Motor Fuel Taxes

In 2007, combined federal motor fuel tax receipts contributed roughly $35.6 billion to the HTF. These taxes are charged at a flat rate per gallon that Congress sets. The current tax rates on motor fuels are 18.4¢ per gallon for gasoline/gasohol and 24.4¢ per gallon for diesel fuel. (The current federal tax for other "special" motor fuels such as liquefied natural gas varies by fuel type, but averages about the same as the gasoline tax.) One cent per gallon in motor fuel taxes (including on gasoline, diesel fuels, and special fuels) yields about $1.8 billion per year.21 Federal motor fuel tax revenues are allocated as follows:

• Proceeds attributable to 2.86$ of the tax (equivalent to about $5 billion annually in 2007 and 2008) are credited to the Mass Transit Account of the HTF.

• Proceeds attributable to 0.10¢ of the tax are credited to the Leaking Underground Storage Tank Trust Fund (not part of the HTF).

• About 4.2 percent of gross motor fuel tax receipts is transferred to the Sport Fish Restoration and Boating Trust Fund or refunded to state and local governments, agricultural users, and other specified exemption categories.

• The remaining proceeds are credited to the Highway Account of the HTF (15.44$/gallon for gasoline and gasohol and 21.44c/gallon for diesel fuel).

Growth in motor fuel tax receipts is driven by two factors: tax rates and fuel consumption. Federal motor fuel tax rates were last raised in 1993, when Congress added an across-the- board 4.3$ increase. The proceeds from this increase, however, initially were directed to the General Fund and were not credited to the HTF until October 1997 (start of federal FY 1998). Because the tax rate has remained constant since 1993, inflation has significantly eroded the value of the tax receipts.

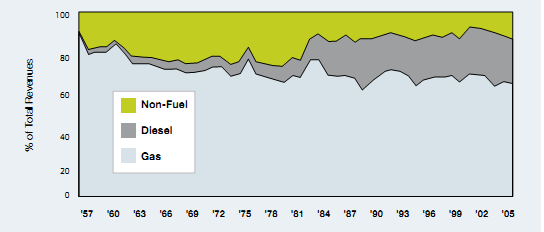

EXHIBIT 2-8: HTF RECEIPTS OVER TIME BY GENERAL CATEGORY, 1957-2006 |

|

Source: FHWA Highway Statistics, Tables HF-10 and HF-210

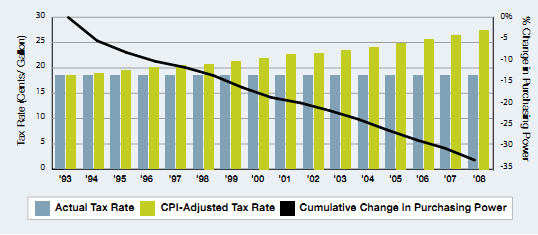

EXHIBIT 2-9: FEDERAL GASOLINE TAX RATE AND LOSS IN PURCHASING POWER |

|

Source: FHWA 2006 Highway Statistics, Table FE-21B, indexed using CPI-U as reported by the Bureau of Labor Statistics.

In order to help maintain the purchasing power of the fuel tax receipts, the tax rates would need to be indexed to a measure of inflation. Exhibit 2-9 illustrates that if the federal gas tax rate of 18.4¢ per gallon had been indexed using the Consumer Price Index for all Urban Consumers (CPI-U) beginning in 1993, the tax rate in 2008 would be 27.5¢ per gallon. By not adjusting the tax rate for general inflation, gas tax receipts have experienced a cumulative loss in purchasing power of about 33 percent over the last 15 years.

A common misconception is that increases in vehicle fuel efficiency also have led to declines in motor fuel tax purchasing power in the last 15 years. In reality, vehicle fuel efficiency increased rapidly from the mid-1970s to the mid-1980s, then declined moderately from 1987 to 2004, and only started to increase again in 2005. In fact, the average fuel efficiency of new 2008 light-duty vehicles (20.8 miles per gallon (MPG)) is still 1.2 MPG lower than the peak reached in 1987 (22.0 MPG).22 (Light-duty vehicles category includes automobiles, sport utility vehicles, vans, and pick- up trucks.)