INTRODUCTION

1. Infrastructure is a key element of the business environment and a generator of employment. However, increasing demand for infrastructure in the Middle East and North Africa (MENA) region is being met by declining private investment in major projects due to global economic conditions, banking prudential requirements and regional political uncertainty.

2. Estimates of infrastructure funding needs in the MENA region vary widely. According to the Arab Financing Facility for Infrastructure (AFFI), a joint venture of the World Bank, the International Finance Corporation (IFC) and the Islamic Development Bank (IsDB), the Arab world needs to invest between $75 billion and $100 billion a year in infrastructure to sustain the growth rates achieved in recent years, boost economic competitiveness and foster job creation. According to the World Bank1, MENA region infrastructure needs through 2020 are estimated at about USD 106 billion per year or 6.9% of the annual regional GDP. Investment and rehabilitation needs are likely to be particularly high in the energy and transport sectors - and this type of infrastructure has especially strong employment generation effects. Overall, there is potential to generate around 2 million direct jobs throughout the MENA region and 2.5 million direct, indirect and induced infrastructure-related jobs by meeting estimated annual investment needs.

3. Persisting political and economic uncertainty due to the war in Syria (especially for Jordan and Lebanon), increased sectarian violence (for example, in Iraq, Lebanon and Libya), and general security concerns and political polarisation (such as in Egypt), affect foreign direct investment (FDI) flows into MENA economies. The region has been adversely affected by deteriorating trade, tourism, real estate, finance, and banking prospects and has seen FDI decline by 15% to an estimated USD 17 billion in 2013. However, recent history shows that a quick and strong rebound in FDI is possible. After plummeting in 2011 from an earlier peak in 2008, flows into the MENA region rebounded by 43% in 2012 to reach USD 19 billion, reflecting underlying investor durability even in the face of political risk. The rebound was particularly strong in Egypt, which had been adversely affected by a deteriorating economy, an uncertain political outlook, and significant downside risks. FDI flows there reached nearly USD 3 billion in 2012, having registered net divestments the previous year.

4. Political uncertainty has also taken a toll on private investment in infrastructure. To restore investors' confidence, the governments of Egypt, Jordan, Morocco and Tunisia have implemented economic and institutional reforms. One of their key challenges looking ahead will be to strengthen the legal environment for investment, in particular infrastructure investment.

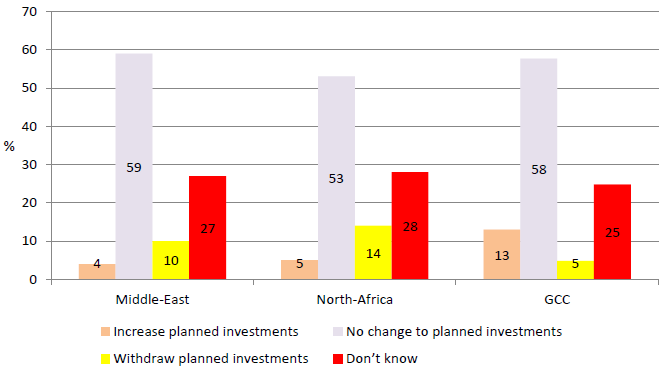

5. Although they acknowledge the tremendous growth potential of the region, private operators usually consider the investment situation on the ground in MENA as being, "highly complex". The economic and political situation has led most investors to adopt a "wait and see" approach (MIGA 2013). Even though some progress is being made in some countries, high social and political instability is still weakening investor sentiment. The holding pattern adopted by investors contributes to the current deterioration in the economic situation and in the quality of public sector services and infrastructure.

| Figure 1. Impact of political and social instability on investment plans in the MENA region (2013) |

|

|

| Source: Multilateral Investment Guarantee Agency (MIGA) (2013), World Investment and Political Risk. |

6. The "high risk" perception of the MENA region is not just the result of the financial crisis and the recent political upheaval in the region, but also the combined effect of several pre-existing elements:

• Lingering negative perceptions of the business and general investment climate, both overall and on a country level. For several years some MENA countries have ranked poorly in business environment comparators such as the World Bank Doing Business report. This negative perception is partly the result of inadequate infrastructure, but also of an inefficient regulatory framework and uneven compliance with contractual obligations by governments and public entities. This has been compounded by a number of investor - state investment disputes in certain countries, as evidenced by the number of arbitration cases before the International Centre for the Settlement of Investment Disputes (ICSID). A good portion of these disputes have been in the infrastructure sector.

• The lack of regional cooperation, coordination and integration, together with the disparate nature of MENA economies. The MENA region is often considered one of the most economically heterogeneous in the world. This makes it difficult to find regional answers to issues which have a direct impact on infrastructure investment and financing, such as the lack of developed capital markets and frequent exchange rate variations. It also impedes the development of interconnections in sectors as energy and transport.

7. For infrastructure projects, these regional factors converge with the complexity of financing long-term infrastructure investments and several recurrent challenges in project finance, such as:

• High upfront development and financing costs;

• Slow delivery;

• Identification of appropriate project finance and public-private partnership techniques;

• Obstacles to refinancing project debt;

• Ensuring efficient risk allocation among project participants; and

• Public officials ill-equipped to select and develop bankable infrastructure projects.

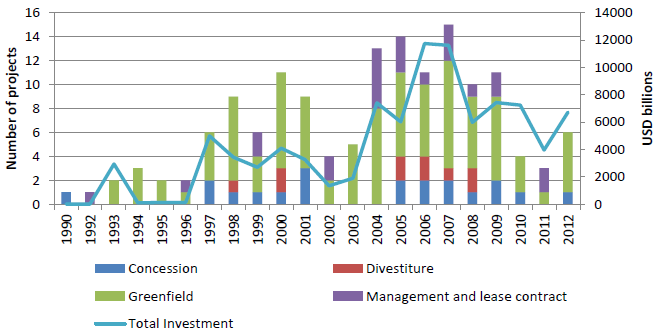

Figure 2. When region-specific factors are combined with the inherent challenges of infrastructure, attracting investment to the region can be more difficult than in other regions and will often involve higher costs and lower returns. However, data from the Public-Private Infrastructure Advisory Facility (PPIAF) shows a nascent recovery trend for infrastructure PPP in the MENA region. This trend remains to be confirmed.

| Figure 3. Infrastructure projects in the MENA region, by type of projects (1990-2012) |

|

|

| Source: OECD, based on PPIAF PPI database, last updated May 2014. |

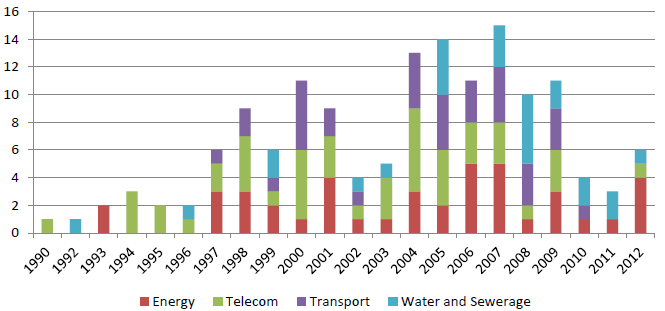

| Figure 3. Private infrastructure projects in the MENA region, by sector (1990-2012) |

|

|

| Source: PPIAF database, December 2013 |

8. Heightened perceived risk in the MENA region is not the only explanation for decreased private sector capital availability, including from commercial banks. Deleveraging by Euro area banks, not only in response to market pressures but also to prepare for tighter Basel III capital requirements over the 2013-2019 period, has also played a role in increasing the cost of capital available for infrastructure projects and in raising the quality standards applied in project selection. In the wake of the global financial crisis, traditional sources of finance for large-scale, long-term projects have been declining and the gap between infrastructure funding and infrastructure demand has widened. Although international capital markets have been recovering since 2009, private funding for infrastructure projects has become more selective and focused on higher quality projects.

9. The number of banks active in MENA project finance and infrastructure deals has declined markedly in recent years. Collins and Godfrey have estimated that before the global financial crisis, there were at least 40 regional and international banks that regularly participated in project finance and infrastructure deals in the MENA region2 and that this number has probably declined by more than half. Much of the decrease is due to international banks withdrawing from the market or scaling back their involvement in regional deals. The banks that remain generally have much reduced funding, and in some cases reduced technical capacity, especially for complex transactions in markets where perceived risk is high. In this context of scarce bank liquidity, and growing country risks, traditional lenders have limited appetite and capacity to lend long-term on an unsecured basis, and the absence, underdevelopment or limited availability of appropriate risk mitigation tools, together with a lack of refinancing and credit enhancement mechanisms, has made some project structures unattractive. This can make infrastructure projects in MENA more difficult to structure than in other regions, often with higher costs and lower returns.

10. Scarcer resources mean that MENA governments have to carefully select projects in the context of a well understood and appropriate legal, regulatory and financial environment. According to the European Investment Bank3, a key advantage of well-structured project financed PPPs, as opposed to traditional procurement methods, is the project discipline created in terms of due diligence and thorough planning. Although most MENA countries already have had some success with PPPs and/or are preparing to introduce structural reforms necessary for them to work, there are numerous prerequisites for a successful PPP programme, including institutional and legal frameworks, capacity and high-level political commitment. The pages that follow will consider some of these conditions.

____________________________________________________________________

1 . World Bank (2012), Infrastructure and Employment Creation in the Middle East and North Africa, Caroline Freund and Elena Ianchovichina, Quick Notes Series Number 54.

2 . Collins N. and Godfrey M. (2013), The Middle East and North Africa: How the MENA region is meeting the funding challenge. Latham & Watkins LLP.

3 . European Investment Bank (2011), Study on PPP Legal and Financial Frameworks in the Mediterranean Partner Countries, Facility for Euro-Mediterranean Investment and Partnership (FEMIP) Trust Fund.