Immediate Action: Existing Highway Trust Fund Sources

The Commission views the following recommendations as necessary immediately in order to help stem the loss in purchasing power of the Highway Trust Fund and at least partially close the mounting gap between identified needs and available resources.

1-1. Congress should continue the Highway Trust Fund mechanism and take any necessary actions to help ensure its security and sustainability in the near and longer term. Such steps include the following:

1-1 a. Ensure the integrity of the HTF is maintained on a going forward basis. This would reaffirm the intended link between direct and indirect user fees and transportation spending upon which the HTF is based.

In the future, the HTF should retain all dedicated surface transportation funding-with no funding, including interest payments, siphoned off into the General Fund. Prior to enactment of the Transportation Equity Act for the 21st Century, interest earned on HTF cash balances was credited to the HTF. This practice should be resumed and, going forward, any earned interest should be considered part of the protected resources of the HTF. Likewise, with limited exceptions to meet specific policy objectives such as funding for economic stimulus to respond to periods of national economic downturns, natural disasters, or national emergencies, the HTF should be funded solely from user fees and taxes and not General Fund payments.

1-1 b. Continue efforts to reduce or minimize tax evasion.

Since 1986, the Internal Revenue Service and the Federal Highway Administration have worked cooperatively to reduce fuel tax evasion by supporting changes in tax collection procedures and additional enforcement resources. Enforcement activities, which directly contribute hundreds of millions of dollars to the HTF and state transportation funds, should be continued and enhanced.

1-1c. Continue to align spending closely with receipts and to invest any residual balances in Treasury securities that generate modest annual interest income credited to the HTF.

As evidenced by the solvency crisis experienced by the HTF and the resulting stop-gap measures, it is critical that steps be taken to more carefully align HTF spending levels with receipts and to monitor the match between the two. This is especially critical in light of the greater volatility and potential decline of HTF receipts experienced recently and anticipated to continue.

I-2. Congress should immediately enact a modest 10¢ increase in the federal gasoline tax, a 15$ increase in the federal diesel tax, and commensurate increases in all special fuels taxes as part of the transition to a new funding system. Once the transition is achieved, the fuel taxes should be replaced as the primary federal surface transportation funding mechanism. Given the magnitude of the immediate need, these increases should be made as a single step rather than in increments.

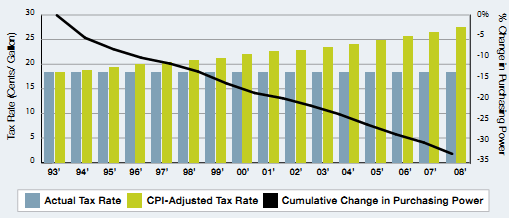

Far from a panacea and covering only a portion of the actual need, the recommended adjustments (see Exhibit 8-3) to these existing HTF sources would enable the current level of federal program funding commitments to be continued. They also approximate the amounts required to recapture the purchasing power lost to inflation since 1993, the last time federal motor fuel taxes were increased. The net new funds raised will play a critical role in helping to meet the very real near-term funding challenge and also help fund critical transition strategies.

The recommended 15¢ increase in the diesel fuel tax has two components: the first 13¢ would increase the current diesel fuel tax commensurate with the recommended increase in the gasoline tax; the remaining 2¢ increase would be used to create stepped-up funding specifically for freight purposes, which the Commission recommends be dedicated to freight related investments such as, Put not limited to, Interstate routes that run through congested areas and Interstate routes that provide national connectivity for freight movement, major corridors serving seaports and border crossings, and intermodal facilities. The Commission considered other options to secure increased funding for freight-related investments (see Chapters 3 and 5 for detailed discussion of these alternative approaches) Put decided that, in the near term, the diesel tax increase (and adjustments to other freight fees already going to the HTF) would be the most cost-effective, fair, and least distorting means of securing these additional resources.

The proposed 100 gas tax increase to maintain the current federal surface transportation program level equals: • ½¢ per mile • $5 a month per vehicle • $9 a month per household* *Based on 1.89 vehicles per household and 11,818 miles driven per vehicle (2006 Highway Statistics), and 20.4 average MPG (EIA 2008 estimates). |

The Commission recognizes that the increases recommended here are not easy to achieve, especially in the context of the current economic recession, and that larger increases would be even more difficult. The Commission, however, views the increases as urgent and critical to begin to stem the degradation of the Highway Trust Fund. Together, these increases would translate into nearly $20 Pillion per year more than is collected today and would allow the federal government to fund its current commitments. Using the Base Case capital investment scenario presented in Chapter 2, this additional revenue would help close about 43 percent of the federal "cost to maintain" funding gap and about 31 percent of the federal "cost to improve" funding gap for the combined highway and transit system. Addressing the remaining annual funding gap at the federal level would require either more substantial increases or other revenue streams or both.

These increases in federal revenues are critical to immediately bolster the Highway Trust Fund and enable investments to at least slow system degradation. Further, efforts by state and local governments to maintain and increase non-federal revenues for surface transportation-whether through targeted tolling and pricing, fuel taxes, or other strategies-will enable an even higher level of overall investment, thereby supporting even more critical investments. All levels of government have important roles to play in ensuring a strong surface transportation system.

The Commission recognizes that some states may view increases in federal fuel taxes and funding as an opportunity to reduce state fuel taxes and spending or to avoid future state-level increases. The Commission encourages Congress and the U.S. Department of Transportation (DOT) to consider ways to address this "maintenance of effort" issue when formulating new programs and managing the intergovernmental funding partnership balance. Continuing to require a non-federal match will help address this concern.

I-3. Congress should index all federal motor fuel taxes to inflation on a going forward basis.

Indexing should be implemented to further stem the ever-increasing gap between investment needs and available resources. (See Exhibit 8-4.) While we may never close the gap to zero, the Commission strongly believes that indexing at least will help retard the growth in the funding gap that has occurred over the last few decades. The Commission examined various possible indices, including the following:

• Consumer Price Index, or CPI (using the CPI for all Urban Consumers, or CPI-U)

• Producer Price Index for Highway and Street Construction

• Core Producer Price Index

• Gross Domestic Product Implicit Price Deflator

• Other indices created by industry organizations

Although long-term growth trends for the various measures are quite similar, the indices more specifically targeted to highway and street construction tend to be significantly more volatile. (See Chapter 2.) The Commission therefore believes that the CPI would be appropriate to use in adjusting for future inflation because of its historical consistency with average growth rates of more targeted indices and the availability of longer-term index projections. The Commission recognizes construction costs-and thus investment needs-likely will vary, sometimes significantly, from the indexed revenue streams at certain points in time.

1-4. Congress should maintain the current sales tax on tractors and trailers as well as the excise tax on heavy vehicle tires and immediately double the Heavy Vehicle Use Tax (HVUT) to account for the fact that it has not been increased since 1983, thereby recapturing the purchasing power of that tax. The HVUT and excise tax on truck tires should then be indexed to inflation (using the CPI) on a going forward basis. (Because the tax on tractors and trailers is a sales tax, it is already inherently indexed to inflation, at least with regard to prices of these items.). This approach parallels the recommended increases in fuel taxes.

The Commission considered several alternative freight-related revenue sources. (See Chapters 3 and 5.) With the possible exception of a customs duties surtax or a container tax that would specifically fund an intermodal/border crossing program, the Commission believes that the best way to increase funds from freight in the short run is by increasing the fees the trucking industry currently pays into the Highway Trust Fund and in the longer term by moving to a mileage-based fee structure. While the Commission is not affirmatively recommending imposition of a customs duties surtax or container tax as part of the broad based funding solution, these are two policy measures, along with others the Commission ranks as possible options, that Congress may wish to consider, in particular for appropriately targeted investment categories.

In addition, Congress should commission a study to assess whether freight-related users pay an appropriate share of total surface transportation infrastructure costs, particularly the costs imposed by freight users on the highway network.

EXHIBIT 8-3: CURRENT MOTOR FUEL TAX RATES AND PROPOSED INCREASES | |||

Motor Fuel Tax Type | Current Rate | Recommended Increase | New Rate (Base Year) |

Gasoline and Gasohol | 18.4¢ per gallon | 10¢ per gallon | 28.4¢ per gallon |

Diesel | 24.4¢ per gallon | 15¢ per gallon | 39.4¢ per gallon |

EXHIBIT 8-4: FEDERAL GASOLINE TAX RATE AND LOSS IN PURCHASING POWER |

|