Change in financing

2.31 Most planned expenditure for the new core training is for buying and maintaining aircraft. The Department designed Ascent's contract assuming that it would finance these costs through the private finance initiative (PFI). This assumption changed, which challenges overall affordability. Overall funding for the new core training was also reduced from a forecast £6.8 billion to £3.2 billion.

2.32 Although the amount expected to be spent on the new core training was reduced, a change in accounting rules for PFI caused funding issues.11 Funding from central government is allocated as either capital or resource. The Department's original funding was based on using PFI resource funding to procure and support fixed-wing and helicopter training aircraft. However, changes in the accounting rules for PFI mean the Department is now buying the remaining training aircraft differently. Aircraft for helicopter training will be bought through conventional procurement. Fixed-wing training aircraft will still be bought through PFI but will be paid for over a shortened, five-year repayment period.

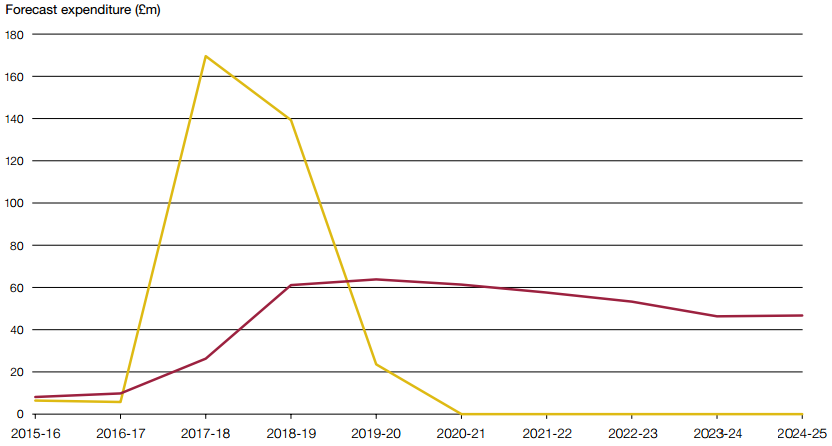

2.33 Before the changes in financing, the Department forecast the costs of the new core training would be spread over its 25-year contract with Ascent. The changes mean that a large amount of unplanned capital funding is now needed up front to finance aircraft procurements. For example, the Department had assumed that capital expenditure would be around £200 million over the 25-year life of Ascent's contract, compared to resource expenditure of £6.6 billion. Capital expenditure for the fixed-wing contract alone will now total £345 million between 2015-16 and 2020-21 (Figure 13). It has taken the Department time to identify the extra capital funding required.

2.34 The requirement for the Department to fund training aircraft using capital funding meant that it faced particular challenges with funding for the new helicopter training package. In 2012, it identified a £496 million capital funding shortfall. Further work by the Department to reduce costs then decreased this shortfall to £388 million. It then explored options to address the remaining shortfall, including delaying the start of the new helicopter training until 2025. However, it could not do this when it found it did not own the training aircraft it uses. The existing provider also did not wish to sell the aircraft. The Department has instead had to extend the existing helicopter training contract by six years to 2018. No further extensions of the contract are possible without breaking EU procurement law. A solution to address the funding shortfall was agreed between the Department and the three services in early 2015. Helicopter training is now expected to start in April 2018.

Figure 13 Capital versus resource expenditure for the fixed-wing training contract The Department had to identify a large amount of unplanned capital funding between 2015-16 and 2020-21 to finance aircraft procurement

Note 1 Resource expenditure of £424.2 million is forecast between 2025-26 and 2032-33 but is not shown on this chart. Source: Ministry of Defence |

Resource expenditure

Resource expenditure Capital expenditure

Capital expenditure2.35 As well as postponing the start of the new fixed-wing and helicopter training, the funding challenges have led to extra costs. These include:

• costs for staff and external advisers to manage the extended procurement of the fixed-wing and helicopter contracts;

• a cost of £300 million to extend the existing helicopter training contract, although some of this cost is offset by the Department not paying for the new helicopter training until its 2018 start; and

• having to continue using ageing fixed-wing training aircraft that are increasingly unreliable and costly to support.

2.36 The Department still faces cost pressures and is seeking to identify further opportunities to reduce new core training costs. Ascent has agreed to work with the Department to look for savings but the contract does not effectively incentivise Ascent to do so, particularly as its earning potential has already been greatly reduced.

________________________________________________________________________________________________________________________

11 PFI deals use private sector funding to spread much of the cost of large capital projects (such as introducing new core flying training) across the duration of a contract. Previously, PFI deals were not always recorded on balance sheet. In such cases, no up-front public sector capital budget cover was required. In April 2009, the introduction of International Financial Reporting Standards changed the rules on the balance sheet treatment of PFI. The change means that much of the costs of introducing new core training now has to be on balance sheet. This means that public sector capital expenditure on the new training has to be managed within the Department's capital spending allocations.