Budgeting for PFI projects

1.11 Departments have separate budgets for resource and capital spending. Resource spending (RDEL) includes current expenditure such as pay or procurement. Capital spending (CDEL) includes new investment. The scoring of the project in departmental budgets depends on whether the project is classified as on or off balance sheet under ESA95.

1.12 If a central government project is deemed to be on balance sheet under ESA95, then the capital value of the project (i.e. the debt required to undertake the project) is recorded as CDEL in the first year of operation; and the interest, service and depreciation are recorded as RDEL each year unitary charges are paid.

1.13 If a central government project is deemed to be off balance sheet under ESA95, then there is no impact on the department's CDEL in the first year of operation. The full unitary charge (including interest, service and debt repayment) does, however, score in RDEL each year. Around 85 per cent of past PFI projects have been considered off-balance sheet under ESA95.

1.14 Departmental budgets are set as part of the Spending Review process. The Government has always been clear that value for money and not the accounting treatment is the key determinant of whether a PFI scheme should go ahead.

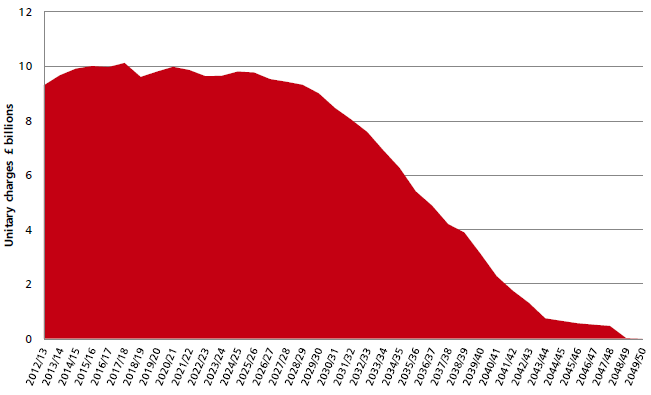

1.15 In order to ensure transparency, the Treasury has regularly published estimated future unitary charge payments for all signed PFI projects. An updated profile of these unitary charge payments is shown in Chart 1.D. The unitary charges are presented as nominal figures, i.e. they include an assumption for future inflation and have not been discounted.

Chart 1.D: Estimated future unitary charge payments (in nominal terms, undiscounted) under signed PFI projects

Source: HM Treasury. Figures are based on departmental and Devolved Administration returns. |