HTF Account Balances and Funding Implications

Between 1980 and 1995, HTF cash balances gradually grew from $11 billion to $19 billion.27 Between 1996 and 2000, however, receipts substantially exceeded outlays, and the overall balance rose from $19 billion in 1995 to a peak of about $31 billion in 2000. With the economic downturn in 2001, however, revenues fell sharply. By 2005 revenues recovered to previous levels, although their growth rates slowed. And as noted earlier, the HTF revenues for 2008 appear to have fallen by about $3 billion compared with 2007. At the same time, both the Transportation Equity Act for the 21st Century and SAFETEA-LU substantially boosted federal highway and transit spending, causing the HTF cash balances to begin to decline sharply. The HTF overall cash balance (including both the Highway Account and the Mass Transit Account) was down to just over $15 billion at the end of 2007 and would have been below $9 billion at the end of 2008 without | |||

the $8 billion emergency infusion from the General Fund. (Without those funds, the Highway Account balance would have dipped perilously close to zero by late 2008 or early 2009 .)28 |

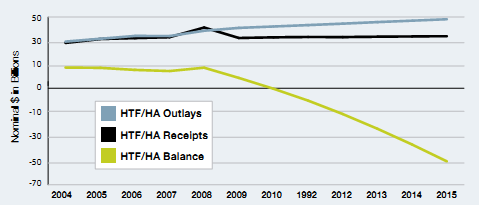

Source: Forecasts made by AASHTO using its federal HTF funding model and based on assumptions contained in the Midsession Review of the FY 2009 Budget | ||

Even with the emergency General Fund infusion in September 2008, the Highway Account cash balance is estimated to fall to between $2 billion and $3 billion by the end of 2009. As shown in Exhibit 2-12, with the growing spread between current-law expenditures and receipts, federal highway program funding cannot be maintained at current levels beyond 2009, and the possibility cannot be dismissed that the Highway Account will run short of liquidating cash before the end of FY 2009.29

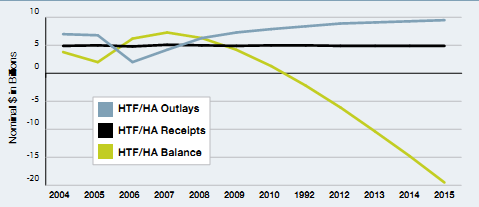

The current trends in federal transit expenditures and receipts practically mirror those on the highway side. The Mass Transit Account balance is estimated to fall to between $4 billion and $5 billion by the end of 2009 and to just $2 billion by the end of 2010. Exhibit 2-13 shows that current-law federal transit program funding cannot be maintained beyond 2010.30

This HTF "solvency crisis" is the result of SAFETEA-LU funding authorizations (through FY 2009) leading to annual outlays that increasingly exceed the capacity of the HTF to meet | |||

Source: Forecasts made by AASHTO using its federal HTF funding model and based on assumptions contained in the Midsession Review of the FY 2009 Budget. | them through new revenues and existing balances. Since the HTF cannot incur negative balances (negative values in graphs are shown only for illustrative purposes), Congress must decide either to provide additional funding to cover the looming short- falls in coming years or to re- duce federal highway and transit spending dramatically to levels that can be supported by cur- rent-law receipts. As illustrated | ||

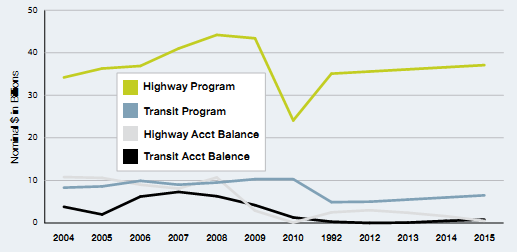

in Exhibit 2-14, without an influx of additional revenues to the HTF the necessary reductions in federal spending will be severe: the highway program would have to be cut by about 45-50 percent from FY 2009 to FY 2010, with only a partial recovery in subsequent years; the transit program would have to be cut by about 50-55 percent from FY 2010 to FY 2011, again with only a partial recovery thereafter. These major reductions would be required because of the multi-year expense reimbursements typically associated with federal-aid capital projects. In any given year, most of the outlays (expenditures) result from prior-year funding commitments. This means that to suddenly reduce outlays to a level supportable by incoming HTF receipts, the current-year funding commitments must be cut drastically to accommodate the liquidation of prior-year commitments. Once the current-year funding commitments have been so reduced, the funding commitments in subsequent years can approximate future receipts to stay within the HTF revenue curve. Essentially, future federal funding has to be reduced significantly from recent authorizations in order to be supported by current-law HTF revenues that are barely growing.31 | |||

Moreover, there may well be mega-trends at work, collectively undermining the assumptions on which these HTF projections are based. It is quite possible that conventional thinking about fleet turnover, the use of alternative fuel vehicles, and other factors will no longer be valid and that the

EXHIBIT 2-14: POTENTIAL FEDERAL FUNDING LEVELS UNDER CURRENT LAW |

|

Source: Forecasts made by AASHTO using its federal HTF funding model and based on assumptions contained in the Midsession Review of the FY 2009 Budget.

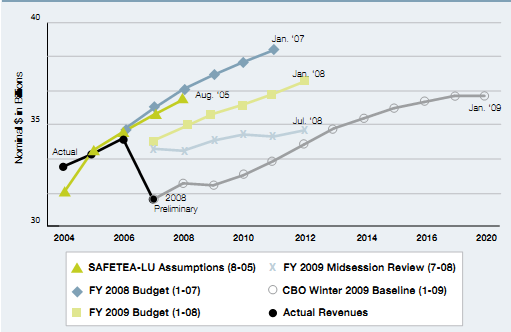

EXHIBIT 2-15: HTF / HIGHWAY ACCOUNT REVENUE PROJECTIONS SINCE SAFETEA-LU |

|

trends in these assumptions will move in the wrong direction (from the perspective of revenues) more quickly, thereby reducing current law revenues much more quickly.