GLOBAL DEVELOPMENTS

Global economic conditions are improving, following a year of depressed economic activity. The global economic recovery is strengthening, supported by a continued upturn in manufacturing activity. In January, global industrial production increased at an annualized rate of nearly 6 percent, the strongest pace in five years. Activity accelerated in the Euro Area, Japan, China, and India, while moderating somewhat in the United States, the United Kingdom, and the Russian Federation. The global manufacturing Purchasing Managers' Index (PMI) improved further in February, while the services PMI remained high. Following four consecutive months of small gains, global (median) inflation rose sharply in January, to about 2.3 percent year-over-year-the highest level since end-2014. The uptick reflected the delayed impact of rising energy prices in 2016. Global goods trade rebounded strongly in the fourth quarter of 2016. This improvement coincided with signs of a bottoming out in global investment growth, which tends to be more trade intensive than other components of aggregate demand. Global export orders point to further improvements in the coming quarters.

Global financing conditions have been favorable since the start of 2017. Financial markets have continued to focus on the prospects of strengthening global growth, while discounting elevated levels of policy uncertainty. Implied volatility in the equity and bond markets remains well below historical averages. The decision by the Federal Reserve to raise rates was expected, and markets reacted positively, with bond yields and the U.S. dollar declining somewhat, and global equity markets remaining buoyant. The European Central Bank kept its stance unchanged, but confirmed that it would begin scaling back its asset purchases in April. Supported by continued monetary policy accommodation, Euro Area bond yields remain exceptionally low.

Financial markets in emerging markets and developing economies (EMDEs) have continued to rebound, supported by the increased risk appetite of international investors, some improvement in growth prospects, and more stable credit ratings among commodity exporters. Accordingly, capital inflows to EMDE bond and equity mutual funds remained firm in March, while international debt issuance increased strongly from January to March. Recent bond issuances by the Arab Republic of Egypt, Nigeria, Oman, and Kuwait attracted strong demand. Bond spreads are currently around 300 basis points, which is lower than the pre-U.S. election levels. Excluding the República Bolivariana de Venezuela, Emerging Market Bond Index spreads are now back to mid-2014 levels.

Commodity prices have firmed. Crude oil price jumped 8 percent in the first quarter of 2017 averaging nearly $53/bbl. Prices dropped below $50/bbl in the second week of March due to concerns over compliance of the OPEC/non-OPEC cuts, larger-than-expected U.S. crude oil inventories, and robust recovery in U.S. shale oil activity. But, they recovered to $54/bbl in early April, on renewed expectations of tightening supply. However, rebalancing is under way as the global oil market is expected to tighten in the second half of the year. Meanwhile, metal prices, which made some further gains in 2017Q1 on stronger demand from China and some supply tightness are now 35 percent higher than their 2015Q4 lows. Agricultural prices have been broadly stable on favorable growing conditions in most regions.

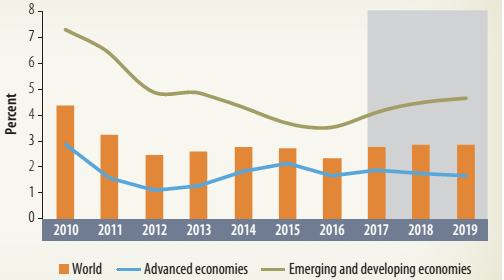

Global economic conditions are improving, growth is projected to pick up in 2017 and continue to strengthen into the next year. | FIGURE 1.1: Global Growth

Source: World Bank. | Global growth is projected to pick up to 2.7 percent in 2017, and to an average of 2.9 percent in 2018-19, broadly in line with previous projections (figure 1.1). Activity in advanced economies is expected to strengthen in 2017, supported by a projected upturn in the United Sates. |

The forecasts for advanced economies have been slightly upgraded, reflecting strengthening domestic demand and exports. After accelerating to 1.9 percent in 2017, growth in advanced economies is expected to moderate somewhat, to an average of 1.8 percent in 2018-19. Aggregate growth in EMDEs is projected to reach 4.1 percent in 2017 and 4.5 percent in 2018. Modestly rising commodity prices, a cyclical rebound in investment, and export growth are supporting a gradual recovery in commodity-exporting EMDEs. Among commodity-importing EMDEs, growth continues to be robust, as a gradual deceleration in China is offset by the rest of the group.