Insurance

6.10 Insurance is taken out to guard against the occurrence of particular risks and is especially useful to deal with low incidence, high impact risks (such as the loss of a building or the death of a person). Accordingly, it has been standard practice for contractors to insure PFI facilities and to pass the cost of this back to the public sector authority1. The underpinning assumptions for this are that:

• risk is best taken by the party best able to manage it. Under PF2, it is the contractor who is responsible for designing, financing, building, repairing, and rebuilding the facility (if it is damaged or destroyed). The authority will only pay for the service if it is provided. The risk, therefore, of guarding against events which interrupt the service sits naturally with the contractor; and

• lenders require insurances (of a detailed nature) to be taken out for facilities which they have financed; key insurances for lenders are material damage and business interruption.

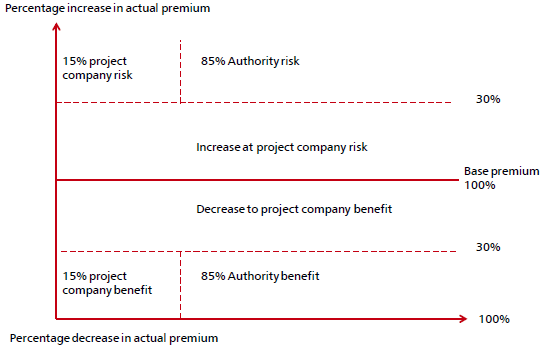

6.11 Since 2006, standardised drafting for insurances and in particular, premium risk-sharing for operational period insurances have been applied to PFI contracts. Under these arrangements construction phase insurances are priced and fixed at financial close and operational insurances are estimated (with the authority taking 85 per cent of the risk of price change resulting from general market movement beyond a 30 per cent nil change band up or down) and priced in the financial model. This is illustrated below:

| Chart 6.A: Insurance

Source: HM Treasury |

_________________________________________________________________________________________

1 The contractor's estimated insurance costs being included as one of the costs in the financial model which determines the monthly unitary charge.