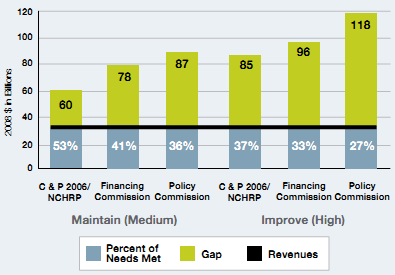

Alternative Investment Strategy

The Baseline Scenario essentially mirrors the federal government's current role of "Continued Significant Federal Investment." (See Box 2-3.) The Commission, however, also considered how investment requirements might change if certain funding principles and investment strategies were aggressively applied to transform the federal program. In particular, the Commission wished to explore the potential investment effect of a federal investment strategy modeled after the "Targeted Investment Role Enhanced with Additional Policies Focused on Driving Innovation and Efficiency." Specifically, the Commission evaluated what federal needs might look like if aggressive use of road pricing were coupled with greater use of technology and other management tools that should result in more efficient investment in and use of the transportation system. | EXHIBIT 2-27: FEDERAL SHORT-TERM NEEDS AND REVENUES | |||||||

Year-by-Year Federal Revenues and Needs Estimates: 2010-15 (billions of nominal $) | ||||||||

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | Total | |

Baseline Revenue Forecast | $38 | $38 | $39 | $40 | $40 | $40 | $235 | |

Need to Maintain |

|

|

|

|

|

|

| |

Base Case Scenario | $81 | $82 | $84 | $86 | $87 | $89 | $509 | |

Funding Gap | $(43) | $(44) | $(45) | $(46) | $(47) | $(49) | $(274) | |

Need to Improve |

|

|

|

|

|

|

| |

Base Case Scenario | $100 | $102 | $104 | $106 | $108 | $111 | $632 | |

Funding Gap | $(62) | $(64) | $(65) | $(67) | $(68) | $(71) | $(397) | |

Note: Sums may vary due to rounding | ||||||||

| ||||||||

To illustrate the long-term potential of such a transformative approach, the Commission developed an Alternative Investment Strategy that assumes comprehensive road pricing is immediately applied to all congested facilities. Other considerations and/or assumptions that went into this alternative analysis included the following:

BOX 2-3: FUTURE FEDERAL ROLE AND IMPACT ON INVESTMENT NEEDS | |

Examining the federal role in surface transportation was not explicitly within the Commission's scope, but any discussion of federal transportation funding and financing policies must be undertaken in the context of potential federal investment responsibilities. Thus, in conjunction with evaluating needs and the associated investment gaps, the Commission considered the range of options for the shape and focus of federal highway and transit investment going forward; four illustrative options are described below. (The Commission does not explicitly endorse any of these options, but it found that they provided a meaningful framework for considering the range of potential federal funding requirements in this chapter. Congress, in its upcoming deliberations, will decide which federal role should serve as the foundation for the next federal transportation program authorization period and beyond.) | |

• Devolution (Minimal Role)—This alternative is premised on the fact that, despite federal funding and oversight, the vast majority of roads and all transit systems are developed, constructed, and managed at the state and local level. Thus, under this alternative, the federal role would be extremely limited, perhaps to supporting and enforcing standards and research and development (R&D). It suggests that federal fuel (and other) taxes should be greatly reduced, leaving states and localities primarily responsible for most of the funding and financing of the surface transportation system. • Continued Significant Federal Investment (Cur- rent Role)—This alternative is premised on the idea that the federal government would remain the central figure in funding the comprehensive needs of the transportation system and thus should directly fund and set policy for the national transportation net- work. Effectively supporting this role would require raising significantly more federal revenues—perhaps through a wide array of means, including both direct and indirect user charges. Regardless of the level of federal funding, however, this alternative assumes that current federal policies and programs would be reformed, not merely extended, to ensure effective use of national resources. • Targeted Investment (Smaller and More Focused Role than Current)—This alternative assumes the federal government would retain responsibility for national standards, R&D, and funding to ensure system performance but on a smaller share of the overall system, | focused principally on the core network (critical roads, nodes, corridors, and public transportation networks, and homeland security). This alternative would require additional federal resources but would be less significant than fully supporting the currently articulated federal role. This alternative also recognizes the need for some cross-subsidization and reallocation of resources at the federal level to achieve certain national network benefits, but it stresses the importance of ensuring that funding sources—particularly for highway funding—have as close a relation to system use as feasible. • Targeted Investment Role Enhanced with Additional Policies Focused on Driving Innovation and Efficiency—This alternative assumes the federal government would support national standards and R&D and would promote system performance on a core network (critical roads, nodes, corridors, and public transportation networks, and homeland security). This alternative also would require additional federal resources but would be less significant than fully supporting the currently articulated federal role. In addition to reallocating some resources at the federal level to achieve certain national network benefits, it also emphasizes the need to make investments that increase innovation and efficiency, particularly at the state and local level. This alternative responds to institutional barriers and political hurdles to innovation, including charging system users more directly, by providing incentives for more aggressive development and implementation of management approaches, operating technologies, and pricing mechanisms.

|

• The same basic tools, methodologies, and assumptions that are used to evaluate similar road pricing scenarios for the C&P report were applied, with adjustments to accommodate a longer time horizon.

• Highway investment priorities that emphasize operations strategies to improve system performance were assumed.

• As with the Base Case Investment Scenario, the highway "cost to improve" estimates incorporate a 1.2 benefit-cost ratio as a threshold for determining improvement needs.

• Transit investment needs were expanded to accommodate both organic ridership growth as well as anticipated travel diversion caused by road pricing. Although it is not possible to determine with precision the degree to which road pricing will increase transit ridership, both the "need to maintain" and "need to improve" cost estimates were increased from the spending required to accommodate the historical 2.4 percent average growth rate in annual ridership to levels compatible with annual average ridership growth of 3.53 percent, which would accommodate a doubling of transit ridership within 20 years.47

• The federal share of highway investment potentially could change. For the purposes of this analysis, the Commission considered the impact of a change from 45 percent of total capital spending needs to 80 percent of needed investment on the National Highway System (excluding federal spending on routes outside that system). This scenario variation would concentrate federal-level spending on the highest-priority roadways, with the federal-eligible system decreasing from 985,128 miles (the current federal-aid highway system) to 163,467 miles (the current National Highway System).48 As with the Base Case Investment Scenario, the federal share of transit investment would remain at an amount equal to 45 percent of total capital spending needs, the recent historical average.

The Commission cautions that this Alternative Investment Strategy is not realistic (at least in the near term) and probably represents a theoretical lower limit on needed system investment. The results, however, may be instructive in the context of what could be achieved in the long run if comprehensive road pricing (e.g., through a vehicle miles traveled charging system) ultimately were embraced by policy makers and the public. The scenario is based on the assumption that all congested highways would be priced immediately; in reality, such wide-scale road pricing likely could not be implemented for many years—nor is it clear how comprehensive such an effort should or would be. Also, to achieve the estimated reductions in needed investments under the Alternative Investment Strategy, the average congestion charge imposed on individual vehicles would need to be more than 30¢ per mile (in 2008 dollars) and be levied on about 20 percent of all vehicle miles traveled.49 It is assumed that congestion charges would be imposed by state and local governments and thus would not provide a source of federal funding. They could, however, provide significant means to supplement or replace existing state and local funding sources in congested areas.

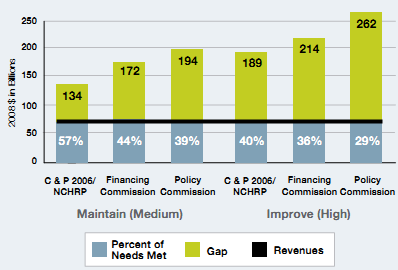

The results of this hypothetical analysis indicate that such an approach could lead to significantly reduced long-term investment needs (all figures in 2008 dollars):

• The total annual level of spending needed to maintain system performance drops by 26 percent, from $172 billion (Base Case Scenario) to $128 billion (Alternative Scenario); highway investment needs fall by more than 42 percent, from $131 billion to $76 billion, while transit investment needs rise by 24 percent, from $42 billion to $51 billion.

• The total annual level of spending needed to improve system performance drops by about 15 percent, from $214 billion to $183 billion; highway investment needs decline by nearly 28 percent, from $165 billion to $119 billion, while transit investment needs increase by nearly 28 percent, from $49 billion to $63 billion.

• Assuming the federal share of total investment remains at the historical 45 percent for both highways and transit, the annual federal funding needed to maintain the combined system falls from $78 billion to $57 billion and the annual federal funding needed to improve the combined system falls from $96 billion to $82 billion. If the federal highway funding role were narrowed, however, to cover 80 percent of the investment needs of the National Highway System (instead of 45 percent of | |||||

| all highway capital investment needs), then the annual federal funding levels required to maintain and improve the combined system would fall further to $40 billion and $65 billion, respectively. The long-term system performance that could be achieved by 2035 under the Alternative In- vestment Strategy would obviously vary based on a wide range of considerations (e.g., the speed of congestion pricing implementation), Put it is estimated to include the following:50 • Need to Maintain—For the overall sys- tem, adjusted average user costs would remain even in constant dollar terms, average delay would decrease by 1.8 percent, pavement conditions would improve by 12.9 percent, and the backlog of needed bridge investment would re- main unchanged. • Need to Improve—The adjusted aver- age user costs would be reduced by 2.2 percent, average delay would decrease by 9 percent, pavement conditions would improve by 9.8 percent, and the backlog of needed bridge investment would be fully addressed. | ||||