Shareholders may benefit from the early repayment of subordinated debt or equity capital

2.8 A common condition of banks lending to a PFI project is that the companies within the consortium provide a proportion of the total funding required on a basis subordinated to the banks. Shareholders, and on occasions external investors, usually provide such funding in the form of subordinated debt and equity. Its purpose is to provide the project company with adequate capital to absorb any adverse financial consequences arising from construction risks or poor performance in delivering the service specified. At the same time, this reduces the risks shouldered by the banks providing the senior debt.

2.9 Once the construction or implementation phase of a project is finished and the service is being delivered satisfactorily, banks may agree to relax their requirements for subordinated debt or equity because the project risks have reduced significantly.

The source of additional | Figure 7 |

|

|

| |

|

| |

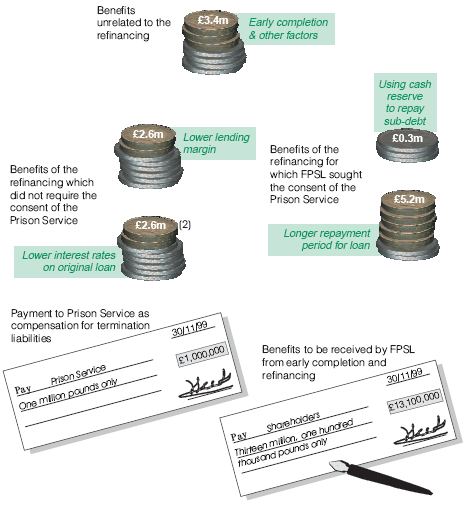

| Notes: | 1. Benefits are quoted as net present values as at 30th November 1999, based on a real discount rate of 6%. |

|

| 2. It is unclear from the legal contract as to whether FPSL needed to seek Prison Service consent to extend the interest rate hedging arrangements to cover the remaining term of the existing loan facility and, therefore, whether the £2.6 million of refinancing benefits from lower interest rates on the original loan also depended on the Prison Service's agreement. FPSL's analysis of the benefits reflects its lenders' opinion that such consent was not required. |

Source: National Audit Office | This figure shows the different factors which contributed to the increase of £13.1 million in expected shareholder returns on the Fazakerley prison PFI contract. The shareholders made a payment of £1 million to the Prison Service to compensate the Service for the increase in termination liabilities arising from certain aspects of the refinancing. |

2.10 There are benefits to the investors or shareholders from having subordinated debt or other investment repaid early on in the life of the contract, because they can generally find a more profitable use for these funds either by using them in other parts of their businesses or by making other investments. Repayment of these investments does not normally affect the ownership of the project company. The companies within the consortium will continue to be shareholders in the project company by virtue of nominal holdings of the project company's ordinary shares, and they will therefore continue to be entitled to receive dividends paid from profits on the project.

2.11 In the case of the Fazakerley prison, the shareholders put up some £7 million of subordinated debt for the project, the proceeds of which were placed on deposit and acted as a contingency reserve during the construction of the prison. Now that construction has been completed and the prison is operating satisfactorily, the banks agreed as part of the refinancing that a much lower level of reserve would be required and that most of the cash released could be used to repay the shareholders' original investment of subordinated debt. The total value created for the shareholders as a result is £0.3 million in present value terms.13

___________________________________________________________________________

13 The value created for shareholders from the repayment of the subordinated debt has been calculated using a public sector real discount rate of 6%. Shareholders would have evaluated aspects of the refinancing using their own discount rate which is higher than that of government and which would have made a more compelling case for the repayment of the subordinated debt.