Wider contract management problems

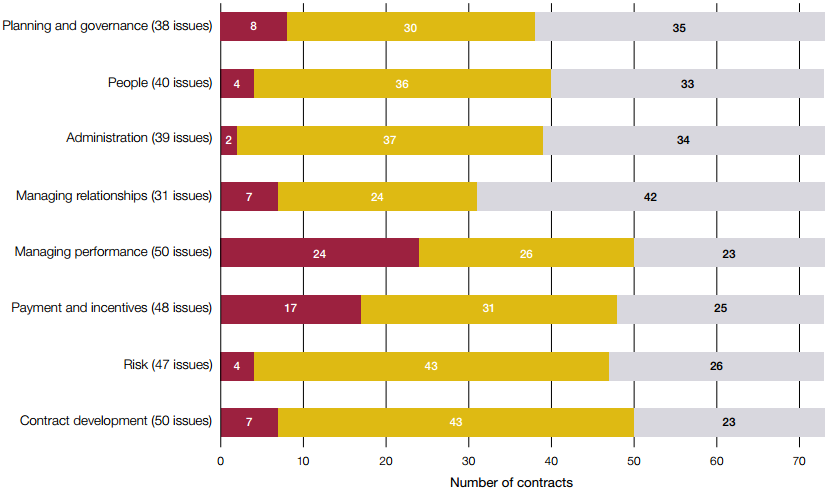

1.8 The reviews also identified a range of contract management weaknesses across government (Figure 3). Contracts were tested against the 8 areas of our 2008 good practice framework and problems were found across all areas. Contract management weaknesses and their causes are examined in more detail in Part Two of this report.

Figure 3 The reviews found issues against all areas of our framework Contract management framework area

Notes 1 Includes the cross-government review (28 contracts with G4S and Serco, all of which were tested for overbilling), the Ministry of Justice (17 reviewed, of which 7 were also tested for overbilling), the Home Office (13 additional to the cross-government review, of which 5 were tested for overbilling) and the Department for Work & Pensions (15 contracts, which were only tested against the framework). This does not include a further 20 Ministry of Justice contracts tested only for overbilling. 2 In total 73 contracts (with various contractors) were reviewed against the NAO framework and 60 were tested for overbilling. Source: National Audit Office analysis of government reviews of contract management |

Weaknesses which create material risk of overbilling

Weaknesses which create material risk of overbilling Other weaknesses

Other weaknesses No issues detected

No issues detected1.9 It is likely that there is further overbilling in other contracts across government. The reviews found particular weaknesses in managing performance. These include weak verification of information provided by contractors. For example, in one contract the Ministry of Defence's poor record-keeping meant the reviewers could not verify whether a contractor provided the number of staff billed for, although the service was satisfactory. The reviews tested billing in 60 contracts and controls in 73 contracts, but central government has well over 100,000 contracts.

1.10 Weaknesses in contract management have far-reaching consequences for departments:

• Fraud and error risk

Without basic scrutiny of payments and performance, departments rely on the contractor to interpret the contract correctly, and meet the standards the public expects. For instance, better scrutiny of payments and understanding of the contract could have prevented the overbilling found in the Ministry of Justice contracts referred to authorities.

• Not managing risk

Departments often do not understand what the risks on their contracts are, or who bears them. They then do not manage the risks properly. For instance, the Ministry of Defence's failure to provide ICT infrastructure critical to the success of the Army's recruitment contract with Capita impacted on recruitment activities and increased costs.

• Risk of contractual dispute

Without good change control, departments risk not knowing what the contract requires the supplier to do. Without both parties understanding the contract the relationship with the supplier suffers, potentially leading to disagreements. For instance, ambiguities in the Home Office's immigration removal centre contracts meant that disagreements were difficult to settle, often to the contractors' favour.

• Performance deductions are not always enforced

For instance, the Home Office did not enforce penalties for defects in COMPASS asylum seeker accommodation as it felt that the contracts were at an early stage. Also, as the contractors could pass the penalties down the supply chain, the Home Office felt enforcing penalties may have threatened subcontractors' financial stability and led to overall service failure.

• Not understanding how contracts meet policy objectives

Senior staff do not always understand what their contracts are achieving, which leaves departments unable to shape contracts and contractual incentives to their needs or work with contractors to get the required results. For instance, poor senior oversight meant the risk profile on the Department for Work & Pensions' Work Programme was changed in the contractors' favour.

• Use of commercial levers

Absent data, or limited scrutiny of performance data, means departments do not understand how a service is provided, or how to challenge poor performance. Without market testing, departments can be locked into inflexible or expensive contracts which they cannot revise to reflect innovation or learning from the outside world. Not using performance incentives means that departments do not challenge poor performance. For instance, pressures to find cost savings led HM Revenue & Customs (HMRC) to trade away some of its negotiating power and hindered its ability to get strategic value from its long-term Aspire ICT contract. When negotiating cost savings in response to successive funding settlements, HMRC conceded many of its commercial safeguards through major renegotiations of the contract between 2007 and 2009, including the right to share in supplier profits when they were higher than target and the right to compete services. HMRC estimates it achieved savings of £750 million through such negotiations. Since 2012, HMRC has negotiated some of these commercial controls back.19

_________________________________________________________________________________________________________

19 Comptroller and Auditor General, Managing and replacing the Aspire contract, Session 2014-15, HC 444, National Audit Office, July 2014.