Availability Payments and Performance Payments

Availability payments should relate to the usability of the asset(s). In the case of the provision of a building the availability measure could take into account the importance of each part of the building by:

• Measuring the environment of the building to make sure that it is within specific limits (often known as availability criteria). Any breach of these limits results in a deduction from the availability payment or when social and environmental safeguards are not met

• The size of deduction should relate to importance of area and period

It is important to avoid large sums of money being deducted from contractors for small transgressions, as this would be unfair. This situation can be avoided by the contractor given a reasonable period to rectify any problem but once this period is exceeded the deductions it can then be accelerated to encourage the contractor meet the requirements of the PPP/PFI contract more quickly.

Deductions from payments to contractors arising from any unavailability are usually calculated using an agreed unavailability tariff - based on the level of importance of various areas in the physical infrastructure. Each area is allocated a charge (tariff) per period of measurement that represents its importance to the client. The total of the unavailability tariffs in any one measurement period does not necessarily have to relate to anything, but is usually one to two times the availability charge for that period of time.

In the case of parallel services of PPPs, availability is measured by units of types of area, such as personal offices, open plan offices, restaurants or corridors. If any area fails its availability criteria, the area is deemed unavailable. Availability should be measured during the normal operational hours of the infrastructure. It is good practice to split the working day into more periods (say by the hour) to measure availability. This incentivizes the contractor to fix the problem as soon as possible, as it will be able to stop the unavailability "clock" that much earlier. However, in many situations, it does not make sense to the client to close an area for a short period of time, and in this case the availability period will be linked the actual time the client will be unable to use the area. For example, if a courtroom becomes unavailable, the court manager may have to cancel a half day list of cases at a time.

It is possible to define a trigger level, above which the whole building counts as unavailable. This may be a certain percentage of the building, or relate to particular key rooms. In the case of whole building or site unavailability, clients can choose to vacate the site. In this case, the total charge covering availability for that measurement period should be deducted from the payments due to the contractor. Mechanisms usually include a rebate on the deduction if the client does not depart from the unavailable area. Another complication can be added in the form of consequential unavailability, which makes deductions for areas which are not affected by the unavailability incident, but will not be used because another area is unavailable - for example, rooms off a corridor when the corridor itself is unavailable.

Finally, contractors should be allowed time to put right any area that becomes unavailable. The rectification period should be practicable to allow the appropriate personnel to attend each incident. If a failure is not rectified by the end of that period, then an unavailability deduction should be made. Clients should note that a short rectification period will signal to the contractor that a higher level of resources is needed to service the contract, for example an on-site engineer. Clients should therefore ensure that this is necessary before requiring it - as it will obviously increase the price of the contract.

| Output-based specifications identification [Peru - Decreto Legislativo N. 1012] Art. 7 Las entidades públicas identificarán los niveles de servicio que se busca alcanzar, a partir de un diagnóstico sobre la situación actual, señalando su importancia en las prioridades nacionales, sectoriales, regionales y locales, según sea el caso, en el marco de las cuales desarrollan los proyectos de inversión. [Mexico: Acuerdo Secretaria de Hacienda Diario Oficial 9 Abril 2004] 5. Las dependencias y entidades deberán especificar los servicios que pretendan recibir a través de la realización de un proyecto para prestación de servicios. Dentro de estos servicios se podrán incluir aquellos que sirvan de apoyo a las dependencias y entidades para dar cumplimiento a las funciones y los servicios públicos que tienen encomendados. Quedan excluidos los servicios públicos que, de acuerdo a las leyes, deban ser proporcionados, de manera exclusiva, por el sector público. Measurable service outputs. [Victoria (Australia) - Partnership Victoria, Practitioner's Guide, 2001] Government requirements can be expressed and measured in output terms. Payment mechanisms are generally structured around these output specifications to provide incentives for achieving key performance indicators; Payment related to level of output achieved [Mexico: Acuerdo Secretaria de Hacienda Diario Oficial 9 Abril 2004] Art.10 Las dependencias y entidades no deberán realizar pago alguno al inversionista proveedor antes de recibir los servicios objeto del contrato de servicios de largo plazo, salvo que la Secretaría autorice pagos anticipados conforme a los términos y condiciones establecidos en el contrato respectivo. Art. 31 El contrato de servicios de largo plazo deberá contener una metodología específica que permita evaluar el desempeño del inversionista proveedor. En caso de que el desempeño del inversionista proveedor, evaluado mediante la metodología prevista en el contrato de servicios de largo plazo, sea inferior al convenido, se aplicará un descuento al pago que deba realizar la dependencia o entidad contratante o alguna otra forma de penalización por deficiencia en el desempeño. El cálculo del descuento o la determinación de la penalización se hará conforme a las fórmulas que al efecto se establezcan en el contrato de servicios de largo plazo. [Brazil: Lei 11.079, Art. 5] Art. 5. The clauses of public-private partnership contracts shall be in accordance with the provisions of art. 23 of Act 8987, dated February 13th, 1995, as applicable, and shall also state: V - the mechanisms to preserve the nature of the service provision; [France - Ordonnance n°2004-559 du 17 juin 2004 sur les contrats de partenariat. (Modifié par LOI n°2008-735 du 28 juillet 2008) Art.1] II - La rémunération du cocontractant fait l'objet d'un paiement par la personne publique pendant toute la durée du contrat. Elle est liée à des objectifs de performance assignés au cocontractant. Output specifications as mandatory contract clauses [Brazil: Lei 11.079,] Art. 5The clauses of public-private partnership contracts shall be in accordance with the provisions of art. 23 of Act 8987, dated February 13th, 1995, as applicable, and shall also state: V - the mechanisms to preserve the nature of the service provision; VII - the objective criteria for evaluating the performance of the private partner; Art. 7. The payment provided by the Public Administration shall obligatorily be preceded by service delivery. Sole paragraph. According to the terms of the contract, the Public Administration may pay the private sector partner for the portion of the service that is made available. |

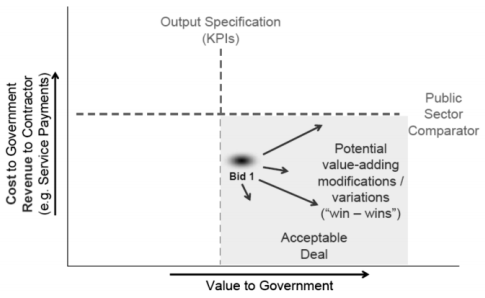

Performance payments for the services under a PPP/PFI contract should be SMART (specific, measurable, achievable, realistic and time-bound) and linked directly to the 'requirements of the 'output specification' for the PFI/PPP contract. They should also be weighted to reflect the importance of each test. The performance of contractors can be measured against a series of key performance indicators ('KPIs'). Services that fail to meet these KPIs will attract a penalty. Each KPI should be weighted to reflect its importance to the client, and the size of the penalty will be directly linked to the weighting of the KPI. It should be noted that it is not unusual for contracts to allow some failures to occur before a deduction is made. For example, a building may be allowed to have five areas identified as dirty during any 30 day period before a deduction is triggered. Subsequent breaches would attract deductions, which can be ratcheted to reflect a higher level of service failures overall. The KPIs are useful to ensure output given compliance to specifications and deliver payment mechanisms (see graph below).

If outputs do not meet specifications, contract is not awarded (if project is in the bidding process) or contractors may be penalized. The area where KPIs are met and public sector underperforms in relation to the private contractor (in terms of cost and delivery) is where contractor is subject to payment.

Output specification, value adding and space of payment

In addition to deductions within individual services, clients could also consider escalating the deductions further aimed at penalizing poor overall management of the services. For example, when total service deductions pass 25% of the month's unitary charge, an additional deduction of 5% could be added. However, if this kind of structure is adopted, it is very important to ensure that one ratchet does not cause the other one, as this is unfair to the contractor.

Contracts, or project agreements, generally contain a provision that links termination to a level of deductions over a period of time (measured as a percentage of the unitary charge), or to the number of KPIs failed in that period of time. It is critical to the fair operation of the contract that the payment mechanism is graduated and does not contain any 'small triggers' that could led to a termination for a minor transgression. If it does, then the contractor will have priced for this risk and included for it in the payment mechanism - the client will therefore be paying over the odds for the service. One way of ensuring that the termination provisions do not contain any nasty surprises is to construct an escalating system of warnings and lesser penalties before the final termination position is reached. Payment mechanisms are often in more innovative contracts where risks are shared between the parties and performance is attached to costs and service delivery.

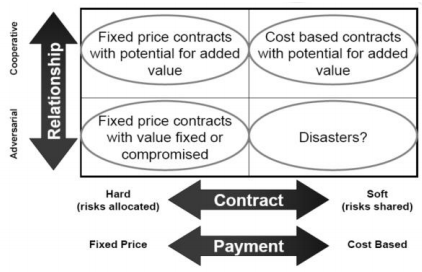

Payment Mechanisms and Risk Sharing provide a Cooperative relationship