SUMMARY

1 Most government projects by value under the Private Finance Initiative (PFI) are funded by the private sector through a mix of debt finance (in the form of bank loans or bond finance) and risk capital (known as equity capital1) provided by the shareholders of the project company.

2 Previous NAO reports2 have shown that there are opportunities for the investors of the equity capital to secure benefits by refinancing on more favourable terms the debt finance of early PFI projects which have been successfully delivered. The improved financing terms on these projects are available as: lending in the PFI market is considered less risky now that the PFI market is established; the delivery risks of the projects have been dealt with; and, in the debt markets, it is currently possible to borrow for longer periods at fixed rates of interest which are lower than when the early PFI contracts were let.

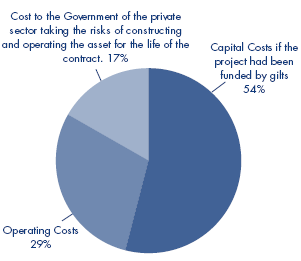

3 Only a small proportion of a PFI project's total costs are subject to refinancing. In most cases a refinancing will not increase the overall financing costs of a project in cash terms but, in improving the terms of the debt finance, will enable payments to the investors of equity capital to be made earlier in the contract period. The resulting benefit to the equity investors can significantly improve the returns on their investments as their initial investment is small (typically around 10 per cent of the project's finance) relative to the debt being refinanced (typically around 90 per cent of the project's finance). In the illustration of costs measured over the whole life of a typical project (Figure 1), 29 per cent are operating costs and a further 54 per cent represent the cost of financing the capital cost of the infrastructure if the Government itself funded the project through issuing gilts. The remaining 17 per cent represents the additional financing cost to government of the private sector taking the risks of constructing and operating the asset for the life of the contract (the financial risk premium).

|

1 |

An illustration of costs in a PFI project measured in nominal whole life values |

|

It is the 17 per cent of costs which are subject to refinancing1

Source: This is based on a financial model developed by the Treasury, typical of a hospital project |

|

|

NOTE 1 In nominal cash flows, refinancing redistributes the costs of finance between debt and equity but does not increase the total costs of the project. |

|

4 Before July 2002, it was not mandatory for PFI projects to have contractual arrangements to share gains arising from debt refinancing. Following reports by the NAO and Committee of Public Accounts (PAC)3, which highlighted the particular opportunities for the private sector to secure gains from debt refinancing on early PFI projects, the Office of Government Commerce (OGC), who had responsibility at the time for PFI policy, consulted with the private sector and introduced arrangements whereby:

■ PFI contracts signed from July 2002 onwards would provide for public authorities to receive 50 per cent of any gains arising from debt refinancing;

■ As from September 2002, a voluntary code ("the Code") would apply whereby authorities would generally expect to receive 30 per cent of the gains from debt refinancing where their contracts had not included arrangements to share the gains.

5 The successful operation of the voluntary sharing arrangements of the Code is important as it is the early PFI deals, entered into before July 2002, which are likely to have the greatest potential for debt refinancing gains but most of these deals had no contractual mechanism for sharing these gains. In later deals, the improved financing terms now available should be priced into the deal when the contract is let and there are contractual arrangements to share any subsequent refinancing gains. In December 2002, the OGC told the PAC that it expected the public sector to receive £175 to £200 million from the introduction of the Code.4 Responsibility for PFI policy was transferred from the OGC to the Treasury on 1 April 2003.

6 The opportunities to refinance the debt finance of PFI projects have arisen as the PFI market has matured. A further development as a consequence of the maturing PFI market and a period of liquidity in the global capital markets has been the emergence of a market, known as the secondary equity market, in the buying and selling of the equity capital in established PFI projects.

7 In this report we examined:

■ how the level of debt refinancing gains which the Government has secured compares with the OGC's expectations in 2002;

■ how well the new arrangements to share debt refinancing gains have been working;

■ whether there are any risks for authorities from debt refinancings; and

■ how the maturing PFI market is affecting the use of equity capital in PFI projects.

8 Our examination included a cross government survey of PFI projects. The study scope and methodology is set out in Appendix 2 and a list of the projects we surveyed is in Appendix 3.

9 In summary we have found that:

■ The Government has secured £137 million from PFI debt refinancing but there has been little recent activity; (Part 1 of this report)

■ Debt refinancings may bring risks as well as benefits; (Part 2)

■ There have been developments in the PFI equity market as the PFI market has matured and financial markets have become more liquid. (Part 3)

In terms of the overall effect on the value for money of PFI deals, the debt refinancings that have been completed relate to only a small proportion of PFI contracts. As we reported during 20055, the increased risks to the public sector from certain refinancings which generated large refinancing gains through increased private sector debt made the value for money of those refinancings questionable despite the sharing of the gains. The Treasury's emphasis on value for money appears to be bringing greater discipline but also a reduction in debt refinancing activity.

10 Our main findings have been:

a) Some large debt refinancings have enabled the Government to secure gains of £137 million

The debt refinancing of PFI projects had enabled the Government to secure the right to gains of £137 million up to February 2006 (Figure 2). £102 million arose from four refinancings. Three hospital deals (Norfolk and Norwich, Bromley and Darent Valley), where the lead investors were Barclays and Innisfree, accounted for £60 million of the Government's gains. The investors, who retained large gains from these refinancings, had shared 30 per cent of the gains with the public sector under the voluntary sharing arrangements of the Code. A further £42 million of the Government's gains arose from the refinancing of the London Underground Tube Lines project where the sharing was based on a contractual provision and did not, therefore, rely on the Code's voluntary sharing arrangements. The remaining debt refinancings of early PFI deals since the Code was introduced have mainly been undertaken on smaller projects. These have yielded small gains for both the public and private sectors with the public sector securing on average less than £1 million from each refinancing.

|

2 |

The right to refinancing gains secured by the public sector up to February 2006 |

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

Number of refinancings |

Actual gains which the public sector has secured the right to |

2002 OGc estimate of gains to the public sector £m |

||||||||||||||||||||||||||

|

Voluntary sharing under the Code: |

|

|

|

||||||||||||||||||||||||||

|

Norfolk and Norwich Hospital |

|

1 |

|

|

34 |

|

|

||||||||||||||||||||||

|

|

3 |

60 |

|

||||||||||||||||||||||||||

|

|

|

|

|

||||||||||||||||||||||||||

|

Other deals |

|

17 |

|

|

12 |

|

|

||||||||||||||||||||||

|

|

20 |

72 |

175-200 |

||||||||||||||||||||||||||

|

Other refinancing gains: |

|

|

|

|

|

|

|

||||||||||||||||||||||

|

London Underground |

|

1 |

|

|

42 |

|

|

||||||||||||||||||||||

|

|

|

27 |

|

|

65 |

|

No estimate |

||||||||||||||||||||||

|

|

|

47 |

|

|

137 |

|

No estimate |

||||||||||||||||||||||

In addition, the financing of the Ministry of Defence's Skynet 5 project has been improved as part of a much wider substantial restructuring of the project.

b) Refinancing gains arising from the Code have declined since 2004

The £137 million of refinancing gains the Government has secured the right to includes £72 million from the voluntary sharing arrangements of the Code, nearly all of which arose prior to 2005. Only three small debt refinancings under the voluntary sharing arrangements have been completed since December 2004 from which the public sector will gain £0.7 million. The decline in gains from this aspect of debt refinancing has been affected by investors taking stock of the additional scrutiny of PFI refinancings following NAO reports in 2005 on two of the large refinancings of the Norfolk and Norwich and Darent Valley hospital projects.

These NAO reports, together with a subsequent PAC hearing on the Norfolk and Norwich deal, raised concerns about large refinancing gains where the private sector had increased its debt to accelerate the benefits to investors. The concerns focussed on the fact that these refinancings had been based on the public sector accepting both increases to the liabilities it would incur to end the contracts early and extensions to the minimum contract periods. The authorities judged that, on the balance of current probabilities, these arrangements would be value for money in the long term. These conclusions could change however if the authorities wish to end the contracts early because of changes in requirements over the next 35 years. The Treasury has re-emphasised to departments the need to rigorously evaluate the value for money of all refinancing proposals. This is expected to take into account any changes to public sector termination liabilities taking account of the amounts that the providers of both debt and equity finance would be able to recover on termination.

The amount being received from debt refinancings, where sharing of gains under the Code would apply, has mainly declined because the private sector is less assured that the public sector will now agree to further refinancings involving significant increased debt. The private sector has less interest in taking forward other smaller value refinancings because the time and costs involved in arranging a refinancing of any size are considerable.

c) Gains from early PFI deals currently look likely to fall short of the OGC estimate

Up to February 2006, the gains of £72 million which the public sector had secured from the voluntary sharing arrangements of the Code were well short of the OGC's 2002 estimate of £175 to £200 million. It is difficult to estimate how much more the Government may now secure from these voluntary sharing provisions particularly as it is currently uncertain whether the recent decline in refinancing gains from early PFI deals will continue. In addition, the majority of the 700 PFI contracts which have been let may not give the prospect for the public sector to benefit from refinancing; many are too small for refinancing to be viable, others do not have project specific finance or there would be costs involved in unwinding the existing financing arrangements which could make refinancing unattractive. If there is some recovery in refinancing activity, our current best estimate is that the total gains to the Government from the Code are likely to increase to between £110 and £150 million, still short of the OGC's 2002 estimate. The OGC's estimate could, however, yet be achieved in due course if there are any further large refinancings. The Treasury accepts that the Government is receiving less from Code refinancings than initially expected but its main focus has been on the achievement of value for money through an appropriate balance of risk and reward rather than maximising the gains. The Treasury has carried out some initial research to identify which of the large PFI deals may be capable of refinancing.

d) The new gain sharing appears to be generally working well with some exceptions

Where early deals have been refinanced since 2002 the provisions of the Code for calculating and sharing the refinancing gains have, for the most part, been followed. Overall, the public sector has secured the right to receive close to 30 per cent of the refinancing gains (Figure 3) which was the expectation when the Code was established. In line with Treasury guidance, deals signed since 2002 are giving the public sector the right to 50 per cent of any refinancing gains.

We found no evidence from the survey returns that the private sector had undertaken refinancings without informing the relevant department. We did, however, find three refinancings since the new sharing arrangements came into force, of roads contracts let by the Highways Agency, where the gains were not shared in accordance with the Code. On two of these projects, the Highways Agency and Balfour Beatty said they had been at an advanced stage of negotiating these refinancings in 2002 before the sharing arrangements of the Code became effective. If the gains on these two refinancings had been shared in accordance with the Code, the public sector would have received £1.7 million. The gains from a third refinancing, completed by the Roadlink consortium in 2004, have not been disclosed to the National Audit Office but the Highways Agency believes Roadlink's gains to have been less than £1 million.

|

3 |

Sharing of gains on refinancings since the Code came into operation |

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Project |

Total refinancing gains (NPV) £m |

Amount shared with public sector (NPV) £m |

% of gain shared with public sector |

||||||||||||||||||||||||||

|

Norfolk & Norwich Hospital |

|

115.5 |

|

|

33.9 |

|

29.31 |

||||||||||||||||||||||

|

Bromley Hospital |

|

45.3 |

|

|

14.2 |

|

31.3 |

||||||||||||||||||||||

|

Darent Valley Hospital |

|

33.4 |

|

|

11.7 |

|

35.0 |

||||||||||||||||||||||

|

|

|

194.2 |

|

|

59.8 |

|

30.8 |

||||||||||||||||||||||

|

14 other projects where gains were shared in accordance with the Code |

|

48.2 |

|

|

11.7 |

|

24.31 |

||||||||||||||||||||||

|

17 refinancings where gains were shared in accordance with the code |

242.4 |

71.5 |

29.5 |

||||||||||||||||||||||||||

|

3 projects where no gains were shared2 |

4.8 |

- |

- |

||||||||||||||||||||||||||

|

20 completed refinancings since the code came into operation |

247.2 |

71.5 |

28.9 |

||||||||||||||||||||||||||

|

Source: National Audit Office Survey and PUK database of PFI projects |

|||||||||||||||||||||||||||||

|

NOTES 1 Norfolk and Norwich and three other projects gave rise to gains to the public sector of less than 30 per cent in accordance with the Code because returns to investors, prior to the refinancing, were less than expected when the contracts had been let. 2 Two refinancings, involving Balfour Beatty and WS Atkins had refinancing gains of £4.8 million. The gains from a third refinancing, completed by the Roadlink consortium in 2004, have not been disclosed to the National Audit Office but the Highways Agency believes Roadlink's gains to have been less than £1 million. |

|||||||||||||||||||||||||||||

e) Refinancings provide scope for significantly increasing the investors' internal rate of return

In many refinancings the cash which the investors will receive over the contract period will decrease as investors exchange later benefits for the right to increased early benefits from the project. The acceleration of benefits can, however, significantly increase the internal rate of return6 to investors in some cases. Most early PFI contracts were let on the expectation of an internal rate of return to investors of 15 to 17 per cent. Where projects disclosed to us the investors' internal rate of return following refinancing these ranged from less than 10 per cent to over 70 per cent. In a fifth of these projects, all early PFI deals, the investors' internal rate of return following refinancing had risen to over 50 per cent and, in the case of Debden Park School and Bromley Hospital, to as high as 71 per cent. As around half of the projects surveyed on this issue did not disclose their investors' internal rate of return there may be other projects where there have been high internal rates of return after refinancing.

f) The opportunity to benefit from refinancing can also create new risks

Sharing in refinancing gains has the potential to benefit the public sector but there are also risks. The risks relate to:

Income from refinancings involves some uncertainty

The public sector's gains from the Code depends on continued adherence to what are voluntary arrangements. The private sector has said that any attempt to amend the code could jeopardise the voluntary arrangements that have been widely complied with since the inception of the Code. In addition, the ability to refinance will depend on conditions in the financing market. Those authorities which have chosen to take their refinancing gains over time could, depending on the reasons for the termination and the contractual terms, also face uncertainty in collecting their gains if they were to effect an early termination of their contracts.7 The future flow of income from the Code cannot, therefore, be predicted with certainty.

There can be additional liabilities following a refinancing

Some refinancing proposals have increased public sector risk as they have required the public sector's agreement to possible increases in termination liabilities or an extension of the contract period. The Treasury expects departments to carefully assess such proposals and only to accept them if the value for money of such proposals is fully demonstrated.

There may be service related risks

Although authorities reported they were generally satisfied with service performance and the incentives to perform following refinancing, it is still too early to judge whether the acceleration of benefits to shareholders following a refinancing will have an impact on service delivery in the longer term. The theoretical risks are that, having taken benefits, the investors might become less concerned about the project's performance or the project may not have retained sufficient funds to meet future asset maintenance obligations and unforeseen expenditure. Investors argue, however, that, as they expect further revenues from the projects, they will be concerned to ensure that contractors continue to perform. The providers of debt finance are also likely to be concerned that the repayment of their debt, which in some cases has increased on refinancing, is not put at risk by poor service performance. The Treasury has also observed that the terms of financing of PFI project companies following a refinancing are normally in line with those of new PFI deals. It therefore expects the risks to service delivery following a refinancing to be no different from those in new deals.

g) There are transactions which Treasury guidance excludes from gain sharing

The Treasury accepted, after market consultation and taking account of practicalities, that it would be unacceptable for the Government to interfere in certain situations which would, therefore, not be subject to gain sharing arrangements. These exclusions, set out in Figure 10, page 18 and para 3.6, include the sale of equity shares (although the profit on such sales will be subject to taxation). Also, the Government's gain sharing does not extend to the way that investors and other funders manage their portfolios of interests in PFI projects unless this impacts on the underlying PFI contracts which departments have entered into. These boundaries were initially set out in Treasury guidance in July 2002 and were then also applied to the operation of the Code. In negotiating the Code with the private sector the Treasury acknowledged that the private sector was making significant concessions to voluntarily share debt refinancing gains on early PFI deals where there had been no contractual requirement to do so.

h) There is now an emerging secondary equity market in PFI shares

The development of a secondary market for PFI equity has been helpful to investors who fund PFI deals and may also bring benefits to the public sector. Whereas previously there was uncertainty as to whether investors would be able to exit from their PFI investments there is now a reasonably assured market for investors to sell shares in successful PFI projects should they wish to do so. 40 per cent of projects told us there had been a change in the investors in their projects. In these situations either the initial or subsequent investors may wish to also refinance the project and we found that half of these projects had been refinanced, a higher incidence of refinancing than in projects where there had not been a change in investors. The sale of equity can also help future PFI projects where the proceeds are reinvested in other PFI deals. As the supply of PFI equity increases this should drive down the cost of equity and improve the pricing of PFI deals. The Treasury has said that it considers there is scope to reduce the returns of 13 to 15 per cent which investors currently expect when PFI projects are bid for. Further information on the secondary market is set out in Appendix 4.

i) Funders may derive benefits from establishing portfolios of interests in PFI projects

As the number of PFI contracts has increased there has been a trend towards investors and debt providers building a portfolio of interests in PFI projects. This may enable investors to achieve operating efficiencies across the portfolio or to improve financing terms either for the existing portfolio or for subsequent transactions. It is possible in theory that investors or debt providers may seek to improve the financing of the portfolio rather than refinancing individual projects, but there is little evidence to date of this type of activity.

j) There is limited information at present on the operation of the PFI equity market

All authorities receive information about a PFI project company's financial structure and the expected returns to investors when the company bids for the contract or if it refinances the project. In addition, Treasury guidance since 1999 has provided that authorities should have the right to further information available to the lenders. Nevertheless, many authorities had difficulties providing financial information about their PFI projects to assist this examination. Partnerships UK (PUK) records refinancings which have been notified to it and also launched in 2005 a database of PFI projects which includes financing information. However, considerable further work is needed to make aspects of this data accurate and comprehensive and this will require the support of the authorities. The profits or losses which investors may derive from selling shares in PFI project companies are not disclosed to authorities because the contract is between two private sector parties.

__________________________________________________________________________________________

1 Equity capital is usually a mix of ordinary shares and subordinated debt (debt that ranks behind the main debt on repayment).

2 Previous NAO and PAC reports dealing with PFI refinancing are set out in Appendix 1.

3 Appendix 1.

4 Report from the Committee of Public Accounts: PFI refinancing update (HC 203, June 2003).

5 NAO reports on Darent Valley Hospital: the PFI Contract in Action (HC 209 2004-05) and The Refinancing of the Norfolk and Norwich PFI Hospital: how the deal can be viewed in the light of the refinancing (HC 78 2005-06).

6 See paragraphs 1.36 and 1.40 for further explanation of this measure of investor returns. The improved debt financing terms which contributed to increases in investors' internal rates of return should be available to the public sector in current procurements reducing the likelihood of later refinancing gains.

7 See paragraphs 2.4 to 2.5 and Appendix 9 for further explanation of the risks associated with taking the gain as a lump sum or over time.