General Principles Guiding the Use of Debt

Recently much has been written and said expressing caution about state and local governments' overall level of indebtedness-and in some instances, specifically their transportation-related debt. Some analysts have suggested that states and localities have borrowed more debt than is prudent, inferring that debt in general is a bad thing. Conversely, policy makers struggling to encourage greater infrastructure investment in some instances have promoted "alternative financing approaches"-i.e., greater indebtedness-absent adequate consideration of the underlying revenue streams. Debt, however, as a general rule, is neither a good thing nor a bad thing. Rather, debt is a tool that can be a part of the answer when used appropriately.

Following are four general principles that should guide the appropriate use of debt financing for a particular investment or set of investments. The principles should be considered together, not individually, and balanced with other policy factors:

• Maximize Upfront Funding for Long-lived Capital Assets and Match Asset's Useful Life with Debt Term-As the "golden rule" of public finance, debt financing is appropriate for funding capital assets with long useful lives. Conversely, pay-as-you-go funding (i.e., paying out of currently generated revenues or funds on hand) generally is most applicable to fund operations or assets with short useful lives. For assets with longer useful lives, debt financing of comparable duration to the useful life of the asset ensures that the burden of the capital costs is spread over an asset's life and is matched to available revenue streams-such as user fees, targeted dedicated taxes, or other ongoing revenues generated from direct users or other beneficiaries. In the context of comprehensive and ongoing capital programs such as those administered by state departments of transportation, applying the "golden rule" gets a bit more complicated. The subsequent principles in part address this added complexity.

• Mitigate Major Capital Investment Spikes-Debt can be used to smooth the impact of a particularly large one-time spike or general "lumpiness" of a capital investment program and help limit the extent to which other important projects or program elements are crowded out by the major project or set of projects.

• Accelerate Benefits and/or Reduce Costs-Debt can accelerate investment in a major capital project. In many instances, financing costs are less than the construction cost inflation that would accompany deferred investment, thus reducing the overall project cost. Less quantifiable, but more important, are the economic and societal benefits that can be captured by using debt financing. Providing an asset earlier can provide environmental benefits (for instance, where the asset is a cleaner-fueled transit vehicle),

|

BOX 7-2. FINANCING CAPACITY OF ALTERNATIVE FINANCE APPROACHES |

||

|

There are multiple structures available to fund transportation infrastructure investment. Beyond pay-as-you-go funding, these include various forms of debt finance and of private-sector financial participation. This Box provides simplified illustrations of the potential financing capacity with each approach. |

||

|

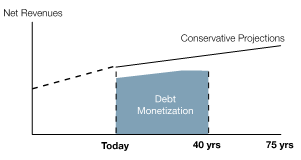

Tax-exempt Debt Financing. Under tax-exempt debt financing approaches, future expected cash flows are leveraged, or borrowed against, in order to deliver upfront cash. States and localities routinely borrow a portion of the present value of a stream of cash flows (such as tax receipts or facility revenues). The amount of debt financing available is a function of several variables, including the length of a debt instrument, the amount of revenues supporting it, the expected growth rate of these revenues, and the stability or riskiness of the revenue steam by expressed as a discount rate and "coverage ratio," which is the multiple required over forecast revenues to satisfy debt investors. Traditional public finance debt markets tend to take a conservative view on expectations for the growth of these net revenues, often allowing only minimal growth to be factored into the debt finance structure. An illustrative debt-financed project might have a profile that looks like this: |

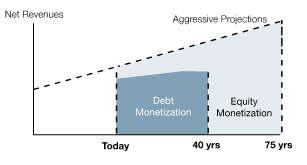

Private-sector Financial Participation. Like tax-exempt debt financing, private-sector financial participation-in the form of debt or equity or a combination of the two- is another tool that can be used to leverage future revenues. Again, project sponsors (e.g., state and local governments) can leverage a future stream of cash flows in order to generate upfront proceeds. Depending on a number of assumptions, a strategy that includes equity investment can raise greater upfront proceeds than can debt financing alone. This is due to a number of key differences between private-sector financial participation and more traditional public finance strategies, including the following: • First, equity investors are sometimes willing to look out over a longer time horizon than debt investors. Private- sector equity participants will invest in 50 years (as much as 99 years) of expected revenues for a given asset. By contrast, debt investors will typically provide only 30 or 40 years of financing at a time. • Second, equity investors are generally willing to "under- write" higher growth rates than will debt investors. While the debt markets will assume minimal (and sometimes zero) growth of net revenues, equity participants are willing to contemplate much higher growth rates in their forecasts of return and take the associated risks. •Third, equity providers in these structures have so far been willing to accept more aggressive assumptions, including lower required "coverage ratios," than their debt investor counterparts-again, balancing risk with return. An illustrative project financed with both debt and private equity might have a profile that looks like this: |

|

|

|

||

|

|

|

|

societal or safety benefits (for instance, improving an accident-prone highway or providing pedestrian or bike paths in a community), or economic benefits (such as roadway or transit investments that spur economic development in the surrounding area).

• Match Costs to Benefits Over Time (Generational Equity)-The above principles notwithstanding, committing future revenues and shifting the burden to future generations through debt financing requires careful balancing. On the one hand, future generations benefit from prior investments. On the other, future annual revenues will be committed to servicing debt. Consideration must be paid to the distribution of the financial burden between current and future payers relative to the distribution of benefit, often referred to as "generational equity" and one of the Commission's overarching guiding principles, as articulated in Chapter 1.

Taken together, these principles can help determine when and to what extent debt financing mechanisms can be appropriately used to help meet transportation infrastructure investment needs-avoiding having to forgo or delay the benefits-without overleveraging available revenue streams, overcommitting future users and taxpayers, or masking the true need for increased underlying funding.