Benefits to shareholders may be improved by extending the term of the funding

2.3 A key element of the funding for many PFI projects is senior debt, so called because the lenders of senior debt have the highest ranking claim over the assets of the project company compared to all other funders and investors. The arrangements for repaying senior debt in many respects resemble a domestic repayment mortgage, whereby the project company makes regular instalments of principal and interest. A shorter term of loan will therefore require larger instalments to repay it in full than will a longer term loan of equal amount.

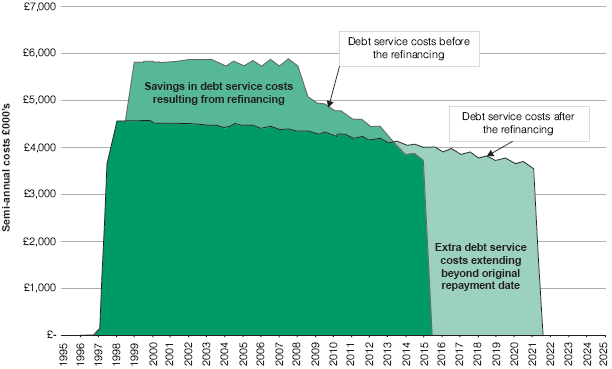

2.4 In the case of Fazakerley prison, one aspect of the refinancing involved extending the term of the senior debt from 20 to 26 years. This in turn reduces the level of instalments payable by the project company in the first 20 years leaving more free cash with which to pay dividends to shareholders, albeit at the expense of less free cash in years 21 to 26 (Figure 6). The additional value that this creates for shareholders, in present value terms, is £5.2 million.

Figure 6 |

|

| How increasing the maturity of the senior debt facility for the Fazakerley project created £5.2 million of additional value for shareholders |

|

|

The graph above compares the half-yearly instalments of principal and interest payable by FPSL under the original loan, with those payable after the refinancing. Due to the extension in the term of the loan, the proportion of principal payable in each period is reduced, creating savings for the company over the next 13 years. Thereafter, the company will face additional costs because the loan will not have been repaid in full by this time. However, because of the time value of money, the savings in the early years outweigh the costs in the final years, providing a net benefit to shareholders of £5.2 million. Source: National Audit Office from information supplied by PricewaterhouseCoopers, FPSL's advisers | |