Debt raised through the bond issues in 2003 was also competitively priced

14 In November 2003, a little over a month after the opening of Section 1, LCR raised nearly £1,550 million of debt secured against payments of track access charges from Eurostar UK and the Government's payment of the Domestic Capacity Charge. The debt comprised bank debt, an issue of fixed interest bonds and an issue of index linked bonds.

15 LCR marketed the two bond issues more actively than it had the 2002 issue of GGBs because investors were not familiar with the structure and credit basis of the proposed issues. Similarly to the 2002 issue of GGBs, LCR took provisional orders from investors. Demand for the index linked bond was so strong that the margin (over the benchmark gilt) was so competitive that LCR increased the size of the issue. LCR placed the index linked bonds and the fixed rate interest bonds in the market with margins of 0.21 per cent and 0.24 per cent above their respective gilt benchmarks. RBC Capital Markets considered these margins competitive compared to the concurrent margins demanded by the market in secondary trading of similar issues such as bonds issued by the European Investment Bank.

16 LCR's preparations in advance of securing the bond and bank debt in 2003 was more complex than the market management run prior to the launch of the 2002 issue of GGBs. To take advantage of the low cost of debt in June 2003, LCR entered into a number of financial transactions known as swaps23, which the company used to hedge against adverse movements in interest rates in the period through to the conclusion of the debt arrangements. The value of LCR's swaps was £1,666 million, which it spread over a portfolio of swaps with seven different maturities ranging from 10 years to 40 years.

17 Shortly before LCR went to market to raise the debt it unwound the swaps by taking an opposite position, in other words agreeing to pay a floating rate and to receive a fixed rate. As it happened, during the period of the hedge, interest rates increased and, consequently, LCR saved approximately £60 million. However, had interest rates fallen LCR would not have benefited from the lower cost of funds. The aim of a hedge is to lock in an element of the cost of financing to gain a greater degree of certainty over affordability rather than speculate on interest rate movements.

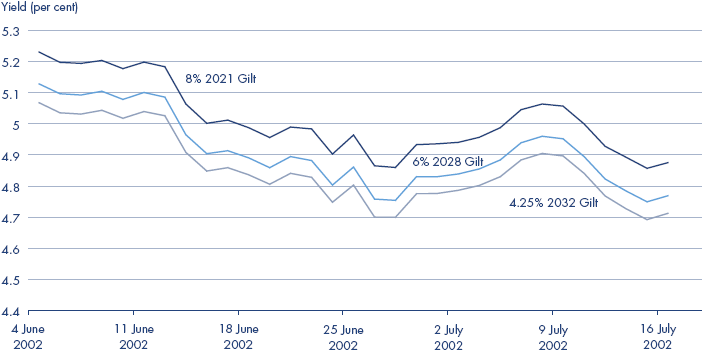

24 | When the GGBs were sold on 25 June 2002, the yield of the benchmark gilt (4.25 2032Gilt) stayed within the bounds of its current trend and did not trade out of line with other long dated gilts |

Source: RBC Capital Markets | |

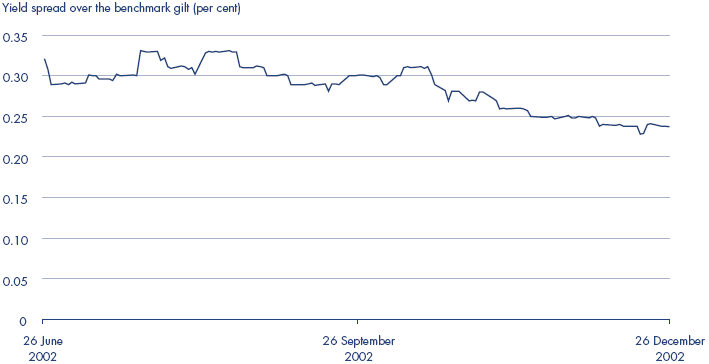

25 | For nearly four months after their issue, the 2002 GGBs traded close to the margin set in the book building exercise |

| |

Source: RBC Capital Markets | |

18 As LCR unwound its swaps, it commenced a market management exercise similar to that it had executed in advance of the sale of the GGBs. RBC Capital Markets reported that the yields of the benchmark gilts remained within the reasonable bounds of their trends, indicating that LCR's market management was successful. The interest rates that LCR pays for the debt is 5.234 per cent under the fixed rate bonds and 2.334 per cent plus RPI24 for the index linked bonds.

19 The Government guaranteed LCR's obligations under the hedging arrangements, as LCR did not have the resources to set aside sufficient cash to meet potential payments under the swaps. Although LCR was first in line for any risk associated with interest rate movements, ultimately the Government and the taxpayer would have had to bear the impact of the adverse consequences to LCR's cashflows. LCR was responsible for the hedging exercise but the Department monitored the transactions to protect its position.

20 The Department's financial advisers, Citigroup, monitored transactions for the longer dated swaps to ensure that the prices offered were good value. However, it wanted to compete for some of the shorter dated swaps business and so stepped down from its monitoring role to avoid conflicts of interest. The Department accepted Citigroup's reduced monitoring role because the shorter-dated swaps market is competitive and, therefore, the role for independent monitoring was less important. RBC Capital Markets found that effective processes were in place for ensuring that the pricing for the swaps transactions was in line with the market.

_________________________________________________________________________________

23 A swap is a financial instrument that can be used to change the basis on which interest is paid on an asset or liability, for instance a floating rate is turned into a fixed rate or vice versa.

24 RPI is the UK All Items Retail Price Index published by the Office for National Statistics as a measure of UK inflation.