Spending controls

4.2 Spending controls are one way that the centre of government can ensure that approaches to delivering technology solutions are consistent across government. Controls can be used to: meet savings targets by preventing unnecessary spending; improve transparency about spending; and enforce common standards and approaches.

4.3 Government introduced digital and technology spending controls in March 2011 following spending restrictions imposed in May 2010. These controls form part of a wider framework of expenditure controls that HM Treasury and the Cabinet Office use, alongside departments' own internal arrangements. Departments submit digital and technology spending requests to GDS for approval at key stages in a project or programme according to the type of expenditure. Digital projects - ie those that directly affect online services - are subject to much lower financial thresholds than spending on administrative systems (Appendix Three).

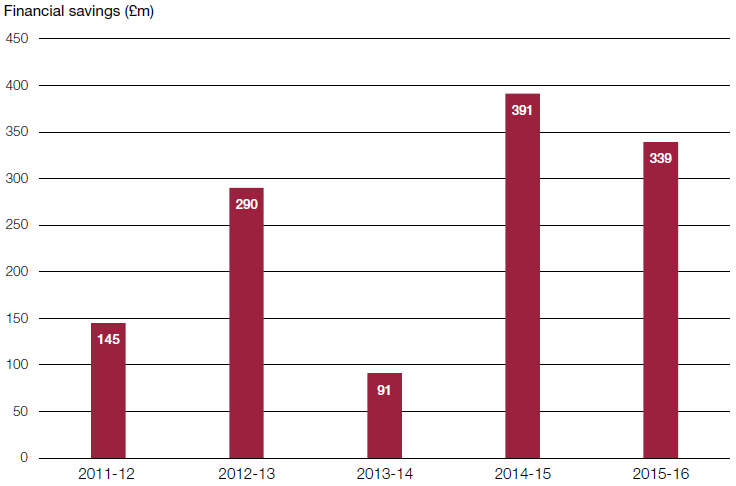

4.4 Spending controls have delivered savings and made spending decisions more open. In January 2013, we concluded that the Efficiency and Reform Group's actions on spending controls had helped departments make substantial cuts in spending.22 Departments submit around 500 spending requests each year, with these expected to show how proposals comply with standards.23 For the five years to April 2016, GDS reported savings of £1.3 billion through spending controls (Figure 10).24

_________________________________________________________________________________________________

Figure 10

Financial savings from spending controls over time

GDS has reported savings totalling £1.3 billion from its spending control interventions

Notes

1 The Government Internal Audit Agency conducts a validation exercise for savings. This review is to provide assurance that the numerical parts of savings and disposals are accurately calculated and backed up with reasonable evidence and that the way claims are made is reasonable and fair. The Agency selects and reviews a sample of projects where savings have been claimed and identifies adjustments to claimed amounts where necessary. We discuss the process in more detail in our report: Comptroller and Auditor General, The impact of government's ICT savings initiatives, Session 2012-13, HC 887, National Audit Office, January 2013.

2 For its review of 2015-16 savings, the Government Internal Audit Agency concluded that it was able to offer moderate assurance that the evidence base supports claimed savings and assertions with some weaknesses. The Agency gave moderate assurance because claimed savings are based on business case projections and the actual cost reductions will not be realised and confirmed until each project is completed.

Source: National Audit Office analysis of Government Digital Service's savings calculations

_________________________________________________________________________________________________

4.5 While spending controls can play a valuable role in strengthening cross-government approaches, the process raises the following concerns:

• Linking savings to transformation

In January 2013, we assessed that less than half (41%) of spending control savings were likely to be sustainable over the longer term.25

• Ensuring proportionate effort is spent on controls

GDS data shows that requests of up to £1 million accounted for 47% of its spending controls team's time on spending controls. At the same time, these requests produced only 1% of the financial savings claimed in 2015-16 (Figure 11).

• Reducing burdens on departments

Although GDS generally meets the agreed targets for assessing applications, when combined with other approval processes, the overall process can be long and require repeated reviews.

• Ensuring departmental compliance

Departments regularly submit spending proposals for GDS approval at a late stage in the development of programmes and projects. Our examination of 2016-17 data found that 40% of programmes and projects relating to applications received at the full business case stage had not been reviewed previously by GDS.

4.6 GDS is piloting a new approach to spending controls so that it can target limited resources more effectively and reduce the burden on departments. The new model - to be implemented more widely from April 2017 - involves reviewing departments' 18-month plan for future technology and digital projects. GDS plans to make greater use of department-led peer review to help overcome the relatively small size of its own assurance teams.

_______________________________________________

22 Comptroller and Auditor General, The impact of government's ICT savings initiatives, Session 2012-13, HC 887, National Audit Office, January 2013.

23 GDS data since April 2014.

24 Over this period, GDS also reported savings of £0.6 billion through wider initiatives, for example migrating websites to GOV.UK.

25 Comptroller and Auditor General, The impact of government's ICT savings initiatives, Session 2012-13, HC 887, National Audit Office, January 2013. Sustainable savings are defined as long-term savings that are likely to occur every year for the foreseeable future.