Global debt market conditions

8.5 Prior to 2008, there was an active bond market for UK and international PFI/PPP projects, providing both fixed and inflation linked debt. These bonds benefitted from a guarantee3, or 'wrap', provided by one or more monoline credit insurers. Bond investors therefore invested in a AAA product, on the basis of the monolines' credit ratings, with the monolines assuming the project risk in return for a fee.

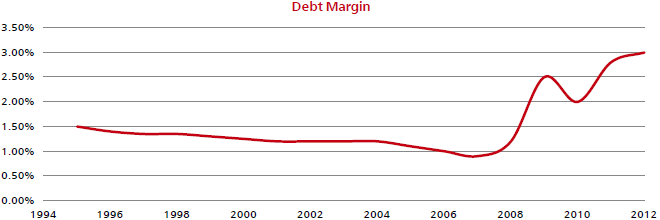

8.6 Project bonds provided an alternative funding source to bank loans and this competition drove down debt pricing. During this period the margin on a bank loan and the coupon on a bond (plus the monoline guarantee fee) often equated to around 1.00 per cent p.a. during construction and operations and in some cases even less.

8.7 As part of other business activities monolines also provided guarantees of other cashflows including mortgage book securitisations and other collateralised loan obligations. In 2007, the 'credit crisis' hit debt markets, initiated by loan defaults on 'sub-prime' mortgage books. Exposures to these losses resulted in the downgrade, or withdrawal of rating, of all monolines4 active in the European project finance markets. Following the loss of the monolines' AAA credit rating investors ceased investing in monoline wrapped project bonds.

8.8 Since the demise of the monoline industry, PFI projects have been largely dependent on the bank loan market as the provider of long-term debt finance. Banks continued to lend to PFI projects following the onset of the financial crisis, recognising the credit quality of these assets, albeit it at a higher loan margin reflecting their rising cost of borrowing in the inter-bank (LIBOR) market. Loan pricing stabilised during late 2009 at margins of c.2.50 per cent p.a. and even began to fall in 2010 before the euro sovereign debt crisis combined with a downturn in the global economy had a major impact on debt markets. It became increasingly challenging to raise private finance for projects.

8.9 At the same time, in response to the financial crisis, a new global regulatory standard on bank capital adequacy, stress testing and market liquidity is being introduced. Basel III will require banks to set aside more capital against their risk-weighted assets. The consequence of this regulatory requirement is that loan pricing will increase to reflect the banks' own higher cost of capital. For long duration loans the impact on pricing is much greater. Additionally, many banks have previously borrowed short-term money to lend long term, causing them to recognise losses when short-term funding costs increased sharply. Management of these banks have reassessed their long-term loan businesses and in some cases have withdrawn from the market for now, after significant write downs of historic business.

8.10 As a result, the cost of long-term borrowing for infrastructure projects has increased sharply and the availability of long-term bank debt has materially diminished. In some cases traditional project finance banks have withdrawn from the market altogether. Where long-term bank finance is available, margins are now generally priced in excess of 3.00 per cent p.a. in the construction phase and include a margin ratchet mechanism to incentivise early refinancing. This pricing is not indicative of the actual project risk by any reasonable historic benchmark but instead is a reflection of banks' own long-term cost of funds.

| Chart 8.A: Illustration of PFI debt margins

Source: HM Treasury |

8.11 PFI projects were typically structured to be on the boundary of investment grade (i.e. in the BBB/Baa range). It could be argued that debt pricing observed in mid 2000 was actually underpriced in relation to project risk, therefore, historically the tax payer has received better value for money from PFI projects during this period. It is unrealistic to expect debt pricing to revert to pre-2008 levels but equally Government expects pricing to be reflective of actual project risk and not banks' funding costs.

_____________________________________________________________________________________________________

3 Guarantee to pay interest and principal as they fall due.

4 Only one monoline credit insurer active in these markets maintains a rating higher than BBB+.