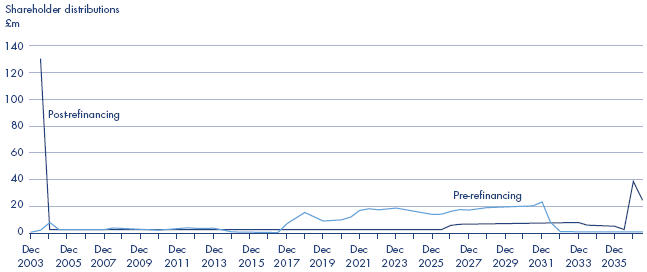

3 As the increased borrowings were not needed to operate the project these additional funds, and the improved financing terms, have enabled Octagon to both increase and accelerate the benefits to its shareholders (Figure 8).

8 | Acceleration of benefits to Octagon shareholders following the refinancing |

Source: Royal Bank of Canada (from Octagon records) | |

4 Octagon has also benefited from falling general interest rates (Figure 9).

9 | Interest rate movements 1998-2003 |

Source: Bloomberg and Royal Bank of Canada (from Octagon records) | |

NOTES Octagon only entered into short-term interest rate hedging in respect of part of its original borrowings. In respect of 75 per cent of its debt Octagon had protection against fluctuating interest rates through a fixed interest arrangement at 6.33 per cent (known as a fixed interest swap), until the end of 2003. In respect of the remaining 25 per cent of its debt Octagon had protection against fluctuating interest rates through linking movements in its interest rates to movements in the Retail Prices Index (RPI) at RPI plus 3.71 per cent (known as a RPI swap) until the end of 2007. In respect of the remaining period of its original borrowings, which would not be subject to these hedging arrangements, Octagon was exposed to the risk of both favourable and unfavourable movements in interest rates. In accepting this risk Octagon made a commercial judgement which it subsequently benefited from as a result of the generally downwards trend in general interest rates which arose after 1998. At the time of the refinancing Octagon was forecasting rates of interest on general commercial borrowing as represented by LIBOR (the London Interbank Offered Rate) of 4.90 per cent compared with its average forecast of 6.62 per cent in 1998. Octagon was able to increase the scale of its refinancing gains in 2003 as a result of this fall in general interest rates which had arisen since 1998. Royal Bank of Canada estimate that, on an indicative basis, around £35 million of the refinancing gain of £81million that mainly arose from Octagon increasing its borrowings and accelerating its shareholder distributions related to the reduction in general interest rates that had occurred since 1998. A further benefit of £5 million which Octagon had earned up to 2003 as a result of falling interest rates was part of its operating results in that period and as such did not constitute a refinancing gain as defined by the Refinancing Code and related guidance. | |

1.4 The Trust is receiving both benefits from the refinancing in accordance with the new code and also new risks but has assessed the overall effect of the refinancing as value for money.

1 The Trust is receiving around 30 per cent of the refinancing gains in accordance with the new voluntary code (Figure 10).

2 To improve the affordability of the project, the Trust agreed to extend the minimum contract period by five years in return for a reduction in its annual payments by £1.8 million over the initial minimum contract period (Figure 11) and an extra £0.1 million a year share of the refinancing benefit.

10 | Gains arising from the refinancing | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

| £m | % | |||||||||||||||||||

Trust share of refinancing gains | 33.9 | 30.9 | |||||||||||||||||||

Octagon share of refinancing gains | 75.8 | 69.1 | |||||||||||||||||||

Total refinancing gains subject to sharing allocation | 109.7 | 100.0 | |||||||||||||||||||

Source: Royal Bank of Canada (from Octagon records) | |||||||||||||||||||||

NOTE The gains were shared by applying the code for sharing refinancing gains on early PFI deals agreed between the Treasury and the private sector in 2002. In addition to the refinancing gains subject to the sharing allocation, as permitted by the code a further £5.8 million of refinancing gains were not subject to sharing to allow Octagon to make good a shortfall in shareholder returns which had arisen prior to the refinancing. | |||||||||||||||||||||

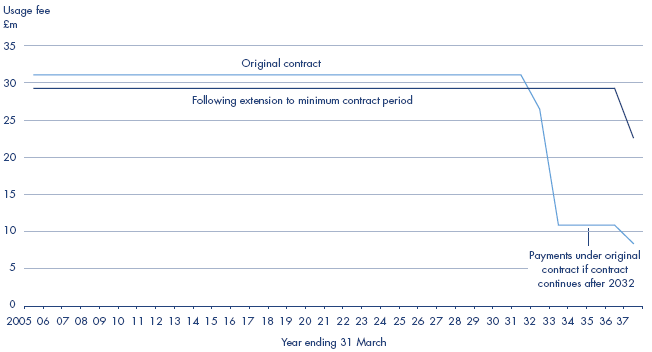

11 | Extended minimum contract period and reduced annual usage fee following the refinancing |

Source: Royal Bank of Canada | |

NOTES 1 Following the refinancing and the agreement to extend the minimum contract period the Trust's annual contract payments reduced, in March 2005 prices, by £3.6 million from £42.7 million to £39.1 million, a reduction of 8 per cent. There was a £1.8 million annual reduction as the Trust will be paying the previous PFI contract price over a longer period and a further £1.8 million annual reduction from the Trust's share of the refinancing gains which is being received by the Trust over time as a reduction to the annual PFI charges. £0.1 million of the Trust's annual share of the refinancing gains arose from its 50 per cent share of the refinancing gains conditional on the minimum contract extension. 2 The payments in Figure 11 relate to the usage fee and are in real terms. As agreed in the original contract the contract price is subject to annual increases for cost inflation as measured by the Retail Prices Index. The usage fee is part of the current total PFI contract price of £37.8 million (Figures 1 and 24). | |

3 The Trust bears the risk that its liabilities in the event of early contract termination would be higher following the refinancing but has demonstrated that, based on conservative assumptions of the current view of the likelihood of the contract being terminated early, the refinancing is value for money (Figure 12).

12 | Analysis of increase in termination liabilities following the refinancing | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

| A | B | C | D | ||||||||||||||||||||

Trust share of refinancing gain2 | 33.9 | 33.9 | 33.9 | 33.9 | ||||||||||||||||||||

Increase in Trust's termination liabilities:3 |

|

|

|

| ||||||||||||||||||||

Expected value of the increased | (7.3) | (10.7) | (3.7) | (5.4) | ||||||||||||||||||||

Assumption4 | That contract may be terminated at any time throughout the contract period (with a 10% probability in each year) | That contract may be terminated when increase in termination liabilities is highest (with a 10% probability) | That contract may be terminated at any time throughout the contract period (with a 5% probability in each year) | That contract may be terminated when increase in termination liabilities is highest (with a 5% probability) | ||||||||||||||||||||

Value for money (i.e. refinancing gain less expected value of the increased termination liabilities)5 | 26.6 | 23.2 | 30.2 | 28.5 | ||||||||||||||||||||

Source: Royal Bank of Canada | ||||||||||||||||||||||||

NOTES 1 Figure 12 summarises the detailed analysis of the value for money of the refinancing which the Trust and its financial advisers Royal Bank of Canada carried out prior to the Trust agreeing to the terms of the refinancing. 2 The Trust share of refinancing gain and the expected value of the increase in termination liabilities are expressed as net present values. 3 The Trust's termination liabilities are linked to the levels of Octagon's outstanding debt which has increased as a result of the additional borrowings taken on to optimise the refinancing gain. 4 The Trust considers that each of the alternative assumptions in its analysis shown in this table is a conservative assumption of the current view of the likelihood of the contract being terminated early. It is possible that over the life of the contract, whose minimum period now extends to 2037, that judgements on the likelihood of early contract termination may change. If a future situation were to arise where the contract does have to be terminated early then the Trust could face significantly higher termination liabilities mainly because of the increased borrowings which Octagon took on at the time of the refinancing. 5 This value for money analysis, which was undertaken prior to the Trust agreeing to the refinancing, compares the refinancing gain with the expected value of the Trust's increased termination liabilities following the refinancing. It is part of a wider analysis of value for money which the Treasury and the | ||||||||||||||||||||||||

4 There are both possible risks and benefits to the Trust's decision to take its share of the refinancing gains over time (Figure 13).

13 | Risks and benefits of the Trust's decision to take its share of the refinancing gains over time | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Time |

| Potential risk: amount of refinancing gain outstanding based on taking refinancing gain over time (NPV)1 | Compensating benefit: indicative reduction in maximum termination liabilities compared with taking refinancing gain as a lump sum3 | ||||||||||||||||||||

At time of refinancing | (2003) | 33.9 | 33.9 | ||||||||||||||||||||

Ten years on | (2013) | 18.7 | 29.8 | ||||||||||||||||||||

Twenty years on | (2023) | 9.2 | 22.6 | ||||||||||||||||||||

End of minimum contract | (2037) | - | - | ||||||||||||||||||||

Source: The Department, the Trust and Royal Bank of Canada | |||||||||||||||||||||||

NOTES 1 On advice from the Department of Health the Trust chose to take its share of the refinancing gains over time by way of a £1.8 million reduction to its annual contract payments. This was consistent with the Department's advice on other refinancings and reflected the Department's view that: A taking the gain over time allows the gain to benefit both current and future users of the Trust's clinical services; B the Department's accounting requirements would create additional charges to the Trust if the gain was taken as a lump sum as this would be treated as an asset which would be amortised as a charge in subsequent years' accounts; C if the refinancing gain was taken as a lump sum then, in order to maintain the level of the refinancing gain, Octagon would have had to increase its borrowings by £33.9 million to fund the lump sum payment to the Trust. Additional borrowings by Octagon would have further increased the Trust's potential termination liabilities; and D the potential credit risk from part of the Trust's share of the refinancing gain being outstanding in the event of early termination of the contract would be addressed as the Trust would hope to continue to receive its share of the refinancing benefit by continuing to pay the reduced annual charge in any arrangement with the project funders or new contractors. 2 Prior to the Trust's decision to take its share of the refinancing gain over time the central Norfolk health system (the Trust, the local Mental Health Trust and four Primary Care Trusts) had expressed a preference to receive the gain as an immediate lump sum to enable it to invest in modernising service delivery to achieve savings required to meet financial balance across the system. 3 The reductions in maximum termination liabilities arising from taking the refinancing gains over time are indicative figures based on the repayment profile of the additional borrowings which Octagon would have had to take on in order to fund the Trust's share of the refinancing gain as a lump sum and to maintain the level of the refinancing gains. The Trust's actual termination liabilities at any future date would, in practice, depend on a number of other factors including prevailing interest rates at the time of the termination. | |||||||||||||||||||||||

1.5 After sharing in refinancing benefits NHS Trusts continue to pay a premium on the financing costs on early PFI hospital deals compared to current deals (Figure 14).

14 | Comparison between early PFI deals and current PFI deals | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||

Aspect of refinancing | Early PFI deals | Current PFI deals | ||||||||||||||||||||

Improvement in financing terms through maturing PFI market | In early PFI deals the public sector should receive 30 per cent of any refinancing gain arising from improved financing terms as a result of the maturing PFI market through applying the voluntary code for sharing refinancing gains | The public sector would expect to get the benefit of the improved financing terms in the initial contract price | ||||||||||||||||||||

Further refinancing, for example by increasing borrowings on completion of the construction phase | In early PFI deals the public sector should receive 30 per cent of any refinancing gain through applying the voluntary code for sharing refinancing gains | In current deals the public sector would receive a contractual 50 per cent share of any refinancing gain after the contract was let1 | ||||||||||||||||||||

As explained in paragraphs 1.2 and 1.3 above better financing terms are available in current PFI deals compared to early PFI deals as a result of the maturing PFI market and the reduction in general interest rates in recent years. As Figure 14 shows, in a current deal the public sector will expect to get these benefits in the initial contract price or, if only available after contract letting, then the public sector will receive 50 per cent of the benefit. On early PFI deals such as that entered into by the Trust, which did not specify sharing refinancing gains, the public sector will at best be limited to receiving 30 per cent of the improvement in financing terms now available through sharing in refinancing gains under the voluntary refinancing code. As a result, after sharing in refinancing benefits, NHS Trusts with early PFI deals continue to pay a premium on the financing costs compared to current deals. | ||||||||||||||||||||||

Source: The National Audit Office | ||||||||||||||||||||||

NOTE 1 Because the public sector will expect to get the benefit of the improved financing terms in the initial contract price in current PFI deals, there is likely to be a significant reduction in the extent of subsequent refinancing gains compared with early PFI deals. The Trust's advisers, Royal Bank of Canada, consider that the scope for the private sector to also generate refinancing gains after a contract is let, by increasing borrowings and accelerating shareholder distributions, will similarly be reduced in situations where the level of debt, in relation to the private sector's expected net income from the project, has been maximised in the original funding arrangements. | ||||||||||||||||||||||