12.1 Government approval and PAA award

One of the major project milestone and approval requirements for alliance projects, as articulated in the Policy,20 is for the Owner to seek endorsement from the relevant Minister and approval from the Treasurer to execute the Project Alliance Agreement with the Preferred Proponent. The Owner, as part of its submission to government seeking that approval, is required to produce a report which demonstrates that the tender outcome is aligned with the requirements and objectives set out in the approved Business Case and the Owner's VfM Statement (which should also be aligned with the approved Business Case) at a fair cost, and that the process undertaken to come to this conclusion is consistent with the alliancing policy intent and guidelines. This Guidance Note proposes that this report be in the form of a Business Case Alignment Report (BCAR). The BCAR also reports on the negotiated Commercial Framework and the proposed PAA for execution.

As the key document supporting the decision to enter into an alliance contract, the BCAR should be impartial of the procuring processes and should be developed by the Owner. The report should reconcile the Project scope, service level and Project TOC with the corresponding items in the Business Case. Areas of significant variance must be explained in terms of changes relating to performance, innovation, risk profile or other.

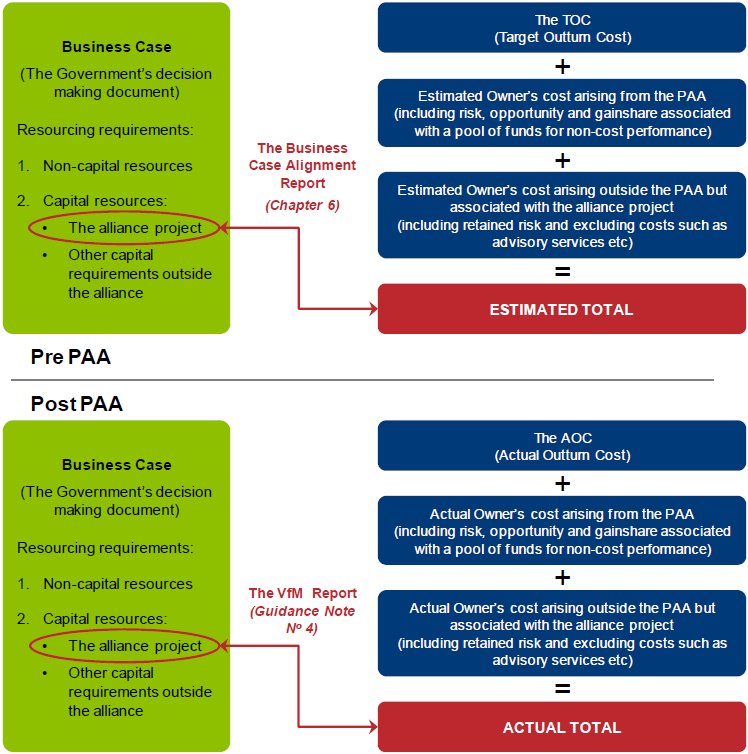

The Business Case budget cost estimate for an alliance delivery method usually comprises:

• the TOC-Target Outturn Cost for the alliance;

• the Owner's estimated costs arising from the legal and commercial arrangements of the alliance (e.g. PAA); and

• the Owner's costs arising outside the alliance's responsibility and the PAA but are associated and are critical for the delivery of the alliance project

It is therefore necessary in the BCAR to include and reconcile all the estimated costs pre- PAA and outside the PAA but are associated with the alliance project that are required to deliver the objectives in the Business Case and not just those that the alliance itself will be responsible. It is also important for the Owner to be aware of any cost shifting between the TOC and those costs outside the TOC and understand the impact of these in terms of risk sharing.

The BCAR is prepared before the PAA is executed, whilst the VfM Report (see Guidance Note No 4) is prepared post-PAA, once the project is final, as illustrated below.

Figure 24: Relationship of Business Case to estimated and actual alliance costs

Appendix C is a template of the recommended components for the BCAR.

_______________________________________________________________________________

20 The implementation of this requirement may vary from jurisdiction to jurisdiction.