Supplier profits

3.19 The changes to the scope and duration of Aspire, shown in Figure 9, will have increased Capgemini's return on its original investment. HMRC has 'open book' arrangements with the main Aspire suppliers so it can scrutinise their profits. Between July 2004 and March 2014, Capgemini and Fujitsu made a combined profit, as measured by the contract, of £1.2 billion.22 This is 15.8 per cent of the revenue they made in that period. It is more than twice the £500 million modelled in 2004, which was then equivalent to a profit margin of 12.3 per cent. The additional profit should be considered in the light of the additional work HMRC has commissioned through the course of the contract and whether it has therefore received proportionally more business value, innovation or risk transfer than expected at the outset. However, HMRC has not evaluated the reasonableness of the increased profit achieved by suppliers. HMRC, believes that the margin is comparable with industry margins for similar services, though the scale and breadth of the contract makes like-for-like comparisons difficult.

3.20 HMRC has the right under the contract to receive some of the additional profit that Capgemini and Fujitsu earned, through a profit-sharing agreement. However, during the major negotiations, HMRC gave Capgemini and Fujitsu reliefs against this (Figure 8). As a result, HMRC received payments worth £16 million as its share of profits earned in the period. Without the reliefs, it would have been entitled to £71 million.

3.21 Capgemini and Fujitsu's profits have been stable for much of the contract's life. In the 39 quarters between July 2004 and March 2014 there has only been one quarter, the one ending June 2008, when suppliers failed to make a profit. In June 2008, Capgemini incurred a significant redundancy cost, which caused a quarterly loss but reduced future costs.

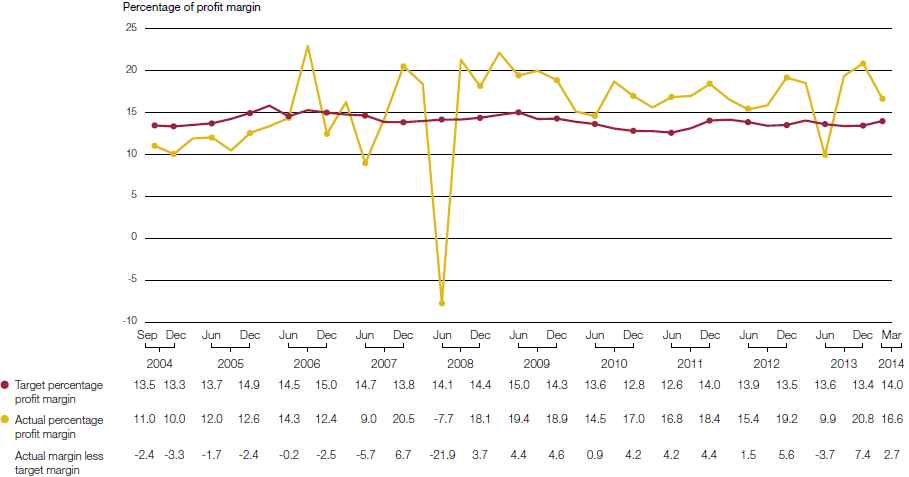

3.22 The Aspire contract specifies a target profit margin for Capgemini and Fujitsu that varies depending on the type of work, and has averaged 14.0 per cent between July 2004 and March 2014. There have only been 12 quarters where their actual profit margin was less than the targeted margin. The quarter ending December 2007 marked a tipping point in the contract's profitability. Up to the end of September 2007, the average profit margin was 13.6 per cent and there were 10 quarters with a margin below target. From the quarter ending December 2007, the average profit margin was 16.9 per cent and there were only two quarters with a margin below target (Figure 11 overleaf).

| _______________________________________________________________________________________________________ Figure 11 The quarter ending December 2007 marked a tipping point in the stability of margins under Aspire

Notes 1 Each service and project line has a specified target profit margin. The overall target margin has been calculated by weighting these by the actual amount of revenue recognised for a project or service in a quarter. This is then compared to the actual percentage profit margin. 2 Numbers may not sum due to rounding. Source: National Audit Office analysis of HM Revenue & Customs' data _______________________________________________________________________________________________________ |

________________________________________________________________________________________________

22 The open-book rules in the Aspire contract establishes a way of measuring profit that combines what has been earned by Capgemini and Fujitsu. It is also measured after cost of capital charges and some, but not all, overheads have been deducted. This means that it is not directly comparable to profits either these, or other suppliers, report publicly in their annual accounts.