Since the voluntary code was introduced the value of refinancings has been less than expected due to a number of factors

1.8 Excluding rescue refinancings13 where the public sector would not expect to receive gains 13 Code refinancings had yielded £70.8 million up until the end of 2004.14 By comparison, there were only three Code refinancings in 2005, of which only one, Laganside Courts yielded a share (£0.7 million) to the Government. There are a number of factors which may account for this subdued nature of refinancing activity despite there being projects which could be suitable for refinancing.

|

6 |

PFI Projects (aggregate Capital Value at contract signature) |

|

|

|

|

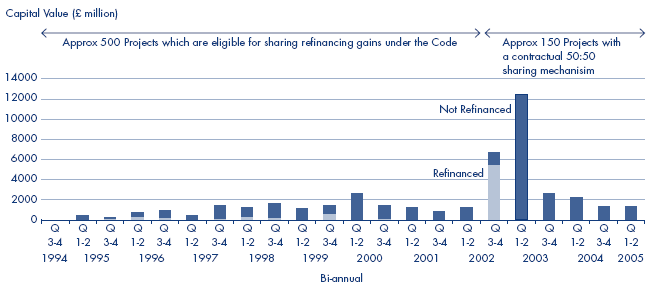

NOTES 1 The peaks during 2002-03 relate to three London Underground Projects with a combined value of £16.2 billion of which one, with a value of £5.5 billion, has been refinanced. The other two are bond financed and European Investment Bank financed and this limits their ability to refinance. 2 In addition to the above there were 11 PFI deals reaching financial close previous to 1994 of which one (Second Seven Crossing) has undergone a refinancing. 3 There is usually a time lag (usually 2 to 3 years) from contract signature to when a project can be refinanced based on the time it takes for a PFI project to become operational. |

|

The sharing of gains and public sector involvement has caused the private sector to consider whether to go ahead with certain refinancings

1.9 The NAO's PFI refinancing update report (November 2002) identified that only 26 per cent of contracts let before June 2000 had an arrangement to share refinancing gains, and only half of these required the authority's approval for a refinancing. Hence prior to the introduction of the Code there was, in most cases, no obligation on the private sector to share refinancing gains or to consult with the public sector over the refinancing.

1.10 The introduction of the Code has meant that the private sector now has to consider:

■ whether the refinancing is worthwhile after sharing 30 per cent of their total refinancing gain with the public sector; and

■ whether it wishes to undertake the time and expense of complex negotiations with the public sector before the refinancing can be effected.

Putting the Code into practice has brought greater appropriate scrutiny of the value for money of refinancing proposals

1.11 The fact that there were only two Code refinancings in 2005 which yielded gains of £0.7 million to the public sector was mainly attributable to the market taking stock of the scrutiny of two large refinancings of early PFI deals under the Code. The NAO's reports on Darent Valley Hospital and Norfolk and Norwich Hospital highlighted large refinancing gains by the project companies increasing their debt at the more favourable terms then available and thereby accelerating the distribution of benefits from the project to the shareholders. The internal rate of return to investors following the refinancings of these early PFI deals able to take advantage of the improvement in funding terms were 56 per cent at Darent Valley and 60 per cent at Norfolk and Norwich.15 The public authorities agreed to higher termination liabilities and extended minimum contract periods as part of the increased debt arrangements. The authorities judged that, on the balance of current probabilities, these arrangements would be value for money in the long term. These conclusions could change however if the authorities wish to end the contracts early because of changes in requirements over the next 35 years.

1.12 There was considerable interest shown by the media in these NAO refinancing reports, particularly focussing on the high returns to private sector investors. Some senior public sector officials expressed to us reservations that a refinancing in the current climate would lead to a critical press even if the refinancing is proven to be value for money. This is especially the case with regards to the earlier PFI projects where the market had been immature and therefore the refinancing gains could be large.

1.13 In February 2005, following the NAO report on Darent Valley Hospital, the Treasury issued an Application Note to help authorities and their contractors to apply existing Treasury guidance more rigorously and consistently to refinancing proposals. The note emphasises the need for a proven value for money case for refinancing proposals, particularly where the public sector teams are asked to accept increased termination liabilities in conjunction with the refinancing. This focus of attention is designed to prevent refinancings occurring which generate large returns to the private sector while at the same time increasing the risk to the public sector without due regard to value for money. The private sector's need to consider the impact of this Application Note, and the existence of other investment opportunities in an active market during 2005, contributed to the decline in PFI refinancing activity.

The Treasury has set out its position on the value for money aspects of refinancing but there has been some uncertainty in the market

1.14 Although the Treasury's Application Note emphasised the need for a proven value for money case for refinancing proposals, interviews we conducted with banks, advisors, monoline insurers and secondary market funds (SMFs) identified that, nevertheless, the market became uncertain in 2005 about what future refinancings would be acceptable. Their uncertainty arose in part because the Application Note was not prescriptive in the methodology to be applied in carrying out the value for money evaluation. Some funders and advisors generally assumed that increases in termination liabilities were no longer going to be accepted by departments. The Application Note had said that: "Given the complex issues which Refinancings raise, it would not be surprising for an Authority to conclude that the simplest Refinancing proposal - particularly one that does not involve any change to Contract termination liabilities - was also the best". The Treasury has clarified in discussions with the market on specific deals that consideration of whether there has been any change to termination liabilities should take into account the total amounts that the providers of both debt and equity finance would be able to recover on termination. Since refinancings that did not involve an increase in public sector termination liabilities were relatively unattractive to the private sector, this contributed to the reduced activity.

1.15 The Treasury has taken opportunities to articulate that there could still be cases where departments would be justified in accepting some increase to their termination liabilities but only where the consequences of agreeing to these increased liabilities has been fully assessed as value for money. The Treasury, together with the Department of Health, is planning to establish good practice in dealing with these issues on a current refinancing being taken forward on the Swindon PFI hospital project.

The public sector relies upon the private sector to instigate a refinancing

1.16 Evidence from our survey showed that public sector project teams were:

■ aware of the potential for refinancings within their projects but,

■ had no knowledge of the reasons why the private sector were not pursuing a refinancing and,

■ were not proactive in finding out the reasons why the private sector were not pursuing a refinancing.

1.17 Although there are benefits to both sides in sharing in a refinancing gain which offers value for money for the public sector, the initiative for setting a refinancing in motion lies with the private sector since it is their debt which is to be refinanced. There is a risk that public sector driven refinancings could be motivated by affordability rather than value for money reasons. Also, the Treasury considers that there are risks to a public authority in pressing for a refinancing since the private sector might try to take a negotiating advantage from the authority's eagerness for a refinancing. For example, pressure might be brought to bear on the authority to agree to increased termination liabilities and contract extensions. Or, the authority might be asked to share in the initial costs of the refinancing proposal or find its bargaining power weaker in resolving any separate contract disputes.

1.18 However, there could be benefits from the public sector project teams being more aware of the refinancing intentions of their private sector counterparts since they could for example prepare in advance for dealing with the technical financial issues which arise from a refinancing. Creating a receptive atmosphere may also facilitate the refinancing process where the gain is deemed to be marginal by the private sector.

__________________________________________________________________________________________

13 A refinancing where the contractor has been in financial difficulties.

14 Details of all Code refinancings are in Appendix 9.

15 On a similar refinancing, of the Bromley Hospital project, the internal rate of return to investors increased to 71 per cent following the refinancing.