ANNEX 1: CASE STUDIES

| Box 9. Egypt: The New Cairo Wastewater PPP The New Cairo Wastewater Treatment Project, the first project finance operation to be launched under the new PPP Programme in Egypt, consisted of a land-mark concession for the design, financing construction, operation and maintenance of a new wastewater treatment facility worth USD 482 million. Project Rationale Since 2006, Egypt's water sector has been identified as a priority by the Egyptian Government. Inadequate water sanitation infrastructure, limited service provision and rapid population growth led the Government to consider new approaches for financing and managing water supply and sanitation services that would involve greater accountability for performance, improved operational efficiency, and a reduced fiscal burden. The project aims to improve sanitation services and accommodate projected population growth in New Cairo, a satellite city created in 2001 to alleviate overcrowding in central Cairo, and where the population of 550,000 is expected to increase to approximately 3 million by 2029. The project is also intended to promote PPP as a model for future cost-effective, environmentally safe water and wastewater treatment projects in Egypt. Project Characteristics • Description: PPP concession agreement under which the private partner shall design, finance, construct, operate, and maintain a new wastewater treatment plant with an initial capacity of 250,000 m3 per day. The final capacity will be 500,000 m3 per day. • Timeline: - Concession awarded in June 2009 - Financial closure in February 2010 - Construction started in February 2010, initially expected to be completed in March 2012 and operational in June 2012 - The project was cancelled in May 2012 in the aftermath of the political events. • Advisor: - The International Finance Corporation ("IFC") was asked by the Egyptian Government to help develop and implement a model PPP that could be replicated in other infrastructure projects, and was appointed as lead advisor for the transaction and international competitive tender. - PPIAF had also been requested to prepare a capacity assessment, conceptual framework and transaction model for the project in 2006. Contract Scheme • 20-year BOT concession contract worth USD 482 million, covering engineering, procurement and construction, as well as operation and maintenance. • Contractor: - New Urban Communities Authority (NUCA), under the supervision of the Ministry of Finance (PPP Central Unit) and the Lead Advisor (IFC) - Orasqualia: a 50/50 joint venture between Aqualia and Orascom Construction Industries (OCI) • Tender procedure: - The international competitive tender process included an initial prequalification of prospective bidders based on financial and technical criteria. Seven bidders were prequalified out of the 10 applications received. - The project attracted five bids from consortia comprised of local, regional, and international firms. - The bidding was organised in two steps: a technical bid, evaluated on a "pass/fail" basis, and a commercial bid, limited to bidders of which the technical offers had been accepted. - The selection criteria consisted in the net present value of the overall sewage treatment charge throughout the concession period. Financing Scheme • Mobilisation of USD 150-200 million (EGP 800 million). • The Government to pay a sewage treatment charge to the private partner, including a fixed portion to cover the investor's fixed costs (e.g. debt servicing and return on equity) and a variable portion based on the actual volume of treated sewage, to cover the investor's variable costs. • Electricity costs to be paid by the New Urban Communities Authority (NUCA) (off-taker) as a pass-through item. Accordingly, bidders were requested to quote their projected electricity consumption level. • Ministry of Finance to guarantee the credit of the New Urban Communities Authority. • European Bank for Reconstruction and Development to acquire a share of Orascom/AqualiT. Obstacles and Lessons learned Operations were delayed due to political instability. The contractors selected in 2009 did not predict the social uncertainty, political unrest and economic crash following the 2011 uprisings. Orasqualia managed, however, to continue construction through three successive governments. Sources: International Financial Corporation, World Bank Group (2013), Infrastructure stories of impact: New Cairo Wastewater Treatment Plant is Egypt's First Public-Private Partnership ; Public-Private Infrastructure Advisory Facility (2013), Impact Stories: PPIAF Support Ground-breaking Public-Private Partnerships in the Wastewater Sector in Egypt ; International Financial Corporation, World Bank Group (2010), Public-Private Partnership Stories, Egypt: New Cairo Water.

|

| Box 10. Jordan: The Queen Alia Airport Expansion PPP The new terminal building at Amman's Queen Alia International Airport (QAIA) in Jordan is a prime example of a successful PPP, with a 25-year concession supported by funds from the governments of Canada, France, Japan, Kuwait, the Netherlands, and the United States, the Islamic Development Bank and USAID. The project includes the rehabilitation of existing facilities, the construction of a new terminal, as well as the operation of the airport. With a yearly capacity of 12 million passengers and its expected generation of more than 20,000 direct and indirect job opportunities and USD 1 billion in foreign direct investments, the new terminal has been classified by IFC as one of the 40 best PPP projects in emerging markets. Project Rationale Jordan aims to develop the country's only international airport into a gateway to Africa, Asia, and Europe. Queen Alia Airport, located 32 km south of Amman, is Jordan's principal airport since it was built in 1983, accounting for 97% of the country's air traffic, and is an increasingly popular transit point for tourists, business travellers, and international air freight. The airport was unable to meet sustained growth of 7% per year in passenger traffic over the last decade, reaching 3.5 million visitors in 2006 - a figure expected to rise to 12.8 million by 2030. In a bid to meet increasing demand for capacity and to position QAIA as a regional financial, trade, and transport hub, the Government of Jordan sought private sector participation to rehabilitate and increase the capacity of the airport through a user-fee PPP concession. The project involves upgrading and operating the existing terminal, building and constructing a new 900,000 square foot adjacent terminal building. The QAIA expansion project, which was part of a broader strategy to liberalise air transport policies, restructure civil aviation, improve competitiveness and eliminate budgetary support to the airport, is already serving as a model for launching a full-scale PPP programme in infrastructure. Project Characteristics • Consortium: Airport International Group, comprising: - Abu Dhabi Investment Corporation (UAE): 40 % - Noor Financial Investment Company (Kuwait): 25 % - Joannou & Paraskevaides Overseas (UK and Cyprus) - J&P Avax subsidiary (Greece): 10% - Aéroport de Paris Management of France (France) : 5% • Lead advisor: International Finance Corporation • Timeline: - Agreement signed on May 2007 with financial close on December 2007. - Stage 1 completed in June 2013 with new terminal opened for traffic in late March 2013 - Stage 2 (expansion) in 2014-2016 to increase airport capacity Contract Scheme • Description: Concession agreement to upgrade, expand, rehabilitate, operate, and maintain QAIA • Duration: 25 years • Bidding process: Through an international bidding process, six consortia representing more than 25 international investors were qualified. Financial bids were evaluated based on the payment of annual concession fees as a percentage of gross revenues to the government, the private partner being entitled to the remaining share of the airport gross revenue in exchange for assuming construction, operation, and demand risks. The concession was awarded to the Airport International Group with a bid offering a concession fee of more than 54% of gross revenues for the term of the agreement. Financing Scheme • The project was funded by equity of the sponsors, a syndicated loan extended by European commercial banks and direct loans from IFC and Islamic Development Bank. The obligor of the loan is the special purpose vehicle (SPV) with no third-party guarantee provided. • Capital value: USD 675 million, including combination of USD 370m debt and USD 305m equity. • Financiers: Islamic Development Bank: USD 100 million lease; International Finance Corporation (IFC): USD 280 million financing package consisting of the following: - The "A loan" of USD 70 million provided through a 17-year senior loan ; - The "B loan" of USD 160 million provided under a 16-year syndication formed by Calyon, Natixis and Europe Arab Bank. A swap was provided to minimize the interest rate risk of the transaction. - The "C quasi-equity loan" of USD 40 million under a 18-year subordinated loan with a 15-year grace period to match concession cash flows ; and - A stand-by facility of USD 10 million to be disbursed in the event that cash flows generated are insufficient to complete the financing of the terminal during the construction phase. Obstacles and Lessons learned The project presented several challenges due to legislative changes, high up-front capital costs, and long payback periods that were required for a project of this size. Commercial banks were not willing to provide long - term financing for a project without political risk mitigation. Furthermore, the iconic design had to be brought back into line with the economics of the project, with scope for future expansion, and disturbance to operations also had to be minimized during construction phase. Despite the 25-years duration of the concession agreement, the loans terms are of approximately 15 years, leading to further refinancing risks for the SPV. As for lessons learned, the consortium of sponsors that formed the SPV - including major construction companies and Aéroport de Paris, an experienced airport operator - had significant financial and technical capacities. In an effective bid evaluation process, the technical competence, strength and experience matter as much as the price offered. The winning consortium combined a strong lead investor, an experienced airport operator, and regional and international construction experts. There was also a commitment for appropriate management resources during the operation stage. IFIs also play a major role as advisers for the development of large, complex PPP projects, especially in ensuring effective bid evaluation and bid management. The IFC advisory team, for instance, commissioned traffic reports from independent advisers to confirm traffic volume and revenue forecasts, and assess the bankability of the design and legal framework. IFC also helped in holding a fair and transparent bidding process that attracted leading airport operators and construction companies. Development finance institutions, participating as financiers and guarantors, also contribute to enhancing project credibility for providers of long-term finance, investors and contractors. Of the project's cost of USD 675 million, IFC committed USD 120 million and helped mobilise USD 160 million in funds from regional and international commercial banks. Sources: PPIAF, The International Bank for Reconstruction and Development / The World Bank (2011), How to engage with the Private Sector in Public-Private Partnerships in Emerging Markets; International Finance Corporation; World Bank (2009), Public-Private Partnership Stories, Jordan: Queen Alia International Airport. |

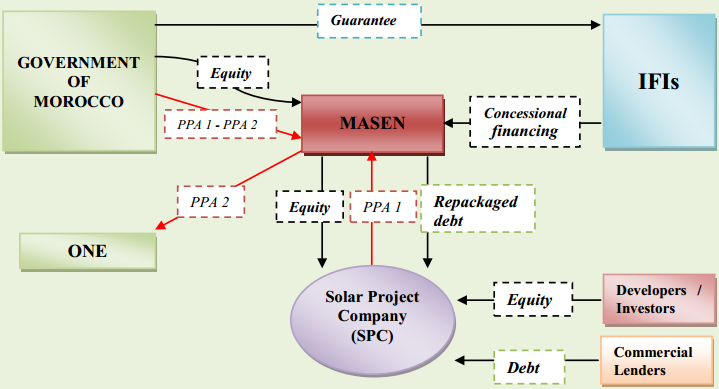

| Box 11. Morocco: The Ouarzazate "Noor 1" CSP Project The Ouarzazate Concentrated Solar Power (CSP) project, also referred to as "Noor" (i.e. "light" in Arabic), is one of the projects identified and designed within the MENA CSP Scale-Up Initiative, a regional programme financed by the Clean Technology Fund and led by the World Bank and the African Development Bank, with plans to install 1.2 GW across Algeria, Egypt, Jordan, Morocco and Tunisia. The project is being developed through PPP, with competitively-selected partners, by a Special Purpose Vehicle: a consortium of private developers and the newly-created Moroccan Agency for Solar Energy (MASEN). Phase 1 of the 500 MW Power Plant Project (160 MW) will make the Ouarzazate CSP Project the largest solar independent power producer (IPP) in the world. Project Rationale Concentrated Solar Power has enormous unexploited potential in the region as a reliable source of renewable energy. However, despite its relatively long track record, CSP technology remains in its early stages of development and is still not commercially viable. In Morocco, where heavy fossil-fuel subsidies distort energy prices, the resulting competitiveness gap between CSP and less expensive carbon-intensive energy alternatives is particularly evident. The Government of Morocco, together with a group of multilateral development banks and private-sector sponsors, is developing the 160 MW Ouarzazate CSP Project, labelled "Noor 1". Located 200 km south of Marrakesh, the plant should come on line by 2015 and help Morocco avoid 240,000 tons of CO2 emissions a year, the equivalent of removing 80,000 cars from the road annually. The project has two over-arching objectives: • Installing CSP at a scale that successfully demonstrates the storage technology component, and generates cost reductions and associated economic benefits (local manufacturing, energy security and a shift away from fossil fuels) ; • Testing a business model, via the PPP formula, that could increase private-sector backing and increase availability of capital and know-how to support the development of a CSP portfolio. Project Characteristics The first Ouarzazate solar plant will have a capacity of 125 to 160 MW and will use the most mature CSP technology currently available: parabolic trough, with three hours of molten salt thermal energy storage capacity. Construction of the plant is underway, and commercial operation expected in the second half of 2015. Key stakeholders include: • The Government of Morocco and the Moroccan Agency for Solar Energy (MASEN), which are expected to contribute USD 883 million over the life of the plant (mostly in the form of operational subsidies) ; • International financial institutions and other donors which have committed in excess of USD 1 billion for the construction of the facility; • A consortium of private developers, which will contribute USD 190 million of equity capital and expertise for an estimated 14% after-tax rate of return. ACWA Power International (95% Saudi Arabia), Aries Ingenieria y Sistemas (Spain), TSK (Spain). Contract Scheme • Greenfield project, Build-Own-Operate-Transfer (BOOT). • Duration: 25 years PPA. • Contractual arrangements - EPC Contractor: Acciona, Sener and TSK (Spain). - Off-taker: Office National d'Electricité (ONE). - Tariff Rate (PPA): 1.62 dirhams per kWh. Figure 6. Noor 1: Institutional and Financing Framework

Financing Scheme The project was made possible through a substantial subsidy from the Government of Morocco, in the form of a power purchase agreement covering the expected 25-year lifetime of the project. • Project Cost: USD 1.438 billion. • Government of Morocco committed to subsidise MASEN for the annual difference between the cost of CSP power (price MASEN will pay to private developer under the PPA) and the national electricity price (price ONE will pay to MASEN), and issued sovereign guarantees to the lenders. • International financial institutions. Table 6. Noor 1: Multilateral Lenders

Source: World Bank Table 7. Financing Options for the Ouarzazate CSP plant

Source: World Bank Obstacles and Lessons learned With its successful financial closure, the project, the first publicly-supported CSP project and among the cheapest to be financed, has proven that a large-scale infrastructure project could be financed within the planned budget in an emerging economy. The project remains an example of successful PPP in the renewable energy sector. Among the highlights of this project: • Strong public support, via a favourable regulatory and policy framework, a specialized entity tasked with developing CSP projects and Government's financial support to implement the ambitious Moroccan Solar Plan; • Significant financial and technical contributions from IFIs: early concessional finance, driving down capital costs by 25-30%, as well as institutional and specialised technical support ; • Strong engagement and coordination of donors: early agreements between donors and MASEN gave a clear indication of project terms and costs, transparency and competition among private investors resulting in satisfactory rates of return (bids were in line or below projected levels) ; • A carefully designed PPP model, allowing for optimal alignment of risk between public and private players: the private developer bears construction and operational risk while the Government of Morocco will bear electricity market risk (revenue risk), MASEN acting as both equity investor and power purchaser (off-taker). Nonetheless, there is room for improvement: • Inadequate institutional structures, insufficient coherence and cooperation between Ministries, strategic guidance: in the quality of the bidding process: MASEN found out late that it would need to take a stake itself to offset some operational costs that the winning bidder did not want to bear ; • Insufficient information made available to investors, lack of experience in the administration and lack of financial incentives: the plant is still to begin operating and test its commercial and economic development objectives. Finally, to become commercially viable and achieve grid parity, the project needs to build on potential economies of scale through regional CSP scale-up and decreasing technology costs: • Scaling up the CSP portfolio in Morocco and the MENA region; only a critical mass of publicly supported CSP projects will help drive faster technology cost reductions, combined with the gradual removal of fossil - fuel subsidies ; • Exports to European markets: given that MENA domestic grid prices are significantly lower than current CSP generation costs, there is a huge potential that requires several preconditions (brokering bilateral and multilateral agreements, removal of subsidies, physical investments in interconnection systems and testing effective demand from EU member states…) and presents a trade-off for Morocco between financial viability on one hand, and domestic energy and environmental effects on the other. Source: Climate Policy Initiative (CPI) (2013), "San Giorgio Group Case Study: Ouarzazate I CSP". |

| Box 12. Tunisia: The Enfidha-Monastir Airport Project The Enfidha-Monastir Airport project involves constructing a new airport under a BOT concession for the decongestion of the existing Tunis and Monastir airports, with a capacity of 5 million passengers/year. Project Characteristics Tunisia's existing airports are either already saturated (Monastir handled 4.2 million passengers for a nominal capacity of 3.5 million) or nearing saturation (Tunis Carthage airport). Due to growing tourism, negotiations on an open skies agreement with Europe and major planned tourism and industrial developments, the upgrade and expansion of Tunisia's airport infrastructure was a key priority of the Tunisian Government. In 2007, the Government of Tunisia awarded two 40-year concessions (including a two-year construction period): • A concession to build, finance and operate a new international terminal at Enfidha for an initial capacity of 7 million passengers (Enfidha is located in Central Eastern Tunisia, 45 km from Monastir airport) ; • A concession to upgrade and operate the existing Monastir international airport (4.2 million passengers in 2006). This approximately EUR 560 million (USED 840 million) project was to be among the largest private sector investments in Tunisia and the first private sector airport concession in the Maghreb region. • Timeline - 1998: initial project launched. - 2001: feasibility study finalised. - April 2004: first tender fails due to disagreement between the Government and private operators on terms and conditions of construction. Project reshaped and simplified. - 2007: new tender, awarded to TAV (Turkey). - December 2009: operational after record 823 days. Project Rationale A new airport was built at Enfidha as the Monastir airport cannot be expanded due to geographical and environmental constraints. Both airports will serve the major tourism areas of Monastir, Sousse and Hammamet, located on the Mediterranean coast. The Enfidha Airport will primarily operate charter traffic, serving a large number of tourism complexes that stretch along the coast. The project is expected to create about 2200 direct jobs during the construction phase and 1200 direct jobs during operations. A further 10,000 direct jobs are expected to be created in the local private sector. The project will also generate revenue for the Government and, by supporting tourism, act as a major source of foreign exchange. The project is economically and financially viable, and environmentally sound. It will have a major impact, not only on the infrastructure sector but also on tourism and associated industries, and it will help boost Tunisia's GDP and global competitiveness. Target 2.800 new jobs created and 2.1 million passengers expected in 2011. Objectives: • Relieve congestion at the Monastir Airport (target market: 8.5 million passengers per year) • Develop tourism in Tunisia in the coastal Sahel and Cap Bon areas (via charter flights) • Foster commercial and industrial activity around the Enfidha site, based on a multimodal transport network Contract Scheme • Concession (Build-Operate-Transfer) • Contractor : Office de l'Aviation Civile et des Aéroports (OACA), under the supervision of the Ministry of Transport • The private sponsor and major shareholder (99.99%) of TAV Tunisia S.A. is TAV Airport Holdings (TAV Airports), a Turkish company headquartered in Istanbul and specialising in airport operation and management. Financing Scheme • Total project cost is estimated at EUR 560 million, to be financed through a 30% equity contribution from the sponsor and 70% via debt. • Multilateral lenders - IFC (EUR 199 million loan) ; - African Development Bank (EUR 70 million loan) ; - Proparco (EUR 30 million) ; - OPEC Fund for International Development (EUR 20 million). • Private commercial banks: ABN ; Société Générale ; Standard Bank. Obstacles and Lessons learned The Enfidha airport project was the first transportation concession in Tunisia and the first airport concession in the Maghreb region. It can serve as a role model for airport PPPs in the North Africa region. Lessons learned related to: • Failure of the first bid due to sub-optimal project scoping (technical specifications, size and volumes) ; • Insufficient funding capacity: commercial banks unable to fund due to financial crisis ; Extension of the airport is planned for 2020-22 with a second terminal. Source: OECD (2010), Progress in Public Management in the Middle East and North Africa: Case Studies on Policy Reform. |