Optimal Risk Sharing Contracts

PPPs cannot rest on the claim that they relieve strained budgets. As mentioned above, one justification of PPPs is that bundling may enhance productive efficiency. An additional advantage of PPPs is that they reduce the sums flowing through the public budget, reducing the inefficiencies associated with subsidy transfers. In this section we derive the optimal contract when subsidy financing is less efficient than user-fee financing (Engel et al. 2008).

When thinking about the risk allocation implied by PPPs, what matters is the inter-temporal risk profile of cash flows, not the year-to-year risk profile. This has interesting implications: for low and high demand projects, an optimal PPP contract replicates the net cash flow streams of conventional ('public') provision. Under privatization, the project is sold for a one-time payment and all risk is transferred to the firm. Moreover, the link between the project and the public budget is permanently severed. This is not the case with a PPP, where at the margin cash flows from the project always substitute for either taxes or subsidies. The conclusion, then, is that from a public finance perspective there is a strong presumption that PPPs are analogous to conventional provision-in essence, they remain public projects, and should be treated as such (Engel et al, 2008).

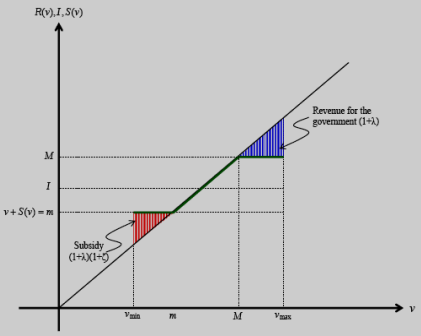

Optimal risk-sharing contract: overview The tradeoff faced by the planner when some of the resources are wasted in the process ( ζ > 0) is the following: On the one hand, she would like to utilize user fee revenues as far as possible to compensate the concessionaire, in order to avoid paying subsidies. On the other hand, using only user fees may expose the concessionaire to excessive risk, and an efficient contract would insure against low demand states through subsidies.

The figure above shows how the trade off is resolved optimally when Vmin < I < Vmax i.e., there are some states of demand in which user fee revenues is smaller than I while there are others in which revenues are larger than I ). The horizontal axis plots the support of v while the vertical axis shows the total revenue received by the concessionaire in each state, R(v) + S(v). To derive the optimal contract, note that in state v the planner will only resort to subsidies after exhausting user fees-otherwise, it could slightly reduce subsidy payments, which would save (1 + λ)(1 + ζ) - α; and increase R(v) which would cost only 1 + λ - α. Thus, R(v) < v ⇒ S(v) = 0 In these states the concession lasts indefinitely, for otherwise they would be high demand states. But no subsidies are paid out by the government, for otherwise they would be low demand states. It follows that R(v) = v and S(v) = 0 . Source: Adapted from Engel, Fischer and Galetovic. 2008. 'The Basic Public Finance of Public-Private Partnerships'. Cowles Foundation Discussion Paper No. 1618. Yale University. See paper for detailed model. |

Transparency of risk allocation [Brazil: Lei 11.079, Art. 5] Art. 5. The clauses of public-private partnership contracts shall be in accordance with the provisions of art. 23 of Act 8987, dated February 13th, 1995, as applicable, and shall also state: III - the sharing of risks among the parties, including those that refer to acts of God, force majeure, acts of State and unforeseeable events; [Mexico: Acuerdo Secretaria de Hacienda Diario Oficial 9 Abril 2004] 20. Las dependencias y entidades deberán presentar las solicitudes de autorización de proyectos para prestación de servicios ante la Secretaría, a través de las Direcciones Generales de Programación y Presupuesto sectoriales. En el caso de entidades sectorizadas, la solicitud deberá ser presentada por la dependencia coordinadora de sector y, en el caso de las entidades no sectorizadas, la solicitud deberá presentarse por la entidad, directamente a las citadas Direcciones Generales. 21. Las solicitudes a que se refiere el numeral anterior deberán acompañarse de la siguiente información: VI. Los elementos principales que contendrá el contrato de servicios de largo plazo que se celebraría entre la dependencia o entidad contratante y el inversionista proveedor, incluyendo: d) Los riesgos que asumirán tanto la dependencia o entidad contratante como el inversionista proveedor. |

Transparency of the liabilities, undertakings, commitments, guarantees, and contingent liability [Mexico: Acuerdo Secretaria de Hacienda Diario Oficial 9 Abril 2004] 32. Las dependencias y entidades deberán enviar a la Secretaría, por conducto de la Dirección General de Programación y Presupuesto sectorial que corresponda, a más tardar el último día hábil de septiembre, la actualización de los montos correspondientes a obligaciones de pago para ejercicios fiscales subsecuentes que se hayan asumido en los contratos de servicios de largo plazo. La Secretaría incluirá dicha información en el proyecto de Presupuesto de Egresos de la Federación del siguiente ejercicio fiscal. [Brazil: Lei 11.079, Art. 5] The clauses of public-private partnership contracts shall be in accordance with the provisions of art. 23 of Act 8987, dated February 13th, 1995, as applicable, and shall also state: II - the penalties applicable to the Public Administration and to the private partner in case of non-compliance with contractual obligations, which shall always be determined proportionately to the magnitude of the offence committed and to the obligations assumed; VI - the facts that trigger public sector payment default, the means and terms for reestablishing the payment stream and, if applicable, the form by which guarantees are enforced; |