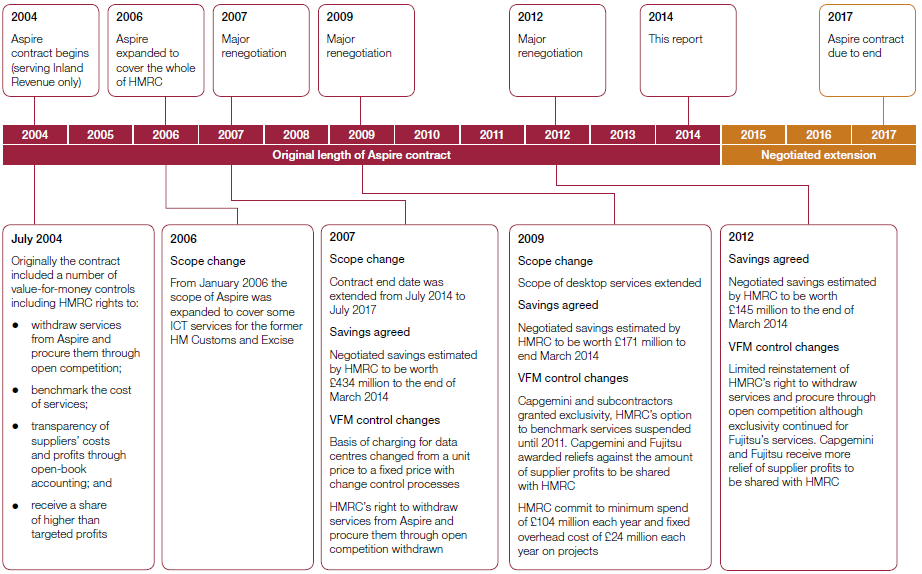

How the contract evolved

3.2 Our report on procuring Aspire found the contract promised HMRC substantial savings when compared to the previous contract and that HMRC managed the transition to the new contract adequately.19 HMRC needed to build on this successful start by taking opportunities from technological change, including reducing costs. It also needed to know what long-term value it was getting.

3.3 Since 2004, HMRC has done four major and 121 minor contract renegotiations.20 One aim in renegotiating the contract was to reduce prices, in response to financial pressures and reductions in technology prices. Through these negotiations, HMRC and Capgemini agreed to change the Aspire contract, including:

• changing scope, such as expanding the contract to cover parts of the technology estate of the former HM Customs and Excise;

• extending the contract by three years;

• changing prices to make savings for HMRC; and

• adjusting the value-for-money controls (Figure 8).

3.4 The combined effect was that HMRC achieved year-on-year savings but conceded many of the controls that had been built into the contract to safeguard value for money. Since 2012, it has negotiated some controls back, including the right to procure certain services outside of the Aspire contract.

| Figure 8 There have been four major negotiations, each triggered by HMRC. These have substantially changed the cost and risk profile of the contract

Source: National Audit Office |

________________________________________________________________________________________________

19 Comptroller and Auditor General, HM Revenue & Customs: Aspire - the re-competition of outsourced IT services, Session 2005-06, HC 938, National Audit Office, July 2006, pp. 4, 15 and 19.

20 These numbers are additional to routine change controls.