I. OVERVIEW OF FEDERAL MOTOR FUEL TAXES

Federally imposed motor fuel taxes are primarily cents-per-gallon excise taxes imposed on the consumption of gasoline, diesel, and special fuels. The origin of federal fuel taxes as a transportation funding source can be traced Pack to the passage of the Federal-Aid Highway Act and the Highway Revenue Act in 1956. (A 2¢-per-gallon federal MFT existed prior to 1956, Put it was not linked to funding for highways or transit.) The two acts established the Federal Highway Trust Fund (HTF), increased the federal motor fuel tax to 3¢ per gallon, created new highway user fees such as truck sale and tire taxes, and dedicated the revenues to the HTF. Federal motor fuel tax rates have been increased sporadically over the years, with the last increase occurring in 1993. (See Exhibit 4-1.)

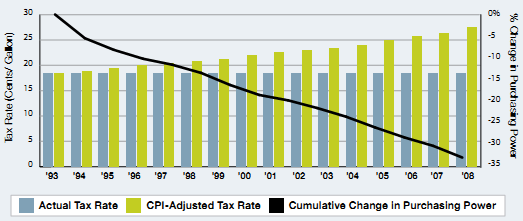

EXHIBIT 4-1: FEDERAL MOTOR | Despite the occasional increases in motor fuel tax rates, the fixed cents-per-gallon structure of the tax means that the purchasing power of MFT revenues begins to decline immediately after any increase. As illustrated in Exhibit 4-2, the actual purchasing power of the gasoline tax has declined 33 percent since 1993. Exhibit 4-3 lists the current total federal fuel tax rates, including amounts not credited to the HTF. These taxes are generally not collected directly from the end consumer; they are paid at major distribution points (known as "the Rack") and then become part of the overall price passed down through the supply pipeline to the consumer.

| ||||

Date | Gasoline Tax Rate | Diesel Tax Rate | |||

| Nominal | 2008 | Nominal | 2008 | |

1956 | 3.0 | 23.7 | 3.0 | 23.7 | |

1959 | 4.0 | 29.6 | 4.0 | 29.6 | |

1983 | 9.0 | 19.4 | 9.0 | 19.4 | |

1984 | 9.0 | 18.6 | 15.0 | 31.1 | |

1987 | 9.1 | 17.2 | 15.1 | 28.6 | |

1990 | 14.1 | 23.2 | 20.1 | 33.1 | |

1993 | 18.4 | 27.4 | 24.4 | 36.3 | |

1996* | 18.3 | 25.1 | 24.3 | 33.3 | |

Current | 18.4 | 18.4 | 24.4 | 24.4 | |

* The 0.1¢-per-gallon MFT for the Leaking Underground Storage Tank Trust Fund was temporarily suspended in 1996.

EXHIBIT 4-2: FEDERAL GASOLINE TAX RATE AND LOSS IN PURCHASING POWER |

|

In total, the contribution of federal motor fuel taxes to the HTF averaged $35.7 billion in 2007 and 2008- $25.4 billion from taxes on gasoline and other fuels and $10.3 billion from diesel taxes.1 At the same time that nominal motor fuel tax rates have increased over the years, the range of investments supported by the HTF has expanded, and revenues at times have been diverted to non-transportation purposes. Beginning in 1983, a Transit Account was established within the HTF, with 2.86¢ per gallon of gasoline and diesel fuel taxes allocated to fund it. In 1987, the Leaking Underground Storage Tank Trust Fund was established with 0.1¢ per gallon of each motor fuel tax (except for liquefied petroleum gas and liquefied natural gas), equaling $226 million in 2007.2 In addition, a portion of MFTs have occasionally been allocated to the General Fund of the U.S. Treasury. Specifically, the Omnibus Budget Reconciliation Acts of 19903 and 1993 each allocated some or all of the tax increases to the General Fund as follows:4 |

| ||||||||||||||||||

• 1990 to 1993: 2.5$ per gallon (all fuels)

• 1993 to 1995: 6.8$ per gallon (all fuels)

• 1995 to 1997: 4.3$ per gallon (all fuels)

• 1997 to 2003: 2.5/3.1 $ per gallon for gasohol only (rate varied by ethanol content)