Other Taxes

Other, non-fuel-related federal taxes contributed $5.3 Billion to the HTF in 2007. About $3.8 Billion of this was raised through a 12 percent federal sales tax on the retailer's sales price for tractors over 33,000 pounds gross vehicle weight (GVW) and trailers over 26,000 GVW. Another $1 Billion was raised through the federal Heavy Vehicle Use Tax, which requires trucks with a GVW of 55,000 pounds or more to pay an annual tax of $100, plus $22 for each 1,000 pounds over 55,000 pounds. The remaining $500 million was raised through a federal excise tax on tires, which charges 9.45$ for each 10 pounds of maximum rated load over 3,500 pounds.23

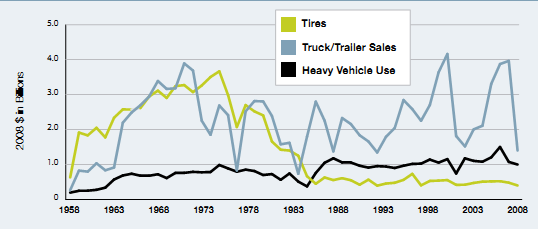

The trends in non-fuel tax receipts since the inception of the HTF are shown in Exhibit 2-10. Unlike the motor fuel tax revenues, which have tended to grow fairly consistently over time, revenues from the truck-related sales taxes are more sensitive to economic cycles and exhibit much greater volatility. Truck tire tax revenues significantly declined between 1975 and 1985, illustrating the sudden impact of technological advancement (in this case, the widespread introduction of radial tires, which greatly increased tire life) as well as a 1984 change in the tax law that repealed tire taxes on vehicles under 33,000 GVW. From 1998 to 2007, growth in non-fuel-related revenues exceeded growth in the motor fuel tax revenues. As noted previously, however, the non-fuel tax revenues appear to have fallen precipitously, Py about 46 percent, from 2007 to 2008, including a drop of nearly $2.4 Billion in receipts from the truck and trailer sales tax.24 This dramatic effect of recent economic conditions demonstrates the potential year-to-year volatility of this group of taxes.

EXHIBIT 2-10: NON-FUEL HTF REVENUES OVER TIME (CONSTANT DOLLARS) |

|

Sources: Historical data from FHWA Highway Statistics, Tables HF-10 and HF-210. 2007 Data from March 2008 Treasury Bulletin.