7.3.1 Existing capacity and services

The Universal Service Obligation requires Telstra to provide all Australians, wherever they live or conduct business, with access to a voice service on reasonable request.

For mobile services:

■ over 99 per cent of the Australian population has access to voice services mobile networks;

■ 81 per cent of premises have access to 3G mobile broadband services; and

■ 59 per cent of premises have access to 4G services.250

Broadly, service levels are good in the competitive urban mobiles market, reasonable in the fixed line urban market and services progressively deteriorate for both mobiles and fixed line services as one moves to rural and more remote areas. The mobile market has the lowest level of regulation, while fixed line is more regulated with fewer competitive infrastructure providers. Services in rural and remote areas are generally subsidised, either through direct subsidy from governments, or through industry cross-subsidies. International comparisons indicate that Australia's mobile services are closer to world's best practice than our fixed line services.251

The Australian mobile network is more competitive as there is no incumbent operating a legacy network. It is therefore easier for new entrants to compete than in the fixed line network.

For fixed line internet services:

■ 91 per cent of premises have some access to ADSL technology. However, broadband services may be limited in some cases, such as where premises are too far from and exchange or areas with no additional capacity;

■ 28 per cent of premises have access to a high speed internet platform (fibre or hybrid fibre); and

■ 6 per cent of premises do not have access to fixed broadband services.

The availability and quality of fixed broadband services is generally much higher in the major cities than in other parts of Australia. Across all areas outside the cities, around 80 per cent of premises receive the lowest quality fixed broadband rating. However, there are exceptions to this. A share of Australia's regional population lives in small towns which may have access to superior fixed lines services than some suburban areas. Additionally, there are pockets of poorly served premises within urban areas, despite close proximity to areas with high quality service.

In 2009, the Australian Government announced the establishment of NBN Co Limited (NBN Co) to deliver wholesale high-speed broadband across Australia. NBN Co is a wholly owned Commonwealth company, or Government Business Enterprise, which operates on a commercial basis supported by public funding.

In April 2014, NBN Co was issued a new Statement of Expectations. This included a requirement to use an 'optimised multi-technology mix' on an area by area basis, to achieve download data rates of at least 25 megabits per second (Mbps) to all premises, and at least 50 Mbps to 90 per cent of fixed line premises, as soon as possible. This service level requirement, in combination with the requirement to prioritise areas identified by the Broadband Availability and Quality Report as poorly served, is expected to reduce service disparities between urban and rural areas over the next five years. These requirements are to be achieved within the constraints of a public equity capital limit of $29.5 billion.252

Under current arrangements, fixed line services will be delivered at a uniform cost across the country, using the returns gained from operations in commercially viable areas to support the cost of rolling out broadband services to regional and remote areas. NBN Co is using a combination of fibre to the premises, fibre to the node and fixed wireless networks and satellite services in regional and remote areas. The Bureau of Communications Research, within the Department of Communications, is undertaking an assessment of the costs of NBN Co's fixed wire and satellite services in regional and remote areas. In the second half of 2015 the Bureau of Communications Research will provide options to Government for replacing the current National Broadband Network (NBN) cross-subsidy embedded in its wholesale access prices with more transparent funding arrangements.253

The fixed wireless services use cellular (TD-LTE or 4G) technology to deliver wireless internet access from a base station, or tower, to antenna installed on individual homes. The network has been designed to deliver download speeds of up to 25 Mbps, with a set number of premises served by each facility.

Satellite services will be delivered using two NBN Co-owned satellites that are able to cover the entire Australian mainland and islands. The satellites will use 101 spot beams, with each beam having its own bandwidth capacity split across end users in the beam. Prior to the launch of the long-term satellites in 2015, services are being provided by leased satellite capacity.

By mid-February 2015, NBN Co reported that more than 818,000 premises had been passed by fixed line or covered by wireless technology, with activation of the NBN completed to more than 346,000 premises.

For mobile services, the private sector can be expected to progressively introduce higher capacity services in response to market forces and technological change. Telstra and Optus purchased access to the radio-telecommunications spectrum in the 700 MHz band for almost $2 billion in 2013. This new spectrum will provide a significant boost to 4G mobile capacity and coverage for some time, but may eventually be fully utilised. In that case more spectrum will be required.

Audit finding 69. The quality of telecommunications service across Australia is mixed, with generally good services in cities and with lower quality services in rural areas and some outer urban areas. The NBN is expected to reduce service disparities within the next five years. |

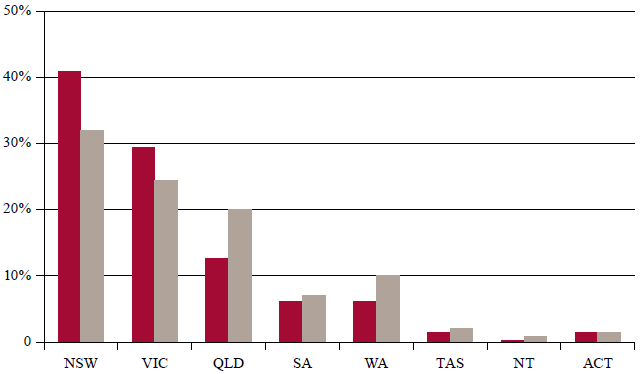

The DEC of telecommunications services across Australia was $21 billion in 2011. The share of this total across the states and territories is shown in Figure 41, with each state and territory's share of the national population included for context.

The data indicates that a relatively high proportion of telecommunications infrastructure value-add is located in NSW and Victoria, which is likely to reflect the concentration of commercial activity in Sydney and Melbourne.

Figure 41: Share of total telecommunications DEC and national population by state/territory - 2011

|

|

|

| Share of national telecommunications DEC | |

| Share of national population | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Source: ACIL Allen Consulting (2014a)

In 2011-12, the Australian telecommunications market generated total revenue of $40.8 billion and capital expenditure of $47.1 billion. Capital stock was estimated to be $124 billion.254

Across a range of services, the Australian telecommunications market is dominated by Telstra. In 2012-13, Telstra held 63 per cent of the retail fixed voice market, 43 per cent of the mobile telecommunications market, and 42 per cent of the retail broadband market. It is also the present provider of infrastructure such as the copper access network used by other businesses to provide services to customers, although NBN Co has recently purchased this copper network. Other major providers include Optus, Vodafone Hutchison Australia, iiNet and TPG.

Mobile broadband has led to major productivity improvements for Australian businesses, and is estimated to have increased Australian GDP growth rate by an annual average of 0.28 per cent from 2007 to 2013. It is estimated that the Australian economy would have been $7.3 billion smaller between 2006 and 2013 without the additional productivity benefits of mobile broadband services.255

_________________________________________________________________________________

250. Department of Communications (2013)

251. Organisation for Economic Cooperation and Development (2013b)

252. NBN Co (2014)

253. Australian Government (2014c)

254. ACIL Allen Consulting (2014a)

255. The Centre for International Economics and Analysys Mason (2014)