1 Review of the Private Finance Initiative

The Private Finance Initiative (PFI) was introduced in 1992 as a means of harnessing the private sector's management skills and commercial expertise, to bring discipline to the delivery of public infrastructure. The overall aim of the policy was to achieve better value for money for the taxpayer by ensuring that infrastructure projects were delivered to time and to cost, and that assets were well maintained. Over the last 20 years PFI has become the form of Public Private Partnership (PPP) used most frequently in the United Kingdom and has been used across a broad range of sectors. The Government's overall objective for the delivery of public infrastructure and services is to secure value for money. There is a range of contracting approaches available to achieve this. As currently, however, it is expected that conventional procurement will continue to be used to deliver a large proportion of the future investment in public infrastructure. Experience of past projects has shown that a number of aspects of PFI are not working effectively and this has led to sub-optimal value for money in some projects. This has included a slow and expensive procurement process, insufficiently flexible contracts, a lack of transparency of the future liabilities created by PFI projects and the perception that some equity investors have made windfall gains. Some features of PFI have, however, operated as intended, delivering projects to time and to budget, creating incentives on the private sector to manage risk effectively and ensuring that assets are maintained properly during the contract term. The Government has already taken a number of steps to address the concerns with PFI and to reflect the recent changes in the economic landscape. These include: • publishing the Whole of Government Accounts in order to improve the transparency of PFI liabilities. This shows that the present value of future PFI obligations, including service charges, is £144.6 billion (2010/11); • launching the Operational PFI Savings Programme to improve the cost effectiveness, value for money and transparency of operational PFI projects; • abolishing PFI credits at the Spending Review 2010 in order to create a level playing field for all forms of public procurement; • introducing new arrangements for the assurance and approval of major projects to strengthen scrutiny and control; and • announcing a number of measures to respond to changing economic conditions, including a new temporary lending programme for PPP projects, increasing capital contributions during a project's construction period to improve affordability and the UK Guarantees programme. The Government does, however, recognise the need to go further and has, therefore, launched a new approach, PF2, to facilitate genuine partnerships between the public and private sector. Capital spending on public infrastructure is a devolved matter and so PF2 will apply in England only. |

1.1 The Government introduced PFI in 1992 as a means of harnessing the private sector's efficiency, management and commercial expertise and to bring greater discipline to the procurement of public infrastructure. Under this policy, the private sector was engaged to design, build, finance and operate infrastructure facilities through a long-term contractual arrangement. PFI was introduced to deliver high quality assets and services and better value for money for the public sector. It aimed to do this through the transfer of appropriate risks to the private sector, a clear focus on the whole of life costs of projects and an innovative approach to service delivery. The payment for PFI projects was structured to ensure that the public sector only paid for the services that were delivered.

1.2 The delivery of projects using conventional procurement normally involves the public sector contracting with the private sector to construct an asset, with the public sector providing the design and the financing itself. The public sector is then responsible for operating the asset once it is built and can outsource these operational services to the private sector under separate contracts. In many cases, however, due to the nature of short-term budgetary decisions public sector authorities do not make provisions for asset maintenance. The delivery of projects under PFI is often more complex than those delivered using a conventional route. This is due, in part, to the lengthy contract periods involved, the greater sharing of risks between the public and private sector and the integration of different aspects of the investment.

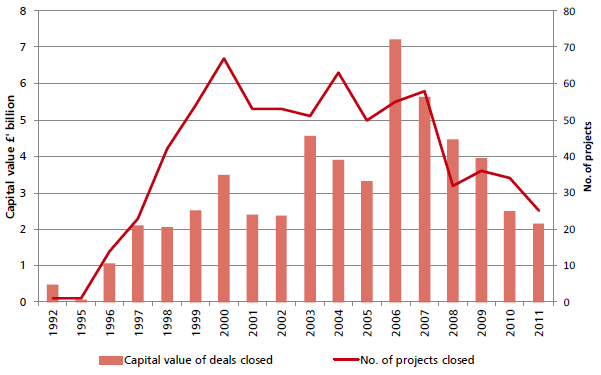

1.3 PFI has been used in the past where there has been a significant investment need for an asset followed by a requirement for ongoing services. PFI has become the form of public private partnership (PPP) most often used in the United Kingdom, with over 700 PFI projects, with total capital costs of £54.7 billion, having reached financial close. Projects have been delivered across a broad range of sectors including schools, hospitals, roads, prisons, housing, defence and waste facilities. Chart 1.A shows the spread of the delivery of these projects over time by number and capital costs and Chart 1.B shows the number of projects that have been undertaken by each Government Department.

Chart 1.A: Number of projects reaching financial close and total capital costs incurred

Figures based on departmental and Devolved Administration returns. Current projects only - does not include projects that have expired or terminated. |

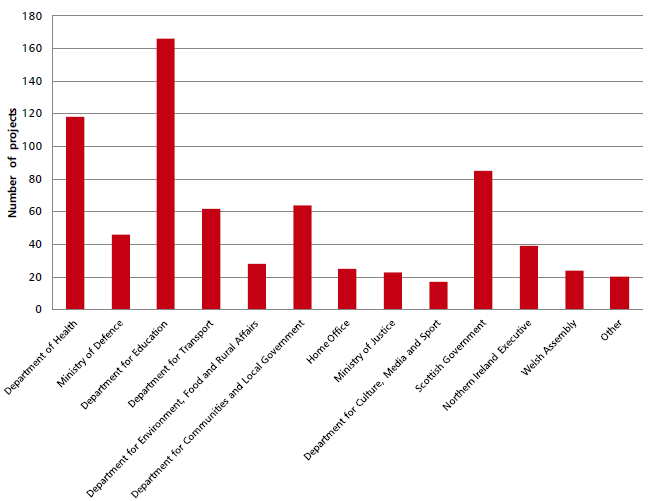

Chart 1.B: Number of PFI projects by Government Department as at 31 March 2012

Other includes the Department for Work and Pensions, HM Revenue and Customs, GCHQ, HM Treasury, Foreign and Commonwealth Office, Department for Business, Innovation and Skills, Crown Prosecution Service, Cabinet Office and the Department for Energy and Climate Change |

1.4 Since PFI was introduced, it has remained a small but important part of the Government's overall investment in public infrastructure. In the financial year 2011/12, Public Sector Net Investment (PSNI), the gross spending on investment less depreciation, totalled £26.7 billion. The capital cost of those PFI projects that reached financial close in 2011/12 was £2.1 billion. There are, however, a number of alternative approaches that can be used to deliver capital investment and this decision is based on a value for money assessment (see Chapter 7, Efficiency and value for money).

1.5 Conventional procurement will continue to be used to deliver a large proportion of future investment in public infrastructure. There are a number of key differences between conventional procurement and PFI which are outlined in Table 1.A below.

Table 1.A: Comparison of PFI and conventional procurement

Conventional procurement | |

Usually short-term design and construction contracts. | A long-term contract (c.20-30 years) integrating design, build, finance, and , sometimes, maintenance of the facility. |

Requirements tend to be specified on an input basis. | Requirements are specified as outputs to maximise private sector innovation. |

The procuring authority usually holds the risk on construction delays and cost overruns. | The private sector party holds the risk of construction delays and cost overruns to provide incentives for delivery to time and to cost. |

The procuring authority pays for the costs of construction, maintenance and services as they arise. | All costs are included in a "unitary" payment which is fixed over the life of the contract and is not payable until construction is complete and services have commenced to an agreed standard. |

The procuring authority pays for the capital costs at the beginning of the project through capital budget. | The capital costs of construction are financed by the private sector borrower, and the costs are amortised over the life of the project. |

Borrowing is financed through issuance of government gilts, managed on a Government portfolio basis. | Borrowing is financed by the private sector on a project by project basis. |

Payment for maintenance and services are not generally linked to performance. | The unitary charge payments are linked to a performance regime. Deductions may be made if services are not delivered to contractual requirements. |

There is no long-term contractual commitment for the provision of maintenance. Authorities can flex their requirements and the costs of maintenance. Only a small number of authorities put in place planned maintenance regimes. | The public sector pays for ongoing maintenance and lifecycle replacement costs as part of the annual unitary charge, and the costs are therefore smoothed across the contract term. This means that the asset is appropriately maintained over the project's life, but the costs of maintenance are effectively locked in over this period. |

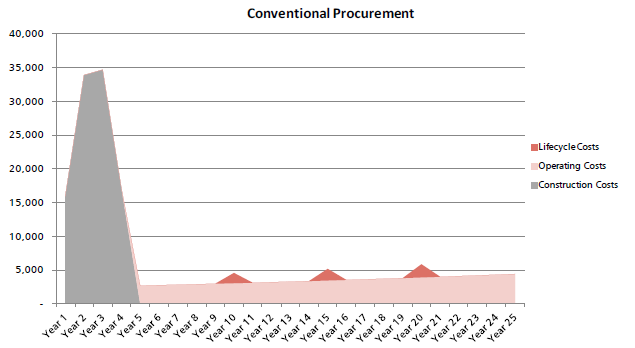

1.6 One key difference between conventionally procured projects and those procured using PFI is the timing of payments from the public sector to the private sector. Under conventional procurement, the public sector pays the capital cost of the project upfront, followed by an ongoing amount for maintenance services over the life of the asset.

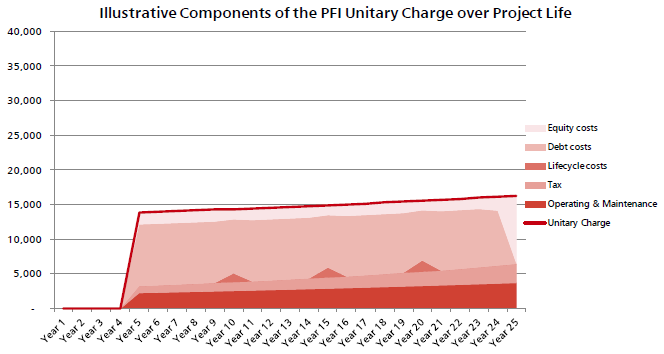

1.7 Under PFI and PF2, the public sector does not pay for the project's capital costs over the construction period. Once the project is operational and is performing to the required standard, the public sector pays a unitary charge which includes payments for ongoing maintenance of the asset, as well as repayment of, and interest on, debt used to finance the capital costs. The unitary charge, therefore, represents the whole life cost associated with the asset. Chart 1.C provides an illustrative payment profile for a conventionally procured project and a PFI project. Chart 1.C also provides an illustration of how the annual unitary charge payment breaks down, for a typical accommodation PFI project, into the components of debt, equity, lifecycle, operating and maintenance costs and tax. Under conventional procurement, the costs include construction, operation and lifecycle.

Chart 1.C: Illustrative payment profile for a conventionally procured project and a PFI project

Source: HM Treasury |