II. CURRENT MOTOR FUEL TAX OUTLOOK

There is no clear consensus on future federal motor fuel tax revenue levels if current rates are maintained. Due to the cents-per-gallon structure of current federal MFTs, revenue levels are a direct function of fuel consumption. This consumption is driven by two factors - the amount of travel and vehicle fuel efficiency (miles per gallon, MPG).

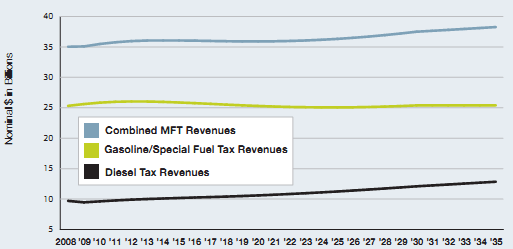

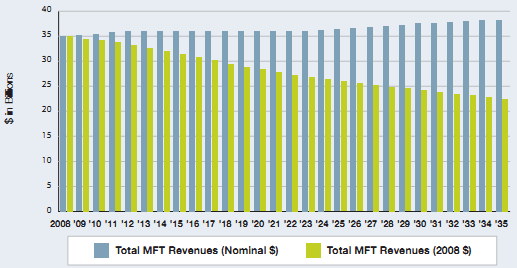

The Federal Highway Administration (FHWA) estimates that vehicle miles traveled (VMT) will maintain an average annual growth rate of 1.5-2.0 percent over the long term as economic expansion and population growth continue to generate demand for highway travel.5 At the same time, however, the most recent U.S. Energy Information Agency estimates predict that the aver- age fuel efficiency for all light-duty vehicles on the road will grow from 20.4 MPG today to 28.9 MPG by 2030, an increase of 42 percent, while that for freight trucks will grow from 6.0 MPG to 6.9 MPG, an increase of 15 percent.6 The combined effect of these anticipated trends is that at current tax rates, total nominal tax revenues will continue to grow, although at a slower rate than inflation. (Thus the purchasing power of the generated revenues will actually decline and will decline even further as a share of VMT.) The growth that does occur will largely be due to steady nominal growth in diesel tax proceeds. (See Exhibit 4-4.) Nominal gasoline tax revenues will only experience moderate growth over the next 25 years and are actually expected to dip for a period until the growth in travel (due in large part simply to population growth) offsets the effect of fuel efficiency improvements on total gas consumption. As illustrated in Exhibit 4-5, the growth in total federal motor fuel tax revenues will be insufficient to keep up with inflation. Thus while annual nominal fuel tax revenues are expected to climb to $38.3 billion by 2035, the value of these revenues in 2008 dollars will only be $22.4 billion.

EXHIBIT 4-4: FEDERAL MOTOR FUELS TAX REVENUE FORECAST |

|

An alternative view, documented in the 2006 Transportation Research Board (TRB) report entitled The Fuel Tax Report and Alternatives for Transportation Funding, is that motor fuel tax revenues will remain reasonably staple and viable over the next 10-15 years Put will then begin to decline significantly as vehicle fuel efficiency improves and the availability and use of alternative fuel vehicles expand.7 (See Box 4-1.) The TRB Fuel Tax study was issued prior to the recent volatility in oil prices and economic turmoil and was based on the assumption that demand for travel is highly inelastic and will thus continue to grow at the long-term rates forecast by FHWA. Recent transportation data, however, indicate that Americans are driving less. Total VMT for October 2008 declined 3.5 percent from a year earlier, and travel for the first 10 months of 2008 was 3.5 percent below the comparable period in 2007, a nearly unprecedented decline. People also are switching to alternative fuel vehicles faster than expected. For the first 10 months of 2008, sales of light trucks declined much more dramatically than overall light-duty vehicle sales, and sales of hybrid vehicles decreased the least. (See Exhibit 4-6.) As a result of these trends, federal MFT receipts are expected to remain flat or even decline slightly over the over the next 5-10 years.8

| It also is important to note that the official medium- to long-term estimates of fuel consumption and associated tax revenues may be overly optimistic about MFT sustainability. Specifically, these estimates use vehicle fuel efficiency and travel growth assumptions that reflect conventional thinking about regulatory requirements, fleet turnover, and other related factors that influence fuel consumption. New possibilities and |

BOX 4-1: KEY FINDINGS FROM THE TRANSPORTATION RESEARCH BOARD'S 2006 SPECIAL REPORT ON THE MOTOR FUEL TAX | |

The most recent comprehensive national assessment of motor fuel taxes was performed by the Transportation Research Board through the Committee for the Study of the Long-Term Viability of Fuel Taxes for Transportation Finance. The goals of the study were to assess the implications of recent trends for traditional highway and transit finance, identify financial alternatives, and suggest ways to overcome barriers to acceptance of new approaches. Major conclusions and recommendations of the study related to motor fuel taxes included the following (note: these findings and recommendations are those of the study's authors and not necessarily endorsed by the Commission): | |

• Current Funding Capacity-The current highway finance system should be able to support some growth in capacity and service improvements but not at a rate that will reduce congestion. • Long-term Tax Revenue Erosion-A 20 percent reduction in average vehicle fuel consumption per mile is highly possible by 2025, but this is dependent on increased regulatory efficiency standards (at or beyond 30 MPG for light-duty vehicles by 2020) as well as higher fuel prices. • Factors Limiting Fuel Efficiency Gains-Progress in vehicle efficiency and associated reductions in motor fuel consumption will be limited by the tendency of consumers to maintain or increase vehicle size and performance, the long lead time needed to bring more fuel-efficient vehicles into large-scale production, and very slow turnover of the vehicle stock. • Erosion of Established Highway Finance Practices- The historical strength of the federal highway program is being threatened by the use of highway user fees for non-highway purposes and the impacts of inflation. • Lessening of Public Support-Due to program changes that redirect funds to less compelling purposes | (e.g., maintenance and reconstruction) and broader social trends, including the "tax revolt," the public and legislatures are more reluctant to support fuel tax rates and fees necessary to sustain the surface transportation system. • Poor Promotion of Efficient Investment-The current finance system fails to ensure that individual projects are economically justified, which has led to poor prioritization and investment practices and has in turn eroded public support for motor fuel tax increases. • Need to Maintain and Reinforce the Existing User Fee Finance System-During the interim period, while alternatives such as more direct road pricing are developed and implemented, the federal government should increase current indirect user fee rates, eliminate motor fuel tax exemptions, and develop mechanisms to capture taxes on alternatively fueled vehicles. • Recognition that Travelers Would Benefit from a Transition to Pricing-The first step in moving to a pricing system where fees are based more on travel than on the level of consumption of gasoline is to adjust current user fee rates to better align payments with costs and to begin a definitive move toward comprehensive road pricing. |

emerging market conditions, such as major advances in fuel efficiency, development and wide-scale roll-out of alternative fuel vehicles, and future oil price shocks, corn- Pined with growing concern about the environment and rapidly developing policy initiatives to reduce petroleum dependence and greenhouse gas emissions, could lead to unprecedented changes in the national vehicle fleet and associated fuel consumption. Much of this will depend on technological uncertainties that are hard to model and predict. If, for example, robust car batteries are developed that allow passenger vehicles to travel relatively long distances on one charge, it is certainly conceivable that there could be a radical change in the vehicle fleet away from gasoline- and diesel-powered vehicles to electric-powered ones.