The Department reviewed options into the placement of Section 2 construction risk

3.13 Under the 1998 restructuring, the Department expected that construction risk associated with Section 2 would transfer to Railtrack Group when it exercised its option to purchase the section. While the Department was keen not to carry the Section 2 construction risk, it was not, in late 2000, prepared to accept Railtrack Group's revised proposals for exercising the option. Compared against the original terms of the option, the Department estimated that the revised proposals would increase the 1997 present value of public sector support through the access charge loan facility by between £370 million and £430 million (1997 prices) depending on forecasts of Eurostar UK's passenger revenues (Figure 15).

3.14 The Department, wanting to consider its options, progressed discussions with both LCR and Railtrack Group. LCR explored the feasibility of the insurance market taking risk at high thresholds of cost overrun. The Department also analysed the option in which the 1998 arrangements remained in place, but with the Department supporting LCR by carrying the risk of construction overruns through an earlier and increased call on the access charge loan.

3.15 The Department, finding LCR's initial proposals unattractive because it would effectively bear construction risk, agreed with LCR that it could involve Bechtel, a key member of Rail Link Engineering, in working up proposals under which Bechtel would carry some construction risk. The Department also asked Railtrack Group to work up a proposal to manage the construction of Section 2, including carrying some construction risk, but without the obligation of purchasing the section.

3.16 As a result of these requests, by late February 2001, the Department had two sets of viable proposals to compare with the arrangements already in place under the 1998 restructuring, albeit without Railtrack Group exercising its Section 2 option, (Figure 16). The Department appraised each option, calculating, in net present value terms, the total costs that the taxpayer would bear and the benefits that it would forego in relation to the construction of Section 2.

|

15 |

The Department estimated that Railtrack Group's revised terms for exercising the Section 2 option would increase the 1997 present value of public sector support through the access charge loan facility by between £370 million and £430 million |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Proposal |

Forecast of Eurostar UK's passenger revenues |

Access charge loan (£ million, 1997 present value in 1997 prices) |

|||||||||||||||

|

Railtrack Group exercising its option to |

2001 Mid Case |

340 |

|||||||||||||||

|

Railtrack Group exercising its option to |

2001 Mid Case |

710 |

|||||||||||||||

|

Source: The Department |

|||||||||||||||||

|

NOTES 1 Railtrack Group wanted the enhanced terms to cover: lower than expected revenues associated with lower than expected Eurostar UK passenger revenues; expected lower revenues from future use of the Link by domestic services; an underestimated allowance for inflation; additional costs associated with Thameslink 2000; and an increase in risk allowance. 2 Railtrack Group would own the full length of the Link under both proposals. 3 Railtrack Group would carry Section 2 construction risk under both proposals. |

|||||||||||||||||

|

16 |

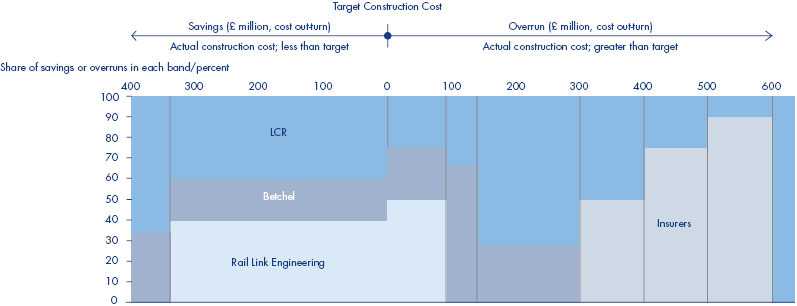

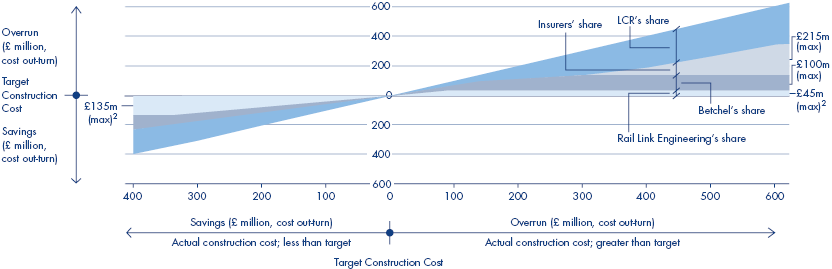

Compared against the Target Construction Cost set in 2001, the LCR/Bethel proposal transferred more construction risk to the private sector than the other 1 proposals reviewed by the Department |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

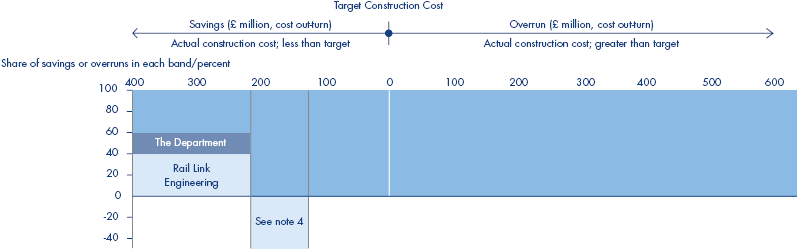

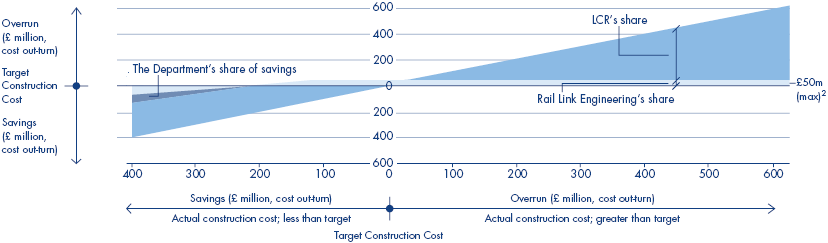

The LCR/Betchel Proposal Bands showing the distribution for sharing savings or overruns as a result of the actual construction cost being respectivly less than or greater than the Target Construction Cost set in 2001. |

|||||||||||||||

|

The distribution of savings/overruns

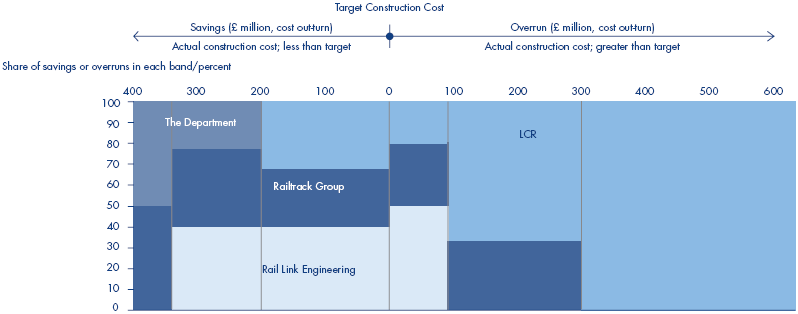

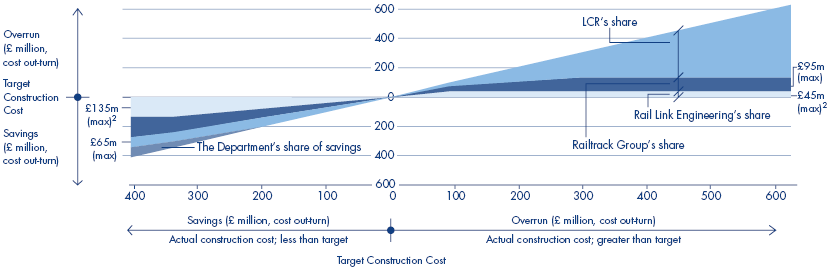

Railtrack Group’s Proposal Bands showing the distribution for sharing savings or overruns as a result of the actual construction cost being respectivly less than or greater than the Target Construction Cost set in 2001.

The distribution of savings/overruns

Arrangements under the 1998 restructuring but without Railtrack Group’s participation Bands showing the distribution for sharing savings or overruns as a result of the actual construction cost being respectivly less than or greater than the Target Construction Cost set in 2001.

The distribution of savings/overruns

|

|||||||||||||||

|

Source: The Department |

|||||||||||||||

|

NOTES 1 In the above arrangements, inflation is assumed to be below the contractual caps. 2 The limit of Rail Link Engineering's share of savings/overruns is based on the value of its fixed fee at the actual completion date, inflated using the Average Earnings Index. The maximum shown in the LCR/Bechtel proposal and Railtrack Group's proposal are based on inflating the 2001 fee at the rate of 3.7 per cent per annum. The maximums shown under the 1998 arrangements were calculated using the 1998 fee, actual average earnings inflation to 2001 and 3.7 per cent per annum thereafter. 3 Arrangements for Section 2 under the 1998 restructuring did not have contractual force. It is questionable whether Rail Link Engineering would have agreed to contracts that retained the sharing mechanism for the target construction cost set in 1998 in the light of further planning and development work on the project between 1998 and 2001. 4 The Section 2 target construction cost in the 1998 restructuring was £2,215 million (1997 prices). As part of the 2001 negotiations, the Section 2 target construction cost was increased to £2,714 million (2001 prices), a real increase of about £180 million (1997 prices) after allowing for project-related inflation. Therefore under the 1998 arrangements, Rail Link Engineering's sharing of overruns would crystalise at an actual out-turn cost lower than the out-turn cost related to the target construction cost set in 2001. |

|||||||||||||||

3.17 Assuming the same outcome from all three options, the calculations showed that the most financially advantageous option for the taxpayer was the proposal under which the Department took all the construction risk (Figure 17). The Department calculated that the 1997 present value of Railtrack Group's proposal was £190 million (1997 prices) more expensive. The 1997 present value of the LCR/Bechtel proposal was around £40 million (1997 prices) more expensive, depending on concessions granted to Railtrack Group if the LCR/Bechtel proposal was accepted.

3.18 The Department chose to proceed with the LCR/Bechtel proposal on the basis that it contained performance incentives (the sharing of savings and the risk of sharing cost overruns) that did not exist in the option in which the Department carried construction risk. In addition, the Department expected that, as a consequence of the incentive arrangements, the risk of overruns would be significantly less than in the case where the Department took the risk. In comparing the LCR/Bechtel proposal against Railtrack Group's proposal, the Department favoured the former because, should cost overruns exceed £300 million (cash out-turn), £215 million of the next £300 million of overruns would be covered by insurers, subject to the insurers' limited exposure to the risk of inflation, which is contractually determined and capped.